Published: 06-03-2026, 11:26 am | Updated: 06-03-2026, 12:21 pm

Gold is down on the day — off roughly 0.8% and trading near $4,454 as of Tuesday afternoon — but the bigger story didn’t come from the price ticker. It came from Frankfurt.

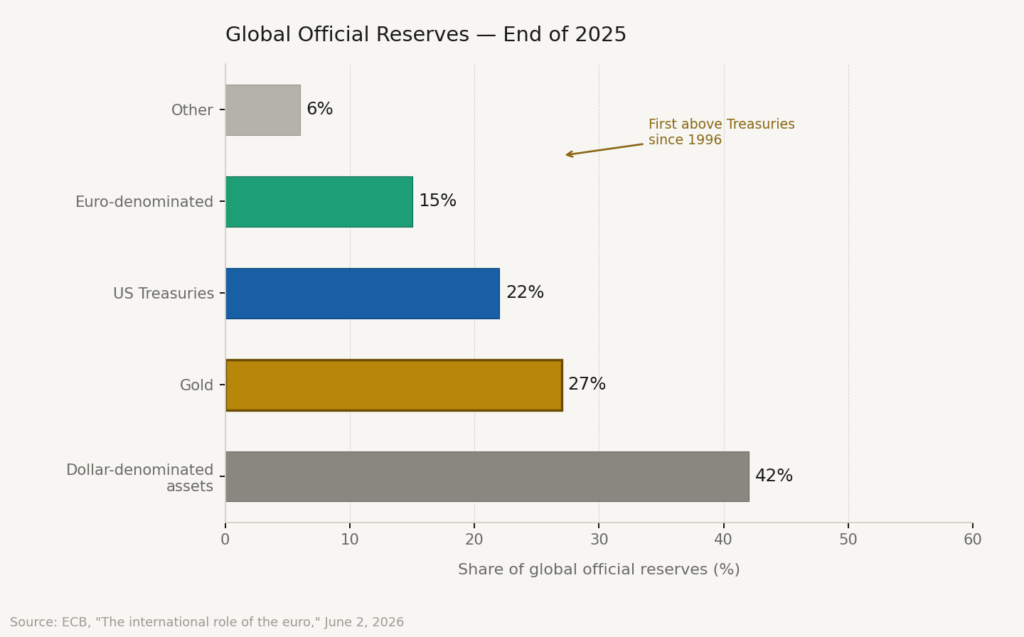

Yesterday, the European Central Bank published its annual report on global reserve assets. The headline: gold now makes up 27 percent of global official central bank reserves. That puts it ahead of US Treasuries at 22 percent and the euro at 15 percent. It is the first time gold has led Treasuries in global reserves since 1996.

The asset governments spent decades calling a relic of a bygone era just officially outweighed the asset they use to borrow money.

Why did gold’s share of global reserves jump seven points in a single year?

Two forces drove it — and both matter.

First: price. Gold rose approximately 60 percent in 2025, following a 30 percent gain in 2024 (ECB, June 2026). When any asset nearly doubles in value over two years, its share of a fixed portfolio rises mechanically. That holds even if nobody bought a single additional ounce. The ECB makes this explicit: at 2023 gold prices, US Treasuries would still lead at 26 percent, with gold at 16 percent.

Second: buying. Central banks purchased around 850 tonnes of gold in 2025. That is below the pace of 2022–2024, when purchases topped 1,000 tonnes annually. Even so, it remains historically elevated. Since Russia’s invasion of Ukraine, China has accumulated more than 350 tonnes, Poland added 320 tonnes, India bought 130 tonnes, and Turkey accumulated 220 tonnes before loaning or selling 130 tonnes in early 2026 (ECB, June 2026). Meanwhile, stablecoin issuer Tether was the single largest overall buyer in 2025, acquiring more than 100 tonnes — just ahead of Poland as the top official-sector buyer. That detail tells its own story about who is hedging against what.

So is this a valuation story or a buying story? Both. And the distinction matters.

The Edge Every Investor Needs Smarter precious metals investing starts here. The Nuggets Newsletter brings you essential market insights, Fed updates, global trends, educational videos, and much more.

Why didn’t central banks simply rebalance back into Treasuries when gold prices surged?

The mainstream framing — this is just a price effect, not real de-dollarization — is technically accurate. But it is strategically incomplete.

Central banks don’t passively hold whatever their portfolios become. They actively rebalance. If gold’s share had ballooned from a price rally and no country wanted it there, they would sell. Instead, central bank gold buying has run above historical norms for four consecutive years. Governments that could have rebalanced back into Treasuries chose not to.

That is a choice. And choices reveal preferences.

As a result, ECB President Christine Lagarde framed it plainly: “Geopolitical tensions continue to drive strong central bank demand for gold” (ECB, June 2026).

The mechanism is straightforward. After the US froze Russia’s dollar reserves following the 2022 Ukraine invasion, every government holding large dollar assets quietly asked the same question: what happens to our reserves if we end up on the wrong side of a US foreign policy decision? Gold holds no counterparty risk. It cannot be frozen, sanctioned, or seized through correspondent banking. It exists outside any nation’s legal system.

Notably, central banks now hold more than 36,000 tonnes of gold in total — approaching the 38,000 tonnes held during the Bretton Woods era, when the dollar itself was convertible to gold (ECB, June 2026). The reserve system is being quietly but deliberately restructured.

What are the limitations of gold as a reserve asset, according to the ECB?

The ECB report addresses this directly. Gold pays no yield. Its price is volatile. Storage is expensive. Supply cannot expand quickly to meet sudden demand. All true.

In other words, these are not bugs — they are features of a monetary asset that cannot be manufactured on demand. Every limitation the ECB names is, from a sound money perspective, a reason to trust it.

But here is what the ECB cannot quite say: every institution in that reserve composition table is simultaneously responsible for managing fiat currency. They are hedging against themselves.

If the stewards of the global monetary system are choosing to hold a larger share of gold, the individual saver has every reason to ask whether their own allocation reflects the same logic. Not because of a collapse thesis. Not because of fear. Because the smartest balance sheets on earth are making the same diversification decision that sound money has recommended for decades.

That is not doomsday thinking. That is financial sovereignty.

What should gold investors watch in the week ahead?

Friday’s US jobs report will drive short-term gold price action. The June 16–17 FOMC meeting — Kevin Warsh’s first as Fed Chair — will set the tone for the summer. But the reserve composition story is slower and more durable than any single data point. Central banks do not rebalance on weekly headlines. The trajectory here spans years, not months.

Key Takeaways

- The ECB confirmed gold now makes up 27% of global official reserves — ahead of US Treasuries at 22% — for the first time since 1996 (ECB, June 2026).

- The valuation caveat is real: at 2023 gold prices, Treasuries would still lead. But central banks chose not to rebalance away from gold when prices rose — that is an active preference, not a passive drift.

- Since Russia’s invasion of Ukraine, China, Poland, India, and others have systematically added gold. The common denominator: reducing exposure to assets that can be frozen or sanctioned.

Stay On Top of Gold & Silver Prices

Get important market alerts sent straight to your inbox.

SOURCES

1. ECB — The International Role of the Euro, June 2026

2. Xinhua — Gold Surpasses U.S. Treasuries, Euro in Global Official Reserves: ECB

3. The Northern Miner — Gold Overtakes US Treasuries in Global Reserve Shift: ECB

4. Canadian Mining Journal — Gold Overtakes US Treasuries in Global Reserve Shift: ECB

5. Mining.com — Gold Overtakes US Treasuries in Global Reserve Shift: ECB

6. South China Morning Post — China Among Top Gold Buyers as Bullion Overtakes US Treasuries: ECB

7. Yahoo Finance — Gold Overtakes US Treasuries as Top Central Bank Reserve Asset

8. World Gold Council — Gold Demand Trends: Central Banks, Full Year 2025

9. TradingEconomics — Gold Price

10. MPA Magazine — Key Dates That Will Define Kevin Warsh’s Opening Months as Fed Chair

Disclaimer: This article is for informational purposes only and does not constitute financial or investment advice. Always consult a qualified financial adviser before making investment decisions.

You May Also Like:

- Central Banks Just Crossed a Line Not Seen Since 1996

- Factory Costs Hit 82.1. That Number Is Now Working for Your Gold.

- Gold at $4,500: What Fort Knox, China, and Silver Are Telling You

- Silver Has Two Engines. Stagflation Is the One Condition That Fires Both at Once.

- The Buyer List for Gold Just Got Longer. These Countries Have Never Bought Before.

- PCE Hit 3.8%. GDP: 1.6%. Gold Went Up. Here’s the Mechanism.

- Gold Targets Are Falling. The $8,000 Forecast Isn’t.

- Gold Radar: 5 Stories the Price Chart Isn’t Telling You

- Silver Lost 3.3% While Gold Lost 1.6%. That Gap Is Not Random.

- Gold Down 1.2%, Silver Down 2.8% — The Floor Holds