Published: 02-24-2026, 03:25 pm | Updated: 02-25-2026, 06:36 am

Government debt has become one of the defining financial realities of the modern era. The U.S. national debt recently surpassed $36 trillion, and similar fiscal pressures are mounting across major economies worldwide. For investors, this raises an urgent question: what does rising government debt actually mean for the price and performance of gold and silver?

The short answer is that government debt tends to be bullish for both metals—but the relationship is more nuanced than a simple cause-and-effect. Understanding the mechanisms at work can help you make smarter decisions about whether, when, and how to add precious metals to your portfolio.

What Is the Relationship Between Government Debt and Precious Metals?

The relationship between government debt and precious metals comes down to one concept: confidence.

When investors trust a government’s fiscal discipline and currency stability, paper assets — bonds, cash, equities — tend to perform well. But when that confidence erodes, capital tends to migrate toward assets that sit outside the financial system. Historically, gold and silver have been the primary destination.

Unlike currencies or government bonds, precious metals are not someone else’s liability. They don’t depend on tax revenues, political decisions, or central bank policy to hold their value. That distinction becomes significant during periods of rising sovereign debt — and today, sovereign debt levels globally are at historic highs.

How Rising Government Debt Affects the Economy

When debt grows faster than economic output, governments face a narrow set of options: raise taxes, cut spending, default, or inflate the debt away. Historically, inflation has been the preferred path.

Monetary expansion—whether through quantitative easing, suppressed interest rates, or direct fiscal stimulus—increases the money supply. Over time, this erodes purchasing power. The currency may continue to function, but each unit buys less.

Gold’s supply cannot be expanded by policy decision. It grows slowly through mining, typically 1–2% annually. When fiat currency supply accelerates faster than gold supply, gold tends to reprice higher in currency terms. This is observable history, not theory.

The Financial System Isn’t Safer — And You Know It As risks mount, see why gold and silver are projected to keep shining in 2026 and beyond.

Historical Evidence: Debt, Inflation, and Gold

The 1970s Debt and Inflation Surge

After the U.S. abandoned the gold standard in 1971 and government spending expanded rapidly, inflation accelerated. Gold rose from $35 per ounce at the start of the decade to over $800 by 1980. What looked like a speculative surge was largely a repricing of gold relative to an expanding money supply.

The 2020 Stimulus Era

In 2020, global governments injected trillions of dollars into the financial system in response to the pandemic. U.S. federal debt surged by more than $4 trillion in a single year. Gold gained 25.1% that year; silver rose nearly 47.9%. Capital responded to the scale of monetary expansion.

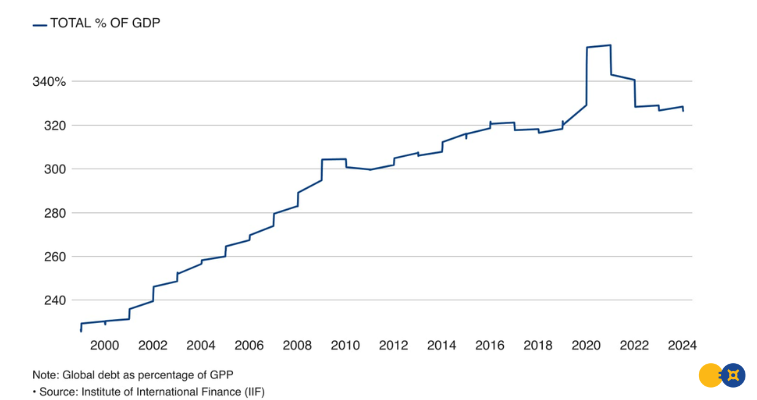

Debt-to-GDP: The Metric That Matters

Investors tracking fiscal sustainability often focus on the debt-to-GDP ratio — the size of government debt relative to economic output. When debt rises faster than GDP, the system tightens:

- Interest payments consume more tax revenue

- Governments borrow to service existing debt

- Central banks face pressure to keep rates artificially low

The United States now carries debt exceeding 120% of GDP. Historically, levels above 90–100% have coincided with slower growth and rising fiscal strain.

But this isn’t just a U.S. story. Globally, total debt has climbed to more than 320% of GDP — nearly double where it stood at the turn of the century.

Global Debt-to-GDP Has Nearly Doubled Since 2000

Source: Institute of International Finance (IIF), via Reuters

When debt reaches these levels, governments rarely default outright. Instead, they lean on financial repression — keeping interest rates below inflation to gradually erode the real value of debt.

And in environments where real returns are suppressed, gold has historically outperformed traditional fixed-income assets.

Real Yields and the Gold-Bond Relationship

Gold does not pay interest. That’s often cited as a drawback. But what matters is real yield — bond returns after inflation.

When real yields are negative, bondholders lose purchasing power. In those periods, gold’s lack of yield becomes irrelevant. If bonds are delivering negative real returns, capital seeks alternatives that preserve value.

Over the past decade, real yields have frequently been near zero or negative, and gold has performed strongly during those stretches. To the extent that debt expansion increases the probability that real yields remain suppressed over the long term, it structurally improves gold’s relative attractiveness as a store of value.

The Safe-Haven Effect: Confidence and Counterparty Risk

Debt impacts gold not only through inflation, but also through confidence. When investors begin questioning a government’s fiscal discipline or a currency’s long-term stability, they look for assets without counterparty risk.

Gold is unique in that regard:

- It is not issued by a government.

- It carries no default risk.

- It does not rely on a financial institution’s solvency.

This is one reason central banks themselves have been accumulating gold in recent years. When sovereign debt levels rise globally, central banks diversify reserves into assets outside the traditional bond system.

When central banks buy gold, they are signaling something important.

Silver’s Dual Role: Monetary and Industrial

Silver historically tracks gold during monetary stress—but often with higher volatility. In addition to its monetary role, silver benefits from industrial demand, particularly in:

- Solar panels

- Electronics

- Electric vehicles

- Grid infrastructure

Large-scale government spending—especially in energy transition and technology—can increase silver demand structurally.

That gives silver two distinct demand drivers: a monetary hedge during inflationary periods, and an industrial component during expansionary fiscal cycles. For investors comfortable with higher volatility, silver can amplify precious metals exposure beyond what gold alone provides.

Has Gold Already Priced In the Debt Risk?

A reasonable concern is whether current gold prices have already reflected the fiscal risks described above. Historically, gold’s major bull markets have coincided with sustained negative real rates, rising debt-to-GDP ratios, weakening currency confidence, and elevated geopolitical tension. To varying degrees, all four conditions are present today.

That doesn’t guarantee near-term price appreciation—markets are complicated, and timing is uncertain. But structurally, the macro backdrop resembles previous multi-year periods of strong precious metals performance, which suggests the underlying case hasn’t been fully arbitraged away.

Putting It in Context

Rising government debt doesn’t automatically cause gold prices to increase. But it does raise the probability of several dynamics that have historically been favorable for precious metals: monetary expansion, persistent inflation, currency depreciation, financial repression, declining real yields, and reduced confidence in sovereign balance sheets.

Gold and silver are among the few asset classes that exist outside this system while remaining deeply integrated into global finance. For long-term investors concerned about purchasing power, that structural position is worth understanding—regardless of what gold’s price is doing in any given quarter.

Stay On Top of Gold & Silver Prices

Get important market alerts sent straight to your inbox.

People Also Ask

Does rising government debt increase gold prices?

Yes. When government debt rises, it typically triggers monetary expansion and inflation, which erodes the purchasing power of paper currency. Investors respond by moving capital into gold—a finite, tangible asset that cannot be devalued—driving its price higher.

Why are gold and silver considered safe-haven assets during debt crises?

Gold and silver carry no counterparty risk—they are not tied to any government’s promise or ability to repay. When confidence in sovereign debt weakens and bond yields turn negative in real terms, investors rotate into precious metals as a reliable store of value outside the financial system.

How does inflation caused by government borrowing affect silver prices?

Government borrowing fuels monetary expansion, which causes inflation. Silver benefits from this environment as a monetary hedge, much like gold. Silver often amplifies gold’s gains during inflationary periods—in 2020, for example, it surged 47.9% compared to gold’s 25.1% as governments unleashed unprecedented stimulus spending.

What historical trends show the link between national debt and precious metals?

Historically, periods of heavy deficit spending and fiscal stress have coincided with strong precious metals performance. Gold rose dramatically through the debt-fueled inflation of the 1970s, and both gold and silver posted significant gains in 2016, 2019, 2020, and 2023—all years marked by expanding government deficits and economic uncertainty.

What percentage of my portfolio should be in gold or silver given high debt levels?

Most financial guidelines suggest allocating 5–15% of a portfolio to precious metals, depending on risk tolerance. Conservative investors typically favor 8–10% in gold with 2–3% in silver. Aggressive investors may hold 3–5% in gold and 7–10% in silver to capture silver’s higher growth potential during periods of fiscal and economic stress.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Past performance is not indicative of future results. Always consult a qualified financial advisor before making investment decisions.

You May Also Like:

- Gold vs Silver: The Liquidity Difference That Matters

- Silver Price Components: Premium, Spot, and Dealer Markup Explained

- Silver Price Forecasts Revisited: Why Wall Street Got It Wrong

- Gold’s Purchasing Power: What One Ounce Buys Over Time

- Why Metals Dominated Every Asset Class in 2025 [and What It Means for 2026]