Daily News Nuggets | Today’s top stories for gold and silver investors

October 7th, 2025

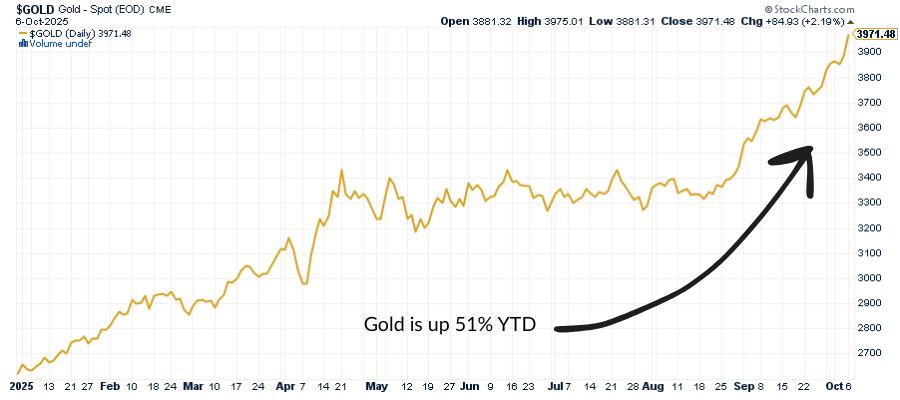

Gold Rush Nears $4,000, Silver Approaching $50

Gold surged toward the $4,000 mark Tuesday, while silver climbed within striking distance of $50 as investors poured into precious metals amid mounting global uncertainty. Analysts cite a perfect mix of drivers — political volatility, weak U.S. data, and record central bank demand — fueling the move.

Gold is now up more than 50% year-to-date, on pace for its best year since the 1970s. Silver has surged 67%, propelled by robust industrial demand and speculative inflows. With monetary policy expected to ease and inflation still stubborn, investors appear to be rotating from paper assets into tangible stores of value.

And as bullion breaks new ground, Wall Street’s biggest players are finally starting to chase the rally they once dismissed.

Goldman Hikes December 2026 gold price forecast to $4,900

Goldman Sachs has lifted its 2026 gold target to $4,900 per ounce, citing persistent central bank buying, a weaker dollar, and slowing growth. The firm sees structural support for gold as investors diversify away from overvalued equities and long-duration bonds.

The upgrade joins a chorus of bullish calls, echoing Fidelity’s recent $4,000 projection. Both rest on the same premise: real interest rates are staying low while faith in fiat money continues to erode.

For months, markets have treated gold’s rise as a curiosity rather than a warning. But the scale of this move — and the institutional shift behind it — suggests investors are quietly preparing for a longer era of instability. And if the economy is as fragile as new private data implies, those fears may be well placed.

Private Sector Steps In: Carlyle Tracks Weak U.S. Jobs Growth

After President Trump fired the head of the Bureau of Labor Statistics earlier this summer, skepticism about the accuracy of U.S. jobs data has only deepened. With the government still shut down and no official report available, private firms are stepping in to fill the void.

The Carlyle Group’s new proprietary model estimates just 17,000 jobs were created in September — far weaker than prior government trends suggested. ADP’s report shows a 32,000-job loss, while Revelio Labs estimates a modest gain, revealing how unclear the real picture has become.

These independent readings add weight to fears that the labor market is weaker than Washington admits. A softening jobs backdrop could force the Fed into deeper rate cuts — a setup that historically boosts gold as investors seek safety from policy missteps.

As confidence in official data falters, policymakers are turning their attention toward something far more tangible — control over real assets.

Trump Greenlights Alaska Mining Push

President Trump has approved a long-disputed access road to Alaska’s Ambler mining district — a move to unlock domestic supplies of copper and other critical minerals. The executive order includes $35.6 million in U.S. funding for Canada’s Trilogy Metals, giving Washington a 10% stake and warrants for an additional 7.5%.

The Ambler project could become a cornerstone in America’s effort to secure its mineral supply chain and reduce dependence on China. Environmental groups warn of threats to fragile Arctic ecosystems, but for the administration, the calculus is strategic: access to resources equals leverage in a volatile world.

While new supply could pressure some industrial metals in the short run, the bigger picture is clear — nations are racing to secure physical commodities as trust in financial assets weakens. And while Washington shores up its own mineral supply, Beijing is quietly stockpiling the world’s oldest reserve asset.

China’s Central Bank Extends Gold Buying Spree

China’s central bank increased its gold reserves for an 11th straight month in September, extending the longest accumulation streak in over a decade. The People’s Bank of China now holds more than 2,250 tons, solidifying its role as the world’s most consistent sovereign buyer.

This buying spree underscores a global shift in monetary strategy. Central banks — especially across Asia and the Global South — are hedging against dollar dependence and sanctions risk, moving steadily toward hard assets.

The direction of flow has reversed: what was once a westward “gold drain” in the 20th century is now a steady movement east. It’s not just a tactical trade — it’s a structural realignment of monetary power that could define the next financial era.

If 2025 has shown anything, it’s that gold is no longer the alternative — it’s becoming the anchor.

Investing in Physical Metals Made Easy