Written by: The MacroButler

Beyond the fading grandeur of the G7 and G20—clubs of nations forged in the aftermath of World War II and now mired in economic stagnation and demographic decay—a new alliance has emerged on the geoeconomic map: BRICS+.

This coalition—Brazil, Russia, India, China, and South Africa—represents a rising league of nations determined to expand their trade influence, secure resource flows, and accumulate the economic surpluses that once enriched Europe’s great empires.

First conceived in 2001 by ‘Government Sachs’ economist Jim O’Neill as “BRIC,” the term began as a mere market classification for economies whose growth threatened to redraw the balance of global commerce. But what began as a banker’s shorthand swiftly became a council of ambition. By 2006, the original four were already meeting to strengthen commercial ties, coordinate investment, and align political strategies. In 2009, their first official summit in Yekaterinburg marked more than diplomacy—it signalled the return of a multipolar world, where the trade routes, resources, and bullion no longer flowed solely to the old imperial capitals, but to new centres of wealth creation.

In 2010, South Africa was brought into the fold, transforming BRIC into BRICS and extending the league’s reach to Africa’s mineral-rich shores. From that moment, BRICS matured from a market label into a trading and political bloc with imperial ambitions of its own—determined to tilt the scales of global commerce away from Western monopolies, rewrite the rules of finance, and channel trade and investment flows along routes they control, not those dictated by the G7, the G20, the IMF, or the World Bank.

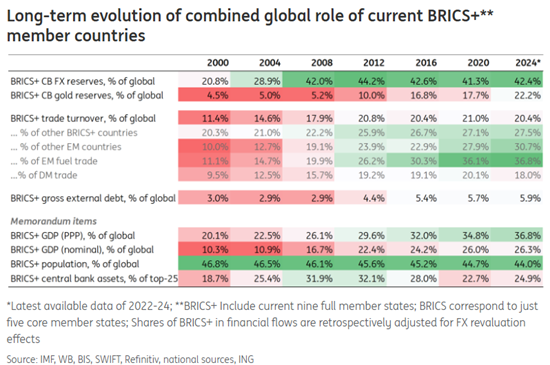

By 2025, BRICS had grown into BRICS+, a formidable trading confederation of eleven full members—Brazil, Russia, India, China, South Africa, Saudi Arabia, Egypt, the United Arab Emirates, Ethiopia, Indonesia, and Iran—controlling vast reserves of commodities and strategic goods, alongside the markets and labour forces to refine and consume them. Further expanding its reach, the bloc introduced a new “partner country” category on January 1, 2025, bringing Belarus, Bolivia, Cuba, Kazakhstan, Malaysia, Thailand, Uganda, Uzbekistan, and Nigeria into its orbit. While not full members, these partners now participate in BRICS+ summits and ministerial meetings, and may endorse the bloc’s declarations, deepening their integration into its growing sphere of economic and political influence.

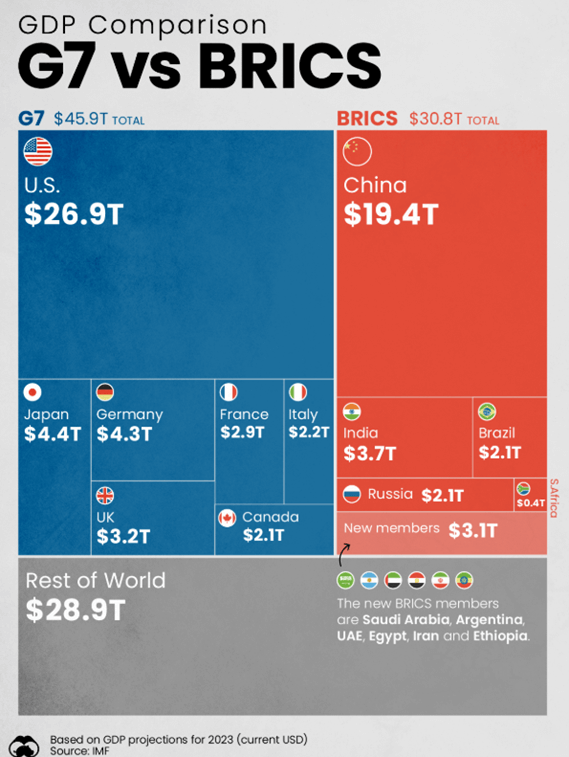

Together, these nations now command roughly 40% of global output in purchasing power terms, according to IMF figures from April 2025—surpassing the economic might of the old developed market powers in key arenas of trade and production. By year’s end, their share is set to climb to 41%, leaving the G7’s diminished 28% in their wake. The tide of bullion, commodities, and commerce is no longer flowing to the aging imperial ports of the West, but toward a rising consortium of resource-laden, market-hardened economies intent on securing the world’s wealth under their own flags.

In population terms, the BRICS command over 40% of the world’s people—a share that swells to an estimated 55.6% when their partner states, known collectively as BRICS+, are counted. This vast reservoir of labour, consumers, and soldiers of commerce forms the backbone of the bloc’s expanding economic power, ensuring that its markets grow not merely through trade, but through the sheer demographic force that has always underpinned great mercantile empires.

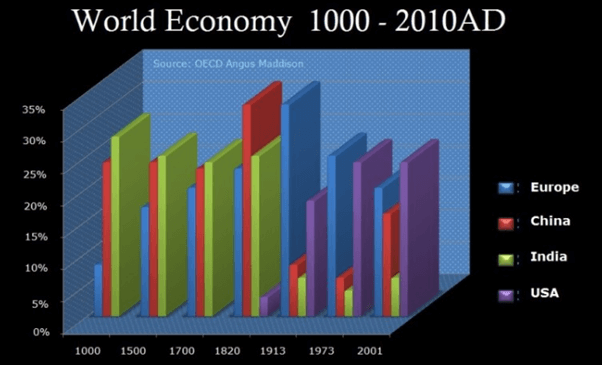

If you’ve read a bit of history—or even just skimmed the CliffsNotes—you know the U.S. and the West haven’t been calling the economic shots forever. The global crown has passed through more hands than a cheap bottle of wine: Mesopotamia, Egypt, Persia, Greece, Rome, China, the Caliphates, Portugal, Spain, the Netherlands, Britain… all took their turn strutting on the world stage before bowing out. Now BRICS+—Brazil, Russia, India, China, and South Africa—are lining up for their shot. And if history teaches us anything, it’s that the economic game of musical chairs never really ends—someone’s always about to grab the seat, and someone else is about to hit the floor.

When great powers start fearing the future, the script rarely changes—they stagnate, sulk, and fade. Ming China once thought it had reached eternal perfection, so it banned ocean voyages, shunned foreign trade, and replaced science with Confucian trivia. Meanwhile, Europe was busy tripping over the New World and inventing trading empires. Fast forward to today, and America seems to be auditioning for a Ming Dynasty reboot—unable to finance domestic infrastructure costs, allergic to global trade, and comforted by the idea that being top dog last century guarantees the same this one. History suggests otherwise.

Americans have spent decades in a 2% growth bubble—enough to quadruple living standards over a lifetime, but slow enough that any five-year stretch feels like watching paint dry, punctuated only by random disasters. Lose your job, your house value, or a government contract, and years of “progress” vanish. No wonder change feels like a threat. In the U.S., new tech means layoffs—encyclopaedia salesmen, carmakers, flip-phone giants, floor traders—one innovation at a time. In modern China, it’s the opposite: tech has been a golden escalator, lifting almost everyone up so fast that losing a job often just means finding a better one. The result? Americans see change as a wrecking ball; the Chinese see it as a construction crane.

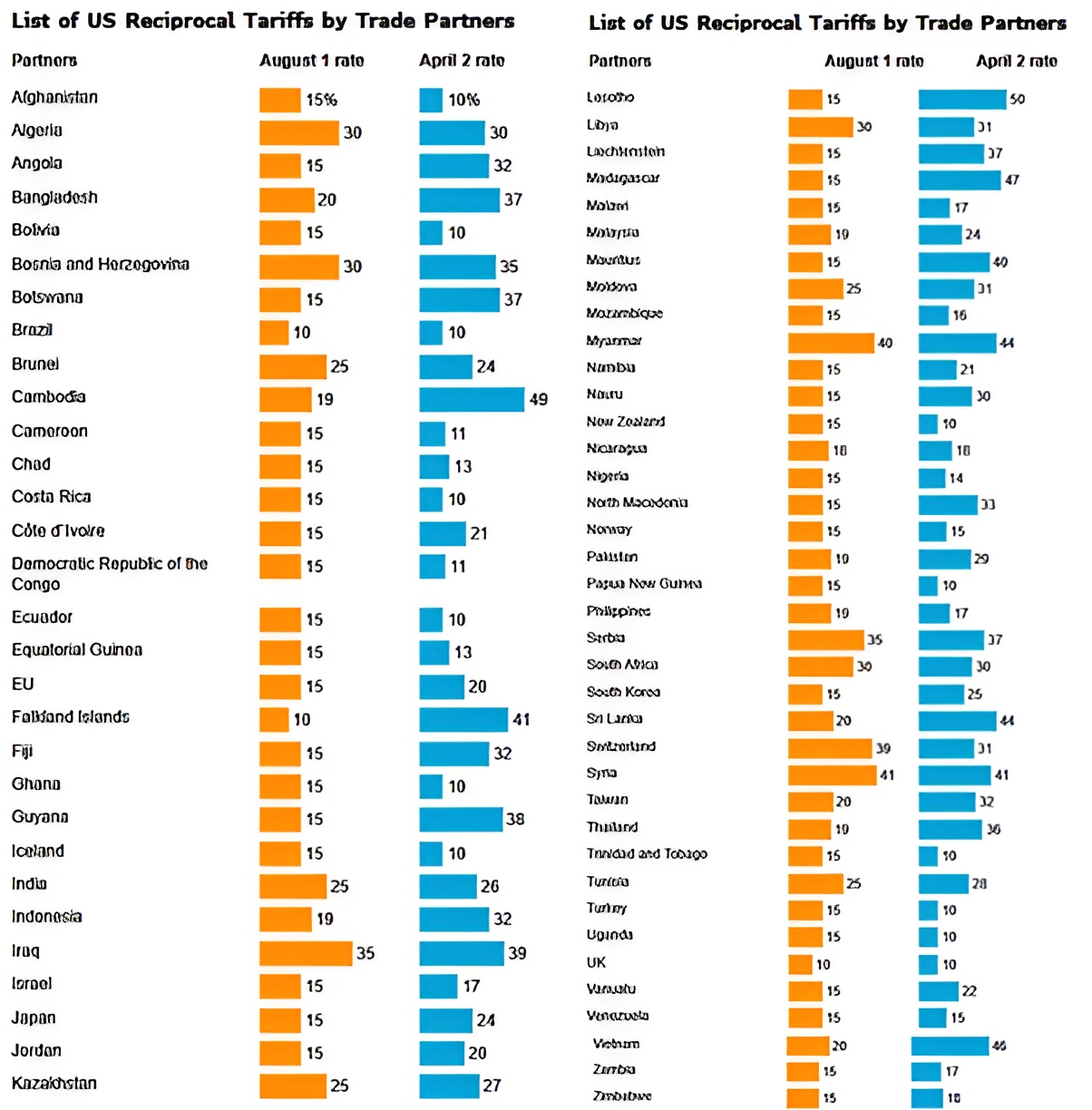

On August 7th, Donald Copperfield waved his magic tariff wand once again, proving tariffs aren’t just economic tools anymore—they’re geopolitical weapons aimed at BRICS and anyone daring to say “no thanks” to ‘Trumperialism’. Apparently, the Washington swamp’s favourite pastime remains spreading chaos under the guise of a Malthusian depopulation agenda, all while slapping new tariffs on the globe. Starting August 8th at midnight ET, planet earth braced itself for a 10% global minimum tariff on imports. Canada’s tariff jumped from 25% to 35%—unless you’re playing nice under USMCA. Switzerland got hit harder, up to 39%, causing some diplomatic huffing. Meanwhile, 40 countries got a 15% slap, a dozen-plus economies faced even nastier hikes, and China and Mexico got a 90-day stay of execution. Tariffs: the world’s new favourite geopolitical toy.

The rise of BRICS+ was practically scripted by the Biden administration’s move to kick Russia off the SWIFT system—a clear message that the U.S. is acting like the world’s financial dictator: comply or get cut off. Threatening China with the same fate if it helped Russia only accelerated BRICS’ birth as a geopolitical counterstrike. The plan to bankrupt Russia with sanctions backfired spectacularly. China dumped U.S. debt, and the Global South caught on—U.S. financial hegemony isn’t just wielded; it’s weaponized. The so-called GENIUS Act? Just the latest chapter in the “control the money, control the world” playbook, this time with a QR code. Meanwhile, Europe, the U.S., and allies booted several Russian banks from SWIFT in early 2022—except Gazprombank, because Europe still needs its Russian gas. The attempt to isolate Russia only fuelled a new economic bloc determined to break the dollar’s stranglehold—and rewrite the global order.

The self-anointed “Peacemaker in Chief,” who in truth is the “Warmonger in Chief,” claws desperately to crush BRICS+ and cling to the dollar’s fading throne—a laughable charade. You can’t drag nations to your dark altar with threats and expect them to leap blindly into your abyss. BRICS+ rose like a phoenix from the ashes of these Neocon iron fists, the true puppeteers of U.S. foreign policy. Meanwhile, those who have played the revolving door game between Government Sachs and the US institutions pop champagne, basking in the chaos as the ‘Manipulator In Chief’ dances to their sinister tune, a marionette bound to their infernal rulebook as ‘Government Sachs’ and other are looking to seize the resources of the Global South as they tried to on the eve of the Asian Financial Crisis in 1998.

The Neocon bill—shamelessly backed by ruthless, un-American operatives from both parties—is a dark threat looming over international security. It hasn’t passed yet, but any lawmaker who supports it deserves to be dragged out screaming, for they serve masters, not the people. Alongside this nightmare lurks the Trade Review Act of 2025, aiming to shackle tariffs with congressional chains—though the White House snarls with veto threats. Meanwhile, courts unravel the twisted legality of Trump’s tariffs, slapped on under a dubious emergency law. Judges, from both sides, see this as a monstrous power grab—the likes of which hasn’t been witnessed in two centuries.

As holding USD assets suddenly turned into a geopolitical headache, it’s no shock that BRICS countries started dumping their U.S. Treasury holdings faster than you can say “unreliable trade partner.” After all, why stick around when the U.S. might just confiscate your assets on a whim for not toeing their “American way or the highway” agenda? Especially when that agenda conveniently involves stealing resources from rebellious countries like Russia—those brave souls who dare to question the Malthusian depopulation plans cooked up by the American plutocracy. Who wouldn’t want out of that party?

US Treasury Holdings by Russia (blue line); China (red line); India (Yellow line); Brazil (green line); South Africa (purple line).

The runner-up to the U.S. dollar in BRICS+ FX reserves is basically a mixed bag of other developed-market currencies, holding a combined 35% slice of the pie—while non-DM currencies barely make a dent. One big hang-up? BRICS+ countries have just 6% of the world’s external debt compared to the U.S.’s hefty 21%, making it tough for their currencies to go global.

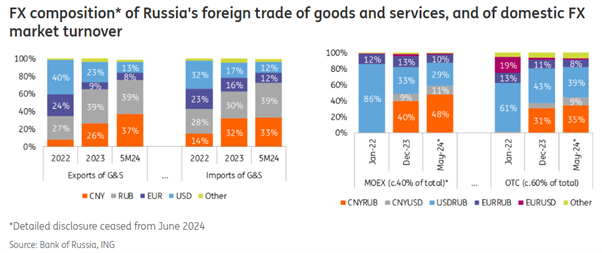

On the trade front, BRICS+ moves a solid 20-21% of global trade—about $10 trillion a year—but growth stalled after the financial crisis thanks to China’s slowdown and falling oil prices. Still, the bloc’s members are cozying up, with intra-BRICS trade climbing from 22% in 2008 to 28% now, and emerging markets trading with them even more. Fuel trade is the real star, doubling BRICS+’s share to 37%, making energy the prime playground for de-dollarisation. With non-OECD oil demand now at 55% of the global total, who pays in what currency matters. While solid stats are scarce, anecdotal reports show renminbi, UAE dirham, and rupees being tossed around for energy deals. India now pays Russia in Rubles and rupees. The renminbi’s the real heavyweight here—Russia’s foreign trade now prefers it over the dollar, thanks to the Bank of Russia stocking up on yuan, which made up 22% of its FX reserves. So, watch this space—BRICS+ might just pull off the ultimate currency mic drop.

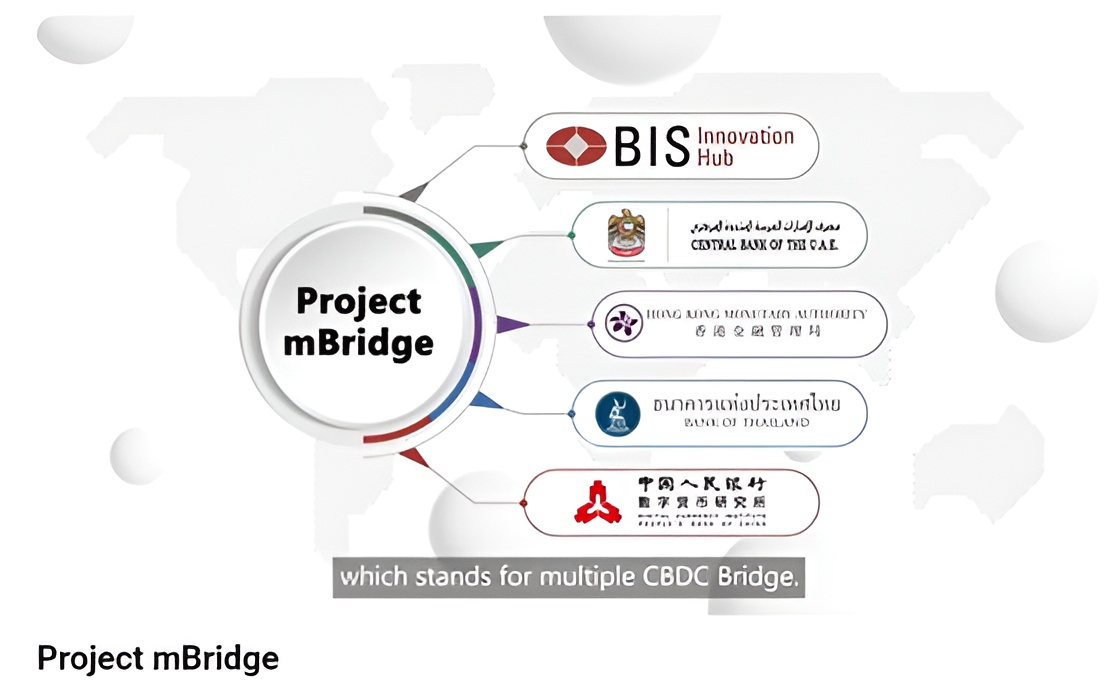

When BRICS talks about dumping the dollar, the m-Bridge project often gets name-dropped—a fancy digital money highway led by the BIS and central banks from China, Hong Kong, UAE, and Thailand. It uses wholesale CBDCs to make big cross-border payments faster, cheaper, and nonstop. By bypassing the traditional correspondent banking network—which often routes payments through the U.S. dollar and American banks SWIFT maze—m-Bridge seeks to reduce reliance on the dollar in global trade settlements. The tech works, but getting all the banks and regulators to agree and play nice? That’s the real challenge. After three years, they’ve barely rolled out a basic version. So yes, m-Bridge could one day shake the dollar’s throne—but don’t hold your breath. The revolution’s cooking, but it’s a slow simmer.

Lots of chatter about a BRICS currency to dethrone the dollar—but don’t hold your breath. First, BRICS aren’t signing up for the globalist playbook the West’s been pushing since WWII. Second, they’ve all seen how the euro turned into a sovereignty-sapping headache, with looming debt defaults all over Europe. And third, they’re not exactly marching in sync—China’s been stuck in deflation since COVID, while Brazil and India wrestle with stubborn inflation, which they actually use to weaken their currencies against the dollar and manage debt. So yeah, a unified BRICS currency? Not anytime soon.

CPI YoY Change in Russia (blue line); China (red line); India (Yellow line); Brazil (green line); South Africa (purple line).

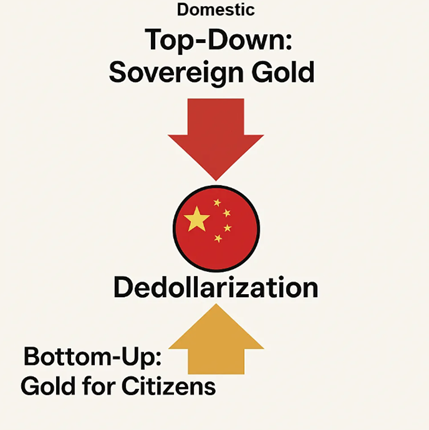

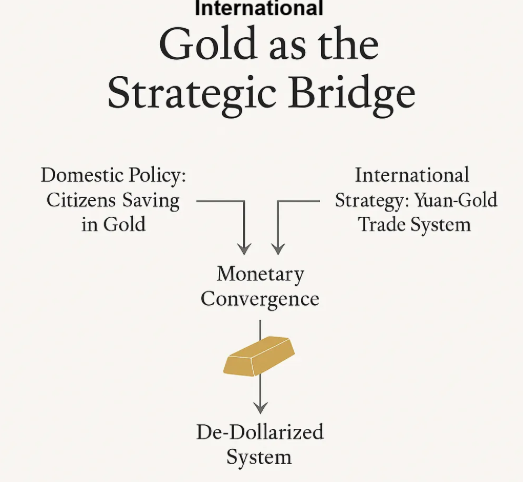

Instead of pushing for a BRICS currency or just switching to the yuan as the new reserve currency, the savvy Chinese leaders who get the headache of owning the world’s reserve currency is quietly steering its people and government away from the U.S. dollar. Citizens are being nudged to buy gold, while the state builds a parallel trade and finance system that skips the dollar altogether. The plan? Two separate tracks converging: a gold-backed domestic savings base meets a yuan-powered foreign trade engine, creating a new, stable financial middle ground.

Unlike the US which just passed the ‘Genius Act’ to finance its forever wars and spread its Malthusian agenda, China has aligned its goals with its people’s interests. It’s pushing the yuan for trade with Belt and Road countries, while promoting gold savings domestically. Internationally, gold acts as a guarantee for partners accepting the yuan. This gold-yuan combo forms a bridge between national ambitions and global trade. BRICS countries are nudged toward a yuan-based system: sell raw materials, get paid in yuan, then buy finished goods from China—closing the loop. If successful, China will issue yuan bonds to foreigners, paying interest tied to gold’s value as a hedge against currency debasement.

Think Bretton Woods 2 was the world on the USD standard backed by US gold? Bretton Woods 3 is BRICS on the RMB standard, with China on a gold-convertible standard.

It’s basically a reboot of what the US did post-WWII—building economies and influence by tying the world to its currency backed by gold. But China’s tweak? No fixed gold price and decentralized gold storage. Smart moves designed to dodge the pitfalls that sank Bretton Woods 2.

BRICS countries will get to peg their currencies to gold, the yuan, or whatever floats their boat. The yuan acts as the medium of exchange, while gold serves as the ultimate store of value. The system’s design nudges countries onto one of two paths: invest in your own economy and watch your currency strengthen or stick to exporting raw materials and become China’s economic satellite.

It will be probably voluntary—but don’t kid yourself, the pressure’s real. Build your industry, and China becomes your partner: infrastructure, goods, investment, the whole package. Ignore that, and you’re stuck dependent, much like how the US rebuilt Germany and Japan after WWII—except now China’s the one doing the financing and franchising.

China’s playing the long game at home too. It’s letting people buy gold, offering gold-linked savings accounts, and pushing gold-backed investment products. Next up? Bonds backed by gold collateral. The goal: build trust in the financial system—and reward that trust with profits. As long as the U.S. keeps looking like a threat and the Chinese government doesn’t mess up, that trust will keep growing.

Internationally, China’s opening its bond market to foreign yuan holders, with returns pegged to gold to hedge against debasement. The cycle is simple: sell resources for yuan, fall back on gold as a safety net, invest in Chinese bonds, and buy Chinese goods. Sound familiar? It’s basically WWII’s Marshall Plan 2.0.

China’s also clever about keeping high-margin manufacturing at home, selling finished goods abroad, and controlling the value in the supply chain—not just raw materials.

Gold is the glue: it reassures other countries, keeps domestic folks loyal, and steadies the ship as the dollar fades. Eventually, the plan is to shift from gold to yuan once the yuan earns enough trust—then maybe ditch gold if the time’s right. Remember, China invented abstract money and had markets before capitalism was even a thing—they’re not playing dumb.

This isn’t some secret plot—it’s history repeating. Major money system shifts follow wars. Today’s battlefield? Trade deals, savings, and bonds. The blueprint is in motion.

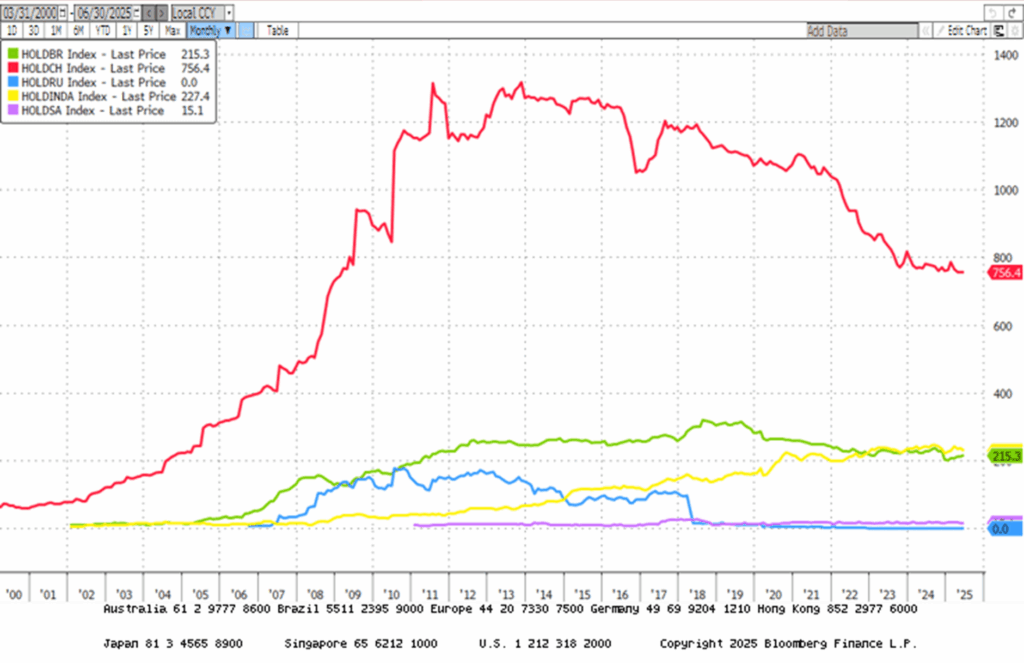

The BRICS didn’t exactly wait around for the “Manipulator In Chief” to sprinkle extra tariffs like confetti before dialling down their love affair with U.S. Treasuries. Nope, they started ghosting Uncle Sam’s trade party way back in 2018 during the first act of “Donald Copperfield.” Guess they saw the tariff magic coming and decided to pull a disappearing act early!

Exports from Russia (blue line); China (red line); India (Yellow line); Brazil (green line); South Africa (purple line) into the US.

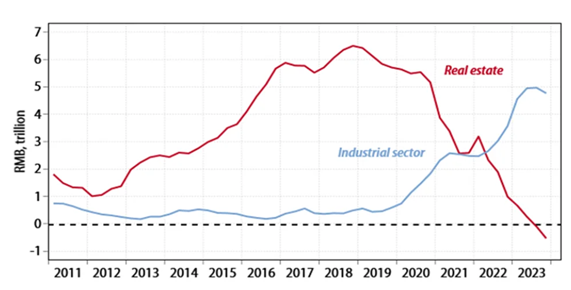

For all the Western “China experts” who’ve never set foot in the Middle Kingdom and churn out papers from their cozy Texan offices: stop obsessing over China’s real estate crisis as if it’s the apocalypse. Unlike the U.S., Chinese companies lean on bank loans—not fickle financial markets—for growth. Since 2019, Beijing has redirected lending from real estate to high-tech industries like EVs, AI, and machinery, spawning global players like BYD, Huawei, and Zoomlion that crush Western competitors on price and quality. Meanwhile, the “real estate crisis” that supposedly dooms China? Beijing doesn’t even blink—Chinese folks are housed, banks are state-controlled, and the government is gearing up for an industrial Blitzkrieg. Meanwhile, the western world is still stuck waiting for the Germans to come through the Maginot Line, distracted by “saving the planet” while China speeds ahead.

For those in the West still clinging to the fantasy that Asia is stuck in trishaws and rice paddies, the 2025 World Robot Conference in Beijing should’ve been a rude awakening—showcasing companies like Unitree, whose humanoid robots outpace anything coming from the U.S., including the pet project of its very own ex–American Rasputin.

Though lacking centralized political power, BRICS+ undeniably hinges on the rise of the Russia-China-India triumvirate—mixing Russia’s vast, cheap natural resources, China’s cutting-edge manufacturing prowess, and India’s booming, hungry consumer market. Together, they form a mercantilist powerhouse that’s reshaping the global economic game.

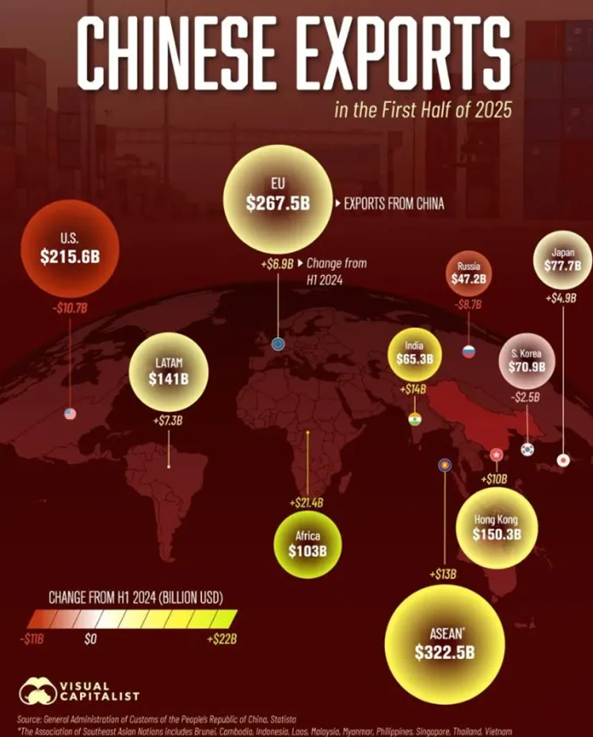

In the first half of 2025, China’s exports tell a story: the Global South is now the hottest dance floor, while the West is sitting out. ASEAN leads the party with $322.5B in imports, Africa’s exports surged by $21.4B, India’s shopping spree grew by $14B, and Latin America kept the rhythm going with $7.3B more. Meanwhile, the U.S. and Wester Europe are showing the cold shoulder. China’s clearly hedging its bets, cozying up to resource-rich, less picky partners in the Global South to dodge Western trade tantrums. It’s a savvy geopolitical pivot—less drama, more diversified shopping carts. Looks like the future of Chinese exports isn’t Wall Street, it’s Main Street… somewhere around the equator.

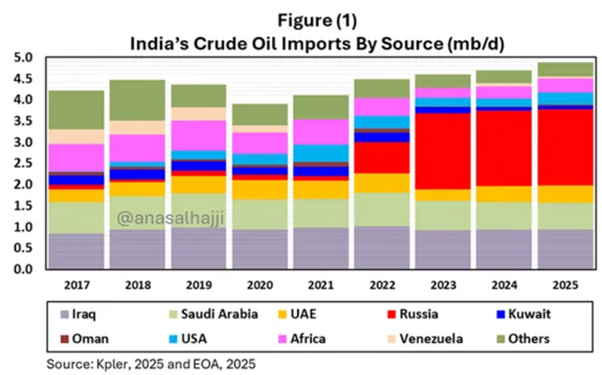

So, while cutting back on trade with the U.S. and even Europe, BRICS+ nations are cozying up and trading more with each other. Take India’s love affair with Russian oil: imports skyrocketed from a modest 68,000 barrels per day pre-USD weaponization to over 2 million—because why pay full price when you can snag a discount? Nearly 40% of India’s crude now comes from Russia, at $10–$20 cheaper per barrel than Middle Eastern oil. Meanwhile, U.S.-India trade hits $118 billion, with the U.S. running a $45 billion deficit—so sure, slap on tariffs and threaten jobs, but India’s smirking behind the scenes. China’s still guzzling Russian oil too, and other Asian exporters can’t fill the void. G7 and EU sanctions may have rerouted oil flows but didn’t crimp global supply or demand, especially not in India. India oil imports from Russia grew steadily, replacing expensive, high-shipping-cost crude from the U.S., Africa, and South America. Most of the Russian discounts come from shipping headaches, not refinery sweetheart deals. Indeed, India swapped pricey imports from afar for cheaper Russian barrels closer to home—making the sanctions and U.S. threats look like a pricey game of musical chairs nobody wanted to play.

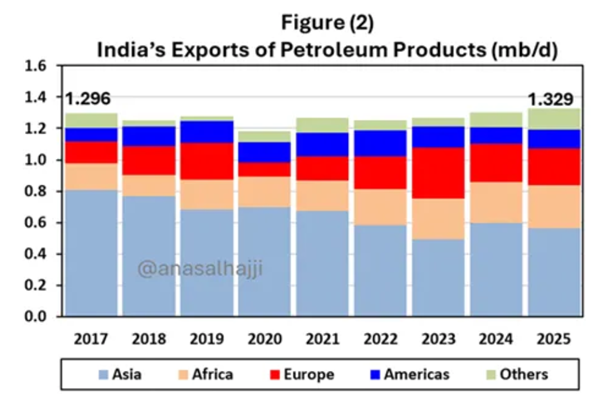

A popular myth among western warmongers claims India is importing tons of Russian crude just to refine and export petroleum products. But the facts say otherwise: India’s petroleum product exports today are pretty much the same as in 2019—long before Russia invaded Ukraine. In fact, there has been a subtle shuffle rather than a surge: exports to Europe have gone up to replace Russian products banned by the EU in early 2023, while exports to Asia slipped. As Europe slowed and got picky about anything linked to Russian oil, Indian refiners found new customers in Africa and elsewhere. If the EU tightens the ban, expect Indian products to shift further toward the Middle East and Africa. Plus, Indian refineries can easily prove they’re using non-Russian crude, since they import plenty from other countries already. Interestingly, the G7/EU sanctions on Russian crude in late 2022 allowed imports of modified Russian oil—like refined products—so Indian exports to the EU and US still follow the rules. Meanwhile, new refineries in Kuwait, UAE, and Oman have stepped in to serve Asian markets that Indian exports used to cover. So, no conspiracy here—just a global game of supply chain musical chairs.

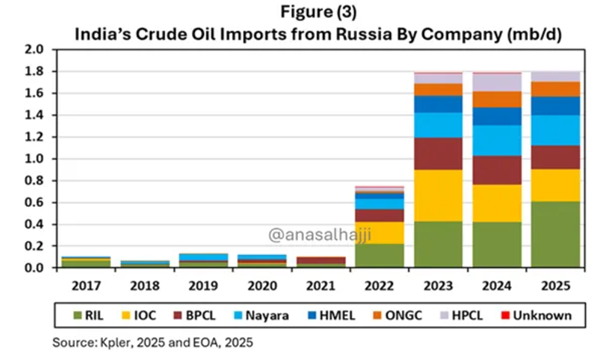

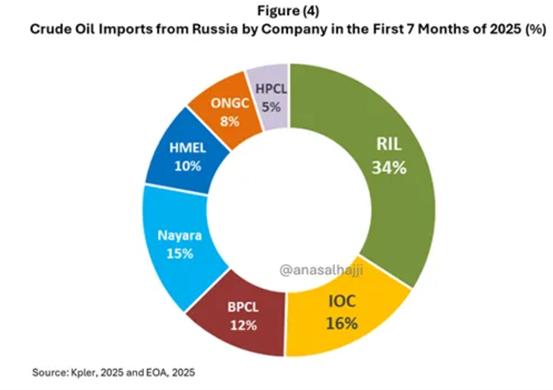

Another myth floating around is that only India’s private companies import Russian crude. Nope—both private and government-owned refiners have been loading up on Russian oil since the Ukraine invasion. So, it’s a team effort, not a private party.

Here’s the scoop: private companies handle about 60% of India’s Russian crude imports, with government-owned firms picking up the rest. Reliance Industries (RIL) alone accounts for roughly a third of the total. On the government side, Indian Oil Corporation (IOC) brings in 16%, Bharat Petroleum Corporation (BPCL) 12%, and Oil and Natural Gas Corporation (ONGC) 8%, with its subsidiary HPCL at 5%. Private players Nayara and HMEL chip in 15% and 10%, respectively. The bottom line? Almost every Indian refiner has a piece of the Russian crude pie.

Another classic case of BRICS mercantilism cashing in on the U.S. “tarrified” mess is how China and Brazil reorganized the coffee supply chain amid increasing tariffs from Donald Copperfield. After the ‘Manipulator in Chief’ slapped Brazil—the biggest South American economy—with 50% tariffs on key goods, China didn’t waste a second. Instead, it jumped in to cozy up to Brazil’s coffee industry, one of the hardest-hit sectors since the U.S. has long been the world’s top coffee buyer. China even flexed its support by granting export permits to 183 new Brazilian coffee companies for five years—because apparently, coffee is becoming China’s new daily essential. Meanwhile, Brazil’s President Lula isn’t shy about calling his BRICS buddies for backup—Xi Jinping, Modi, and Putin. China’s Foreign Minister Wang Yi didn’t hold back either, calling U.S. tariffs “bullying,” a violation of UN and WTO rules, and promising to ramp up cooperation with Global South allies. Lula even proposed a BRICS summit to respond jointly to these tariffs, telling the ‘Bully In Chief’ he’s no “emperor of the world,” despite his world-domination fantasies.

To wage commerce among themselves, BRICS+ nations must secure the battlefield of trade beyond the reach of Western Malthusians, whose strategy is to sabotage their rise as a new mercantilist stronghold of prosperity.

When water is blocked, it seeks another path; when a road is barred, the wise traveller turns his steps elsewhere. So, it is with nations. Mahan taught that mastery of the seas is mastery of the world, for ships carry the lifeblood of trade, and trade begets wealth, and wealth begets power. For a century, the Anglo-American world rode upon these waves, their fleets guarding the sea lanes, their currencies ruling the markets. Yet the ocean, vast as it is, is but one face of the earth. Mackinder saw another truth: that the land, the “World Island” of Eurasia, is the axle upon which history turns. Railways, rivers, and roads bind its riches together, and whoever binds them under his rule may command the world without setting sail.

In our time, the U.S. has sought to lock China within the bars of its island chains, hemming it in like a bird in a gilded cage. But the dragon does not beat its wings against the bars—it burrows through the earth. With the Belt and Road, China lays steel rails, pours concrete, and spins fibre across continents, weaving a net of influence that stretches from the Heartland to distant shores. Thus, as the sea powers guard the tides, the land power builds its road, and the contest of empires flows on, like two rivers racing toward the same sea.

And then there’s Russia.

After the 2022 invasion of Ukraine, the West unleashed its full arsenal of sanctions—no dollars, no euros, no Swift, no tank parts, no chips, no Davos champagne toasts. In short, an attempt to exile Moscow from the ocean-based, dollar-dominated system. Russia’s answer? Double down on Mackinder’s vision—land power over sea power—by turning to its vast network of rivers. The Volga, the Don, the Ob, the Lena—names rarely heard in discussions of global commerce—are being linked with ports, canals, and railways to knit together a Eurasian trade artery that bypasses Western-controlled seas. In doing so, Moscow isn’t just surviving sanctions—it’s redrawing the map of Eurasian connectivity.

When the river meets the mountain, both find their course: China brings wealth and vision, Russia brings land and resources. Together, they weave roads, rails, and rivers into a web the seas cannot touch, shaping a trade realm beyond the reach of navies and sanctions. In this meeting of Heartland and ambition, the map of influence is redrawn—not by conquest, but by connection.

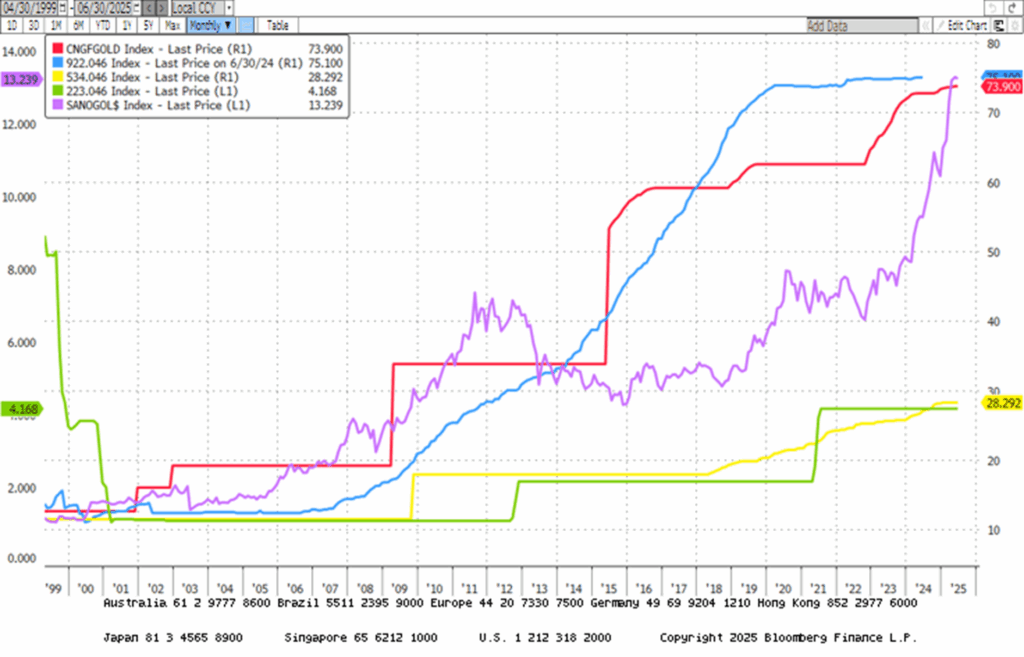

In short, BRICS+ are just doing what economics 101 teaches—playing to their strengths and trading smart. Since 2022, they’ve also been on a gold-buying spree, now hoarding over 20% of the world’s gold. Q2 2025 saw a 41% jump in gold grabs, as these countries ditch the U.S. dollar and chase financial freedom. Russia and China are the golden heavyweights, holding nearly three-quarters of BRICS’ stash. With over 10 new members joining in 2025, BRICS is turning the global financial game into a multipolar showdown, trading more in non-dollar currencies. Gold prices are hitting record highs thanks to global drama and diversification fever. Even India’s jumping on the bandwagon, adding 19.2 tonnes last year, because when the money gets messy, shiny metal feels like a safe bet.

Gold Reserves in troy ounces in Russia (blue line); China (red line); India (Yellow line); Brazil (green line); South Africa (purple line).

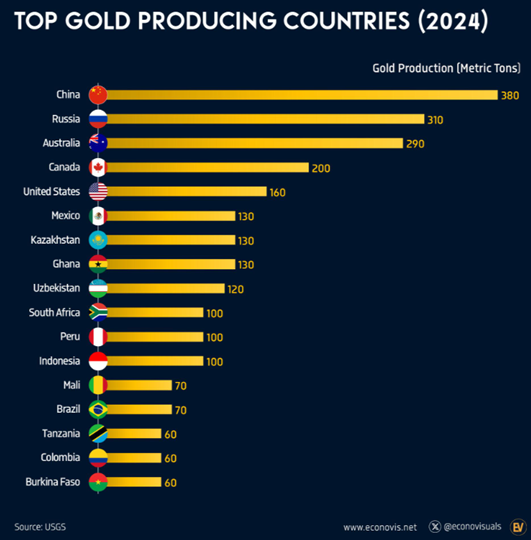

Not only are BRICS and their new members busy piling up gold reserves while ditching US Treasuries, but few in the West realize they also sit on some of the biggest gold deposits on the planet—making them top gold producers too. Talk about having your shiny cake and eating it!

From the geopolitical theatre standpoint, China’s made it clear: Russia won’t lose, because next up might be them. The only defence against reckless Neocons is a united front—Russia, China, India, and others standing strong against the West. India and China once ruled global finance; Europe lost that after two world wars. The endless wars these Neocons wage? They lose every time. They think it’s just a Russia fight, and China can wait its turn. Nope. This is a showdown with NATO, and the rest of the world tired of Neocon arrogance is ready to rewrite the rules once World War 3 ends.

These delusional warmongers are the ultimate armchair warriors—full of swagger but never stepping onto the battlefield themselves. Instead, they happily send everyone else’s kids to fight and die for their grandiose dreams of global domination and glory. Ironically, they’re chasing the very conquest they accuse others of pursuing. Their usual narrative? Russia is on the ropes, about to be squashed like an insignificant ant. Reality? Not so much.

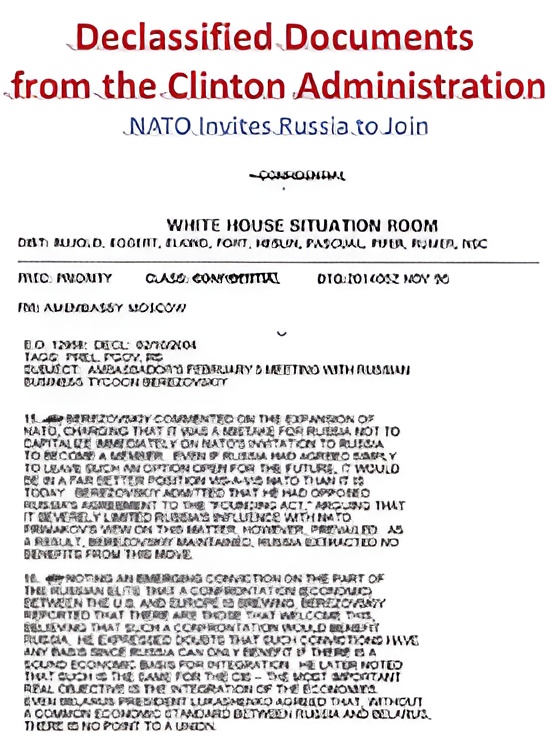

The fake news media has been the drumbeat behind EVERY SINGLE WAR—because, well, that’s their job. Even Tulsi Gabbard exposed that the CIA’s Project Mockingbird is still alive and kicking, with its army of “journalists” peddling lies. Take the recent papers that bust the myth of Putin as just another oligarch. The reality is that, in 2000, when the plot was to seize control by blackmailing Yeltsin into appointing their puppet Boris Berezovsky, a well-known scam was in play, ‘Government Sachs’ and its Wall Street peers were looking to loot Russia’s natural resources.

The “oligarchs’ puppet” Putin myth—pure fantasy. Unlike the Western warmongers of NATO and the Washington swamp pushing global depopulation, Putin and Xi actually know how to restrain and negotiate for their mercantilist agenda. Declassified Clinton-era docs show Berezovsky wasn’t even into Putin—he preferred Igor Ivanov. Putin barely knew Berezovsky, and the oligarchs had no real hold on him. They just needed a loyal stooge to protect Yeltsin’s crew from jail time. Enter Putin, who promptly told the oligarchs to keep their money but get out of politics—then locked up or exiled the troublemakers. Now, the oligarchs left are state made, like Rotenberg and Timchenko, cozy with Putin, not puppet masters. So no, Putin wasn’t their creation—he’s the one holding the strings, while the West keeps flailing around like a spoiled child.

The only silver lining in this insane rhetoric? Maybe Europeans will finally get off their couches and demand real political change—because without it, no TV shows next year. Has Donald Copperfield figured out Europe will NEVER make peace with Russia, so he’s just playing along to sell World War III? Honestly, that’s the best-case scenario. Otherwise, if nuclear war breaks out, forget the fancy spots—avoid major cities and military targets. The logic is brutal but clear: first hit the military, then the economy, and finally, the crowded population centres. Survival tip: don’t be where the fireworks start.

War is the fastest way to bankrupt an empire, and France’s history is a textbook example. Donald Copperfield seems poised to repeat this cycle. Starting in 1558, Henry II drained fortunes fighting the Habsburg-Valois Wars before defaulting. Then in 1648, the young Louis XIV juggled debt amid the Thirty Years’ and Franco-Spanish Wars, eventually suspending payments and manipulating currency. By 1661, scandal erupted as Finance Minister Fouquet was arrested for embezzlement while the debt continued to spiral. Finally, after the War of Spanish Succession in 1715, France went bust again, conveniently pretending some debts never existed. History shows that war and debt are inseparable, and empires inevitably pay the price.

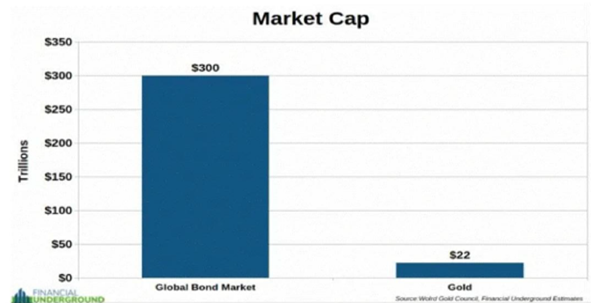

As the world marches toward WW3, history delivers a clear warning: war triggers stagflation, inflationary busts, and government power grabs edging nations toward default—a battle already raging this decade as bondholders bleed value. Decades of reckless spending and monetary distortion have pushed the western world to the brink. The “Big Beautiful Bill” is just another salvo in endless debt and denial. Bond markets—not stocks—are sounding the alarm: soaring yields, synchronized selloffs, and shadow buyers expose a system losing trust. Behind the scenes, the U.S. has already defaulted silently through inflation. Yet many still worship U.S. Treasuries as “risk-free,” ignoring that since 1971, bonds have fuelled a $300 trillion debt beast while all the world’s gold is worth just $22 trillion. The real question: trust politicians’ paper promises or centuries of real value?

At the end of the day, empires tend to commit suicide in three acts: (1) reckless fiscal mismanagement fuels inflation to paper over debt; (2) when borrowing runs dry, they unleash tyranny at home and start blaming an external bogeyman—this time, Putin; and (3) door number three swings open—default, government collapse, and a fresh regime promptly disowning the old debts. Classic tragedy, same script, different cast and we just entered stage 2.

In this context, the path to real prosperity remains paved with tangible assets, not fragile IOUs not genius digital tokens, Physical gold and silver—free from counterparties, free from surveillance—stand as the ultimate antifragile shields. Beyond precious metals, broader commodities guard against a fracturing global supply chain.

Cash must be wielded with precision: favor short-dated USD investment-grade bonds and T-bills to maintain income and swift agility.

In equities, hunt for lean, low-debt, high-cash-flow champions—businesses ready to thrive amid reshoring, trade wars, and surging defense budgets. Because the real enemy isn’t next door; it’s the warmongers pulling the strings.

The Goldilocks era is dead. The age of Gold In Lots—is the new survival playbook.

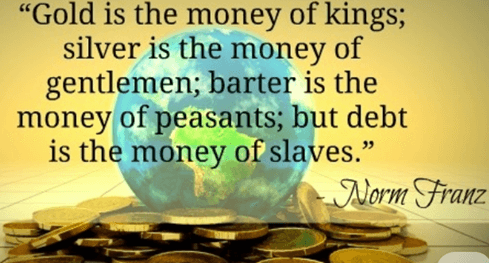

Never forget that Gold is the currency of Kings, Silver the money of Gentlemen; Barter is the money of Peasants, but Debt is the money of Slaves.

KEY TAKEWAYS.

As the golden mercantilist BRICS future unfolds, the key takeaways are:

- BRICS has evolved from a market label into a powerful coalition of resource-rich, populous nations reshaping global trade and finance, overtaking the fading Western empires to command nearly half the world’s economic output and population.

- History taught us that global power is a never-ending game of musical chairs—and while the West clings to fading glory, BRICS is gearing up to claim the next throne, with China riding innovation as an elevator up while America watches progress like paint drying.

- The 2025 tariff blitz turned economic tools into blunt geopolitical weapons, pushing BRICS and the Global South to unite against U.S. financial domination—and proving you can’t bankrupt them without backfiring spectacularly.

- BRICS didn’t wait for the tariff tantrums to ditch U.S. Treasuries—they ghosted Uncle Sam back in 2018, as Russia’s resources, China’s factories, and India’s booming market teamed up to throw the Global South’s hottest trade party, leaving the West out in the cold.

- BRICS+ are playing economics 101 by trading smart, hoarding over 20% of the world’s gold, ditching the dollar, and leveraging their massive gold reserves to fuel a new multipolar financial showdown.

- BRICS won’t rush a unified currency, but China’s quietly building a gold-backed, yuan-fuelled financial system that rewrites the global playbook—think Bretton Woods 3.0 with a smarter twist, where nations choose growth or dependence, and gold holds the keys to a new world order.

- As the US economy shifts into an inflationary bust, investors will once again need to focus on the Return OF Capital rather than the Return ON Capital, as stagflation spreads.

- Physical gold and silver remain THE ONLY reliable hedges against reckless and untrustworthy governments and bankers.

- Gold and silver are eternal hedge against “collective stupidity” and government hegemony, both of which are abundant worldwide.

- With continued decline in trust in public institutions, particularly in the Western world, investors are expected to move even more into assets with no counterparty risk which are non-confiscable, like physical Gold and Silver.

- Long dated US Treasuries and Bonds are an ‘un-investable return-less’ asset class which have also lost their rationale for being part of a diversified portfolio.

- Unequivocally, the risky part of the portfolio has moved to fixed income and therefore rather than chasing long-dated government bonds, fixed income investors should focus on USD investment-grade US corporate bonds with a duration not longer than 12 months to manage their cash.

- In this context, investors should also be prepared for much higher volatility as well as dull inflation-adjusted returns in the foreseeable future.

HOW TO TRADE IT?

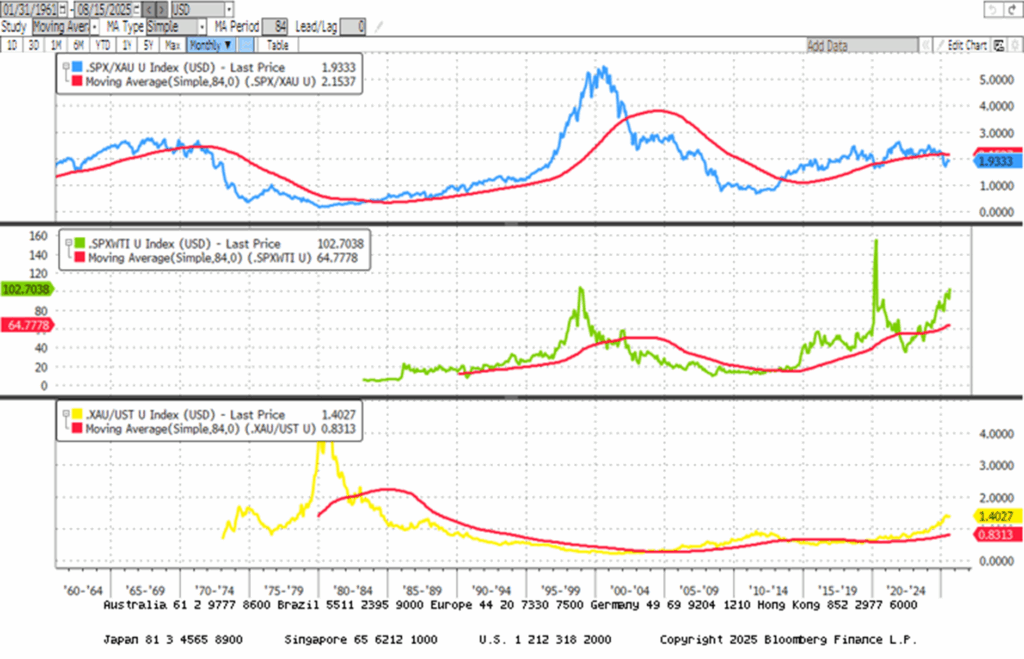

As of August 15th , 2025, the US remains in an inflationary boom, but with the S&P 500 to Gold ratio now below its year below its 7-year moving average for almost 7 months, an inflationary bust will materialize much sooner than Wall Street pundits and their parrots are eager to tell their clients. In this context, investors should stay calm, disciplined, and use market data tools to anticipate changes in the business cycle, rather than fall into the forward confusion and illusion spread by Wall Street.

Savvy investors worldwide—those not still shackled by the Western propaganda machine and its Keynesian fairy tales—have already grasped the brutal truth: the harder the West pushes its Malthusian depopulation agenda through endless wars against BRICS, the stronger the unbreakable bond between Russia, China, and India becomes. From the next decade onward, this Triumvirate will forge the new economic heart of the planet, reshaping the world order in their unstoppable rise.

As the Romans used to say, ‘verba volant, scripta manent’—spoken words fly away, written words remain, a reason why people must write to be read and heard.

More than half of the world’s population resides within a relatively compact geographic zone encompassing China, India, Southeast Asia, and parts of Central Asia. At its center, Hong Kong—historically a Chinese city under English law—occupies a strategic position as a financial, commercial, maritime, and logistical hub. Surrounding it are the industrial powerhouse of China, the labor-rich economies of Southeast Asia, the resource-abundant regions of Russia and the Central Asian republics and the consumer rich India. The disruption of traditional westward trade routes following the Ukraine conflict has redirected Central Asian raw materials southward, facilitating intra-regional commerce. With the ability to transact in local currencies rather than dollars, these economies face fewer external trade constraints, setting the stage for intensified regional integration and potentially one of the most significant Ricardian growth booms in modern history.

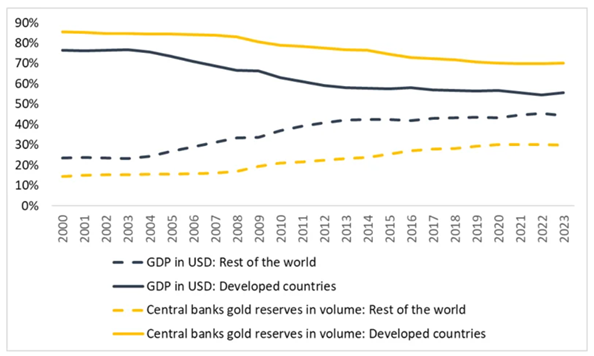

The BRICS+ bloc is leveraging demographic scale, industrial capacity, and commodity security to advance a multipolar economic order independent of Western financial dominance. Intra-regional trade, infrastructure investment, and settlement in local currencies are reducing reliance on the U.S. dollar, eroding the leverage of transatlantic institutions. This shift parallels a broader global realignment: developed economies’ share of world GDP has fallen from 80% to near 50% since 2000, while emerging markets have risen from 20% to the same level.

Similarly, gold reserves are shifting: the share held by developed-world central banks is declining, while emerging-market central banks now hold a rapidly growing portion—mirroring the historic transfers of gold from Europe to the U.S. between 1900 and 1945. This shift signals a loss of competitiveness, as capital and gold flow to regions where entrepreneurs are better treated and debt sustainability is stronger. Just as it was foolish to hold European bonds during the First World War when gold was moving to America, it is now risky to hold Western sovereign debt while gold migrates toward Asia. These flows, already well underway, are irreversible and historically precede currency revaluations—meaning Western currencies are likely to weaken as emerging-market currencies strengthen.

In the age of permanent crisis—where markets convulse, debts swell, and trust in authority rots—stability is a relic. Power lurches from emergency to emergency, each one eroding what little autonomy remains. In such a world, salvation will not come from the glitter of digital illusions or the empty script of policy speeches. It will come from the cold, immutable weight of gold.

The new order demands compliance, surveillance, and central control; fiat currencies march in lockstep toward their own erasure. Bitcoin, stablecoins, and the rest of the digital menagerie will be absorbed or broken. Antifragile and Non-Confiscable Gold alone resists absorption—beyond counterparty reach, beyond algorithmic control, beyond confiscation by bureaucratic decree.

As the American empire stumbles through its boom-bust death cycle, investors have to follow the gold as history’s verdict is unchanged: tangible assets endure while paper promises burn. The future will not be won by those who innovate fastest, but by those who hold what cannot be printed, censored, or erased. Gold has outlasted empires; it will outlast this one.

In a nutshell, the playbook is simple: don’t get confiscated, don’t get frozen, and don’t get poor trying to get rich. In times like these, liberty and liquidity live in personal vaults—not in banks. And always remember: In Gold We Trust—Because Gold Is For War.

At the end of the day, ‘The Desire for Gold is not for gold. It is for the means of freedom and benefits’ .

Want the full deep dive? You can read The MacroButler’s original article on his Substack

https://themacrobutler.substack.com/p/brics-gold-glory-the-dawn-of-a-new