Published: 07-10-2026, 09:32 am | Updated: 07-13-2026, 11:43 am

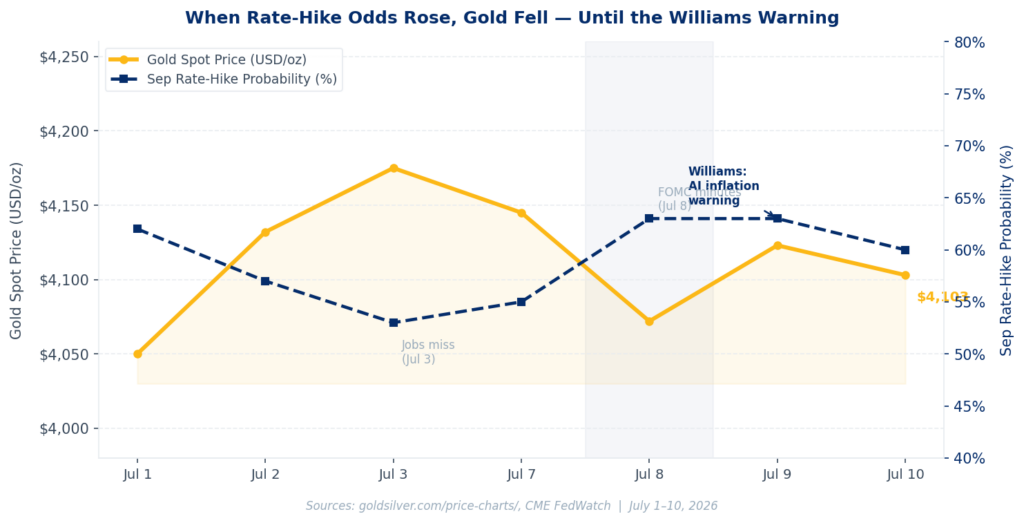

Gold is trading near $4,103 an ounce today, down about half a percent on the day and roughly 1.2% on the week. Mainstream financial media is framing that as a tech-sector story. New York Federal Reserve President John Williams said Thursday that AI-driven demand is now his single biggest inflation concern. Wall Street is reading that as bad news for Nvidia. That reading, however, is incomplete. For gold investors, Williams just confirmed something more important: the Fed’s inflation problem now has a structural engine that tariffs and energy alone cannot explain away.

What Did the Fed’s Williams Actually Say About AI and Inflation?

Williams spoke at a Federal Reserve workshop on market liquidity in New York on July 9, 2026. He said that among all the drivers of U.S. inflation, he is most focused on demand generated by artificial intelligence. Specifically, he stated that if AI demand creates a “sustained impulse to demand relative to supply,” the Fed “would need to respond.”

He also confirmed that core goods price inflation had risen partly due to what the June FOMC minutes called “AI-related pricing pressures.” That phrase appeared explicitly in the meeting notes released July 8. Furthermore, Williams set a clear inflation benchmark: if core PCE runs above 0.2% per month in the second half of 2026, he will treat it as evidence that inflation is more persistent than his baseline forecast. Core PCE currently sits at 3.4% year over year — well above the Fed’s 2% target, according to the Bureau of Economic Analysis.

The Edge Every Investor Needs Smarter precious metals investing starts here. The Nuggets Newsletter brings you essential market insights, Fed updates, global trends, educational videos, and much more.

What Does AI Inflation Mean for Gold?

AI-driven inflation is a new kind of sticky. Tariff inflation fades when duties stabilize. Oil inflation fades when supply routes reopen. AI capital expenditure inflation, however, does not have an obvious off-switch.

The major hyperscalers — Microsoft, Amazon, Google, and Meta — committed a combined approximately $410 billion in AI infrastructure capital expenditure in 2025 alone, according to company earnings filings compiled by the Financial Times. That spending creates demand for power, cooling equipment, data center construction, and advanced semiconductors. As a result, it bids up prices across the entire supply chain. Consequently, the Fed now faces a structural inflation driver that rate hikes can blunt at the margins but cannot eliminate.

Higher interest rates raise the cost of borrowing for AI infrastructure projects. They do not, however, reduce the strategic imperative of tech companies that fund their build-outs from operating cash flow. In other words, the AI capex boom is largely rate-insensitive. That matters for gold specifically: it means the Fed may need to keep rates elevated not because the broader economy is overheating, but because one concentrated sector keeps generating inflation that rate policy cannot fully reach.

Why Is This a Gold Story, Not Just a Tech Story?

Here is the mechanism gold investors need to understand. Gold does not respond directly to inflation. Instead, it responds to real yields — the return investors earn after subtracting inflation expectations from nominal interest rates. When real yields fall, non-yielding assets like gold become more attractive relative to Treasuries.

The AI inflation dynamic creates a specific real-yield scenario. If the Fed holds nominal rates steady — which CME FedWatch currently assigns a 74.9% probability for the July 28–29 meeting — while inflation expectations rise on Williams’s AI-demand warnings, real yields compress. That compression is the direct mechanism connecting today’s news to the gold price.

Moreover, Williams’s remarks arrived alongside a June FOMC minutes document. That document showed nine of the eighteen policymakers who submitted rate projections favor a 2026 hike. Meanwhile, three competing inflation pressures — tariffs, energy, and now AI — all push in the same direction. The Fed has identified a fourth structural reason it cannot reach its inflation target quickly. Each additional reason extends the timeline. Each month the timeline extends, the case for holding a non-yielding, inflation-resistant asset strengthens further.

What Is the Deeper Story That Most Analysts Are Missing?

The surface take from Williams’s remarks is familiar: the Fed is hawkish, gold faces rate headwinds, avoid precious metals until rates fall. Several institutional analysts are writing exactly that narrative this morning. That framing, however, focuses on the short-term rate mechanism while ignoring the structural trap beneath it.

Consider what actually happens if the Fed raises rates aggressively to counter AI-driven inflation. The U.S. government carries approximately $39.4 trillion in debt, according to Treasury Fiscal Data. Annual interest costs on that debt already exceed $1 trillion, per the Congressional Budget Office. Each quarter-point rate hike adds an estimated $90 billion or more in annual interest expense to the federal deficit. Therefore, the more aggressively the Fed fights AI inflation, the faster it expands the fiscal deficit — which, in turn, creates more monetary debasement pressure over the long term.

This is the trap. The Fed can slow AI-driven inflation at the cost of fiscal sustainability. It cannot do both simultaneously.

Gold investors have seen this dynamic before. The last time the Fed faced a structural inflation driver it could not fully contain with rate policy — the energy price surge of the 1970s — gold rose from $35 to $850 over a decade. The mechanism then was identical to what Williams described Thursday: a central bank caught between fighting inflation and protecting the financial system. Notably, history does not guarantee repetition. Nevertheless, the structural architecture of this problem closely resembles past episodes that proved durable tailwinds for physical gold.

Mark Your Calendar: July 14 Is the Next Test

The June CPI report lands Tuesday, July 14, alongside Chair Kevin Warsh’s congressional testimony. A CPI print above 4.0% year over year would likely push the September rate-hike probability above 70%. A print below 3.8% would be constructive. Warsh’s framing of AI-driven inflation will tell you whether the Fed treats this as a temporary spike or something more durable.

As the June FOMC minutes revealed, the committee is split, not settled. Gold at $4,103 is trading just below the World Gold Council’s mid-year fair value band — meaning the market has priced in one hike but assigned little premium to the structural inflation problem Williams just named. That gap is worth watching.

Stay On Top of Gold & Silver Prices

Get important market alerts sent straight to your inbox.

SOURCES

1. Fortune — Federal Reserve’s John Williams Says AI Is Now His Main Inflation Concern

2. Bloomberg — Fed’s Williams Says AI Is Now His Main Inflation Concern

3. FXStreet — Fed’s Williams: Inflation Is Still ‘Far Too High’

4. Bureau of Economic Analysis — Core PCE Price Index, May 2026

5. Federal Reserve — June 2026 FOMC Meeting Minutes, released July 8, 2026

6. CME Group — FedWatch Tool, accessed July 10, 2026

7. Congressional Budget Office — Budget and Economic Outlook 2026–2036

8. U.S. Treasury — Fiscal Data, Debt to the Penny

9. GoldSilver — Live Gold Price Charts

Disclaimer: This article is for informational purposes only and does not constitute financial or investment advice. Always consult a qualified financial adviser before making investment decisions.

You May Also Like:

- Five Days From Now, Two Numbers Will Decide Gold’s Second Half

- Bank of America Cut Its Gold Forecast. The Reason Is More Bullish Than It Looks.

- The Fed Is Split 9 to 8. Gold and Silver Are Paying the Price — Until July 14.

- Gold Is Sitting on $4,000. The World Gold Council Has a Model for What Happens Next.

- Trump Called the Deal Dead. Oil Jumped 6%. Gold Fell. Here Is Why Both Moves Make Perfect Sense.

- China Just Bought Its Most Gold Since 2023. It Did It During the Quarter Gold Fell 16%.