Published: 07-10-2026, 12:40 pm

HSBC (The Hongkong and Shanghai Banking Corporation) slashed its 2026 average gold forecast by $304 on July 9. It left its year-end target unchanged. That gap between those two numbers tells you more about the HSBC gold price forecast 2026 than the headline cut does.

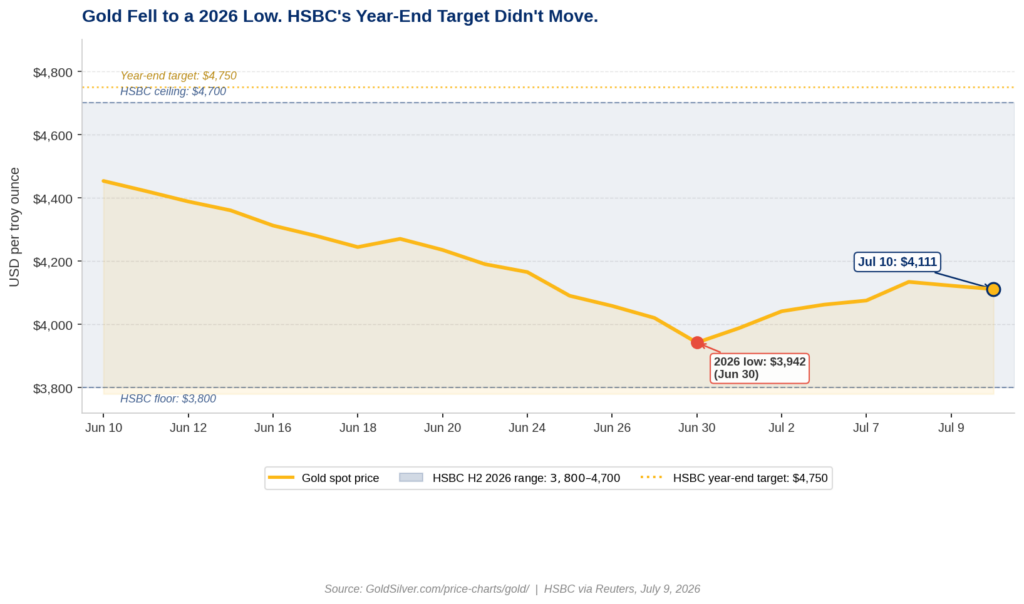

As of Friday, July 10, gold is trading near $4,103 an ounce — down about 0.5% on the day and roughly 27% below January 28’s record high of $5,589.38.

What Did HSBC Change About Its Gold Forecast?

James Steel, HSBC’s Chief Precious Metals Analyst, cut the bank’s 2026 average gold forecast to $4,560 per ounce from $4,864. The 2027 average moved similarly, to $4,925 from $5,000. However, Steel left the 2026 year-end target at $4,750 and the 2027 year-end target at $5,025. Longer-term forecasts for 2028 and 2029 stayed at $5,200 and $5,300 respectively.

The bank now expects gold to trade in a $3,800–$4,700 range through the rest of 2026, then close the year near $4,750.

The stated reason is straightforward. “Changing perceptions of U.S. monetary policy and the impact this had on the dollar are among the central reasons behind further gold liquidation and price declines,” HSBC said via Reuters on July 9. A hawkish Fed tilt raises the opportunity cost of holding a non-yielding asset. Moreover, a stronger dollar makes gold more expensive for international buyers, suppressing demand at the margin.

The Edge Every Investor Needs Smarter precious metals investing starts here. The Nuggets Newsletter brings you essential market insights, Fed updates, global trends, educational videos, and much more.

Why Does the Average-vs-Year-End Gap Matter?

Most coverage focused on the cut. However, the more important data point is what did not change.

HSBC lowered its average forecast — what it expects gold to earn across all H2 trading days. Nevertheless, it held the year-end target nearly intact. In other words, the bank expects gold to spend time near current levels before recovering. The destination, however, has not moved.

Specifically, HSBC did not revise its central bank demand forecast. That figure held at 680 tonnes for 2026 and 850 tonnes for 2027. Furthermore, Steel said heavy gold ETF liquidation from the first half of 2026 may partially reverse in H2 as structural supports reassert themselves. Those supports include rising fiscal deficits globally and ongoing sovereign debt market pressures. The analyst was also explicit that the current conflict is not a permanent headwind. “We do not believe Iran-related declines by themselves would be long lasting,” Steel said. Consequently, downside risk may be more limited than the headline cut implies.

What Does This Mean for Gold’s Structural Case?

The HSBC revision is a timing adjustment, not a thesis reversal.

Specifically, the structural forces that drove gold from around $2,600 in late 2024 to a January 2026 record — fiscal deficits, central bank diversification away from US Treasuries, and the de-dollarization trend — remained explicitly in HSBC’s reasoning as future supports. In contrast, those long-horizon forecasts for 2028 and 2029 were not touched.

Bank of America made the same move recently, trimming near-term numbers while preserving the structural outlook. When multiple major institutions lower their average forecast and hold their year-end target simultaneously, the message is consistent: the path has become harder, but the direction has not changed.

As a result, the structural trap is still in place. Real yields are elevated today. Yet the US fiscal trajectory requires continuous Treasury issuance at record scale. That limits how long truly restrictive rates can hold before they become self-defeating. Importantly, gold’s role as the asset that sits outside this system remains unchanged.

Two Dates Will Decide Which End of HSBC’s Range Gold Tests

The most important near-term catalyst is the June CPI report, due Monday, July 14. A cooler headline reading — made more likely by the recent correction in oil prices — would reduce market pricing for a September Fed rate hike. Markets are currently pricing roughly even odds of a September hike, according to CME FedWatch data. Lower rate-hike odds compress gold’s opportunity cost directly, which is the mechanism HSBC’s year-end recovery scenario relies on.

The July 28–29 FOMC meeting is the second date on the clock. That context was already established by the FOMC minutes released Wednesday. Together, those two events will largely determine whether gold tests the upper or lower end of HSBC’s $3,800–$4,700 range. Notably, HSBC’s year-end view is $4,750 — about 16% above where gold trades today. That is the number Steel did not change.

Stay On Top of Gold & Silver Prices

Get important market alerts sent straight to your inbox.

SOURCES

1. Reuters — HSBC lowers 2026-27 gold price forecasts on hawkish Fed tilt, July 9, 2026

2. World Gold Council — Gold Demand Trends Q1 2026, April 29, 2026

3. CME Group — FedWatch Tool, September 2026 rate probabilities, accessed July 10, 2026

4. GoldSilver.com — Live Gold Price Charts, July 10, 2026

Disclaimer: This article is for informational purposes only and does not constitute financial or investment advice. Always consult a qualified financial adviser before making investment decisions.

You May Also Like:

- The Fed Named AI Its Top Inflation Risk. Gold Noticed.

- Five Days From Now, Two Numbers Will Decide Gold’s Second Half

- Bank of America Cut Its Gold Forecast. The Reason Is More Bullish Than It Looks.

- The Fed Is Split 9 to 8. Gold and Silver Are Paying the Price — Until July 14.

- Gold Is Sitting on $4,000. The World Gold Council Has a Model for What Happens Next.

- Trump Called the Deal Dead. Oil Jumped 6%. Gold Fell. Here Is Why Both Moves Make Perfect Sense.