Published: 07-16-2026, 11:07 am

Key Takeaways

- Purchasing power measures how much real goods and services a unit of money can buy. When the money supply expands faster than the economy, purchasing power falls — even if your bank balance stays the same.

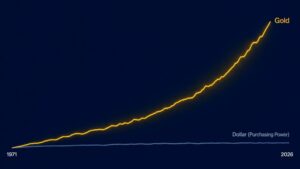

- Since August 15, 1971, the U.S. dollar has lost approximately 87% of its purchasing power, according to Bureau of Labor Statistics CPI-U data. What cost $1 in 1971 now costs roughly $8.

- Gold’s supply grows at less than 1% per year on average over the past decade through mining — no faster. That physical scarcity is why one ounce of gold has bought a comparable basket of goods across radically different eras of monetary history.

- The Cantillon Effect means inflation is not experienced equally. Those closest to the source of new money — banks, financial institutions, large asset holders — deploy it before prices adjust. Ordinary savers receive it last, after purchasing power has already been redistributed.

- Gold sits outside the fiat system. Governments cannot create it, central banks cannot expand its supply by policy decree, and no printing press can dilute it. That is its structural advantage over every currency that has ever existed.

Purchasing power is the quantity of real goods and services a unit of currency can actually buy at any given moment — and it is the single most important number your bank statement will never show you.

When more money chases the same supply of goods, each dollar buys less. The U.S. Bureau of Labor Statistics tracks this through the Consumer Price Index. Since 1971, the dollar has lost approximately 87% of its purchasing power [Bureau of Labor Statistics CPI-U data]. Gold, by contrast, has preserved it across centuries — because its supply grows at less than 1% per year on average, and no government can decree otherwise.

In June 2026, U.S. headline CPI ran at 3.5% year-over-year [Bureau of Labor Statistics, released July 14, 2026]. That number sounds manageable. However, at the Fed’s own stated target of 2% annually, a fixed dollar amount loses roughly 18% of its purchasing power over a single decade [Federal Reserve]. Across a 30-year retirement horizon, the math is severe: a 2% annual erosion compresses purchasing power by nearly half. The investor who understands this mechanism does not panic — they plan around it.

For most of human history, money and purchasing power were inseparable. A gold coin carried a fixed quantity of metal — the government could not print another one. As a result, prices measured in gold tended to stay stable across generations. That relationship changed decisively on August 15, 1971, when President Nixon ended the U.S. dollar’s last formal link to gold. In the five decades since, purchasing power has become a moving target — one that moves relentlessly in the wrong direction for savers holding cash.

What Does Purchasing Power Actually Measure?

Purchasing power measures the real-world command a unit of money has over goods and services. Specifically, it answers the question: how much can this dollar actually buy today, compared to what it could buy yesterday, last year, or a generation ago?

The U.S. Bureau of Labor Statistics (BLS) quantifies this through the Consumer Price Index, or CPI. The CPI tracks the price of a standardized basket of goods and services — food, housing, transportation, medical care, education, and others — across time. When the index rises, each dollar buys a smaller fraction of that basket. That reduction is the loss of purchasing power.

Furthermore, the Federal Reserve tracks a separate measure: the Personal Consumption Expenditures Price Index (PCE). It typically runs about 0.4 percentage points lower than CPI [Cleveland Fed / Bureau of Labor Statistics]. The Fed uses PCE as its preferred inflation gauge and targets a 2% annual rate. In practice, however, the cumulative erosion matters more than any single year’s reading. Over decades, small annual losses compound into substantial destruction of real wealth.

The Knowledge That Changes Everything

Two essential guides — yours free. Understand why gold matters and why fiat currencies always fail.

What Has Happened to the Dollar’s Purchasing Power Since 1971?

The modern story of purchasing power erosion starts with a specific date: August 15, 1971. That evening, President Nixon announced the end of the dollar’s convertibility into gold at $35 per ounce. The decision terminated the Bretton Woods monetary system. Before that moment, foreign governments and central banks could exchange dollars for gold. That arrangement placed a hard external constraint on how aggressively the United States could expand its money supply. After that moment, no such constraint existed.

The consequences accumulated over decades. According to Bureau of Labor Statistics CPI-U data, the dollar has now lost approximately 87% of its purchasing power since 1971 [BLS CPI-U]. In practical terms, a dollar in 1971 bought what costs roughly $8 today. That is not a dramatic collapse — no single year produced catastrophic losses. Instead, it was a slow, methodical erosion driven by repeated rounds of money supply expansion.

The most acute recent episode ran from February 2020 to April 2022. In those 26 months, M2 expanded from $15.4 trillion to $21.8 trillion — a 41% increase and the largest monetary expansion in the modern data series [Federal Reserve FRED, M2SL]. The lagged effect on consumer prices peaked at 9.1% annual CPI inflation in June 2022. As of July 2026, headline CPI sits at 3.5% annually — down from its recent peak, but still meaningfully above the Fed’s stated 2% target [BLS, July 14, 2026].

Why Does Fiat Currency Lose Purchasing Power Over Time?

Fiat currencies lose purchasing power because their supply is not physically constrained. A government that needs to fund spending can direct its central bank to create new money — through bond purchases, direct lending programs, or reserve expansion. That new money enters the economy, bids up prices, and reduces the real value of every dollar already in existence.

The mechanism is straightforward. If money in circulation doubles while goods stay roughly constant, each unit of money is worth approximately half as much in real terms. Prices adjust upward to reflect the larger supply of money. Savers holding the old money find themselves holding something less valuable than what they started with.

Notably, this dynamic is not unique to the United States. Every fiat currency in history has eventually lost a significant portion of its purchasing power. Every government that has operated a fiat system has eventually yielded to the incentive to expand the money supply. The Roman Empire debased its silver denarius over centuries. Its silver content fell from roughly 95% under Augustus to less than 5% by the mid-third century AD — under Emperor Gallienus around 260 AD. The result was ruinous inflation that contributed to the empire’s economic decline [Roman monetary historians]. The mechanism has not changed. Only the technology of money creation has modernized.

Who Bears the Cost When Purchasing Power Falls?

This is where the story gets specific — and where most economic textbooks stop short. Inflation is commonly described as a general rise in prices that affects everyone proportionally. In reality, it does not work that way.

The 18th-century economist Richard Cantillon described this precisely. When new money enters an economy, it does not arrive simultaneously in every bank account. Instead, it flows first to those closest to the source — typically banks, financial institutions, government contractors, and large asset holders. These recipients spend and invest the new money before prices have adjusted upward to reflect the increased supply. They get to buy assets and goods at yesterday’s prices with tomorrow’s money. By the time that same money trickles through to ordinary wage earners and savers, prices have already risen. The purchasing power has already been redistributed.

Consequently, understanding purchasing power erosion is not merely an academic exercise. It is the foundational question of personal financial security. How does a saver protect the real value of what they have worked to accumulate, when the very unit they saved in is designed to lose value over time?

How Does Gold Preserve Purchasing Power?

Gold preserves purchasing power because of a structural property no fiat currency can replicate. Its supply grows at a rate no government, central bank, or policy decision can significantly accelerate. Global gold mine production has grown at less than 1% per year on average over the past decade [World Gold Council]. No printing press, no quantitative easing program, and no executive order can change that. Gold’s purchasing power rests on something no government can replicate — the physical limits of extraction from the earth’s crust.

The historical evidence for this is compelling. Research by economists Claude B. Erb and Campbell R. Harvey examined what a Roman legionary soldier earned in the era of Emperor Augustus — approximately 2.31 ounces of gold per year. A modern U.S. Army E-1 Private earns a base pay of approximately $28,886 annually as of 2026 [DFAS 2026 military pay tables]. At current gold prices near $4,100 per ounce, 2.31 ounces is worth approximately $9,500 today — roughly one-third of a modern private’s annual base pay. The Roman soldier earned substantially less in gold terms than his modern counterpart. Even so, the gap spans just three orders of magnitude across 2,000 years of monetary history. Across that same period, every fiat currency that competed with gold has effectively ceased to exist. Gold-denominated wages have remained in a recognizable range; the currencies used to pay them have not [Erb and Harvey, “The Golden Dilemma,” Financial Analysts Journal, 2013].

Does Gold Hold Its Value Against Commodities Too?

Moreover, the gold-to-oil ratio illustrates the same principle across a completely different commodity. From 1970 through the modern era, one ounce of gold has consistently purchased roughly 15 to 20 barrels of crude oil on average [Federal Reserve Bank of St. Louis / U.S. Energy Information Administration]. That long-run stability held through two major OPEC oil shocks, the Volcker recession, the dot-com boom, and the 2008 financial crisis. When gold and oil are priced against each other — rather than against fiat dollars — the ratio is remarkably durable.

What Most Investors Miss About Purchasing Power and Gold

The conventional framing of gold is that it “hedges inflation.” That means it rises when CPI runs hot and falls when CPI cools. That framing is partially correct but structurally incomplete, and misunderstanding it leads investors to incorrect conclusions.

In reality, gold does not primarily track reported CPI. It tracks the real cost of holding money — specifically, what economists call the real interest rate. When nominal interest rates are low relative to inflation, the opportunity cost of holding gold (which pays no yield) shrinks toward zero. When real rates turn meaningfully negative, cash in a savings account is earning less than the rate at which it loses purchasing power. In that environment, gold becomes one of the only instruments that preserves real value without counterparty risk.

Furthermore, gold’s most important purchasing power function operates over decades — not months. The investor tracking gold’s week-to-week price in dollar terms is watching the measuring stick wiggle. The investor holding gold for the structural reason is asking a different question. What will this ounce buy in ten years, when governments have issued more debt, central banks have expanded their balance sheets further, and the Cantillon redistribution has continued?

Why Gold’s Rise Since 1971 Is Not What Most People Think

The 87% purchasing power loss since 1971 is not primarily a story about inflation. It is a story about what happens when the constraint on money creation is removed. Gold’s rise from $35 per ounce in 1971 to above $4,000 today is not magic, and it is not speculative excess. It is the dollar’s true inflation record, expressed in ounces rather than CPI index points. When the measuring stick expands, the thing being measured appears to grow — but the gold has not fundamentally changed. The dollar has.

What Does Purchasing Power Erosion Mean for Long-Term Savers?

For a long-term saver, purchasing power erosion is not a theoretical risk. It is a guaranteed outcome for anyone holding a meaningful portion of wealth in cash or fixed-income instruments over a multi-decade horizon. At 3% annual inflation — roughly the 50-year average since Nixon’s decision — the real value of a fixed dollar amount halves in approximately 24 years. For someone saving for retirement at 45 and expecting to draw on those savings at 70, the mathematics are consequential.

Why the Official Inflation Number Understates the Problem

Additionally, the Cantillon Effect adds a second layer to this problem. The official inflation figures represent an average across the full basket of goods. In practice, housing, healthcare, and education — the goods that matter most for household financial security — have historically inflated faster than the headline CPI number. Meanwhile, financial securities, real estate, and physical gold are precisely the assets whose prices rise first when new money enters the system. Ordinary wage earners see the benefit last. The saver who holds only cash and bonds while these assets appreciate is experiencing purchasing power erosion on both sides simultaneously.

Physical gold addresses this problem directly. It sits outside the fiat monetary system. No government policy can expand its supply. No central bank decree can dilute its purchasing power. It carries no counterparty risk — no institution’s solvency determines its value. Central banks understand fiat currency mechanics better than anyone. They have been net buyers of gold for 16 consecutive years through 2025 [World Gold Council], and are not buying gold because they expect an imminent crisis. They are buying it because they understand what purchasing power erosion looks like across decades — and they are positioning accordingly.

Stay On Top of Gold & Silver Prices

Get important market alerts sent straight to your inbox.

People Also Ask

What is purchasing power in simple terms?

Purchasing power is how much real stuff a dollar can buy at a given moment. When prices rise faster than income, purchasing power falls — meaning money buys less even though the number on the bill stays the same. The U.S. Bureau of Labor Statistics measures this through the Consumer Price Index, which tracks what a standardized basket of goods costs over time. When the index rises, each dollar’s purchasing power has fallen by the corresponding percentage.

Why does fiat currency lose purchasing power over time?

Fiat currencies lose purchasing power because their supply is not physically constrained. Governments and central banks can expand the money supply through bond purchases, direct lending programs, and reserve expansion. When more money chases the same supply of goods, prices rise and each existing unit of currency buys proportionally less. Since 1971, when the U.S. dollar’s last link to gold was severed, the dollar has lost approximately 87% of its purchasing power according to Bureau of Labor Statistics CPI-U data.

How does gold preserve purchasing power?

Gold preserves purchasing power because its supply grows at less than 1% per year on average through mining — and no government policy can significantly accelerate that rate [World Gold Council]. This scarcity means the quantity of goods one ounce of gold can buy has remained remarkably consistent across radically different eras of monetary history. Research on Roman-era wages shows a recognizable relationship between ancient and modern military pay when expressed in ounces of gold. A Roman legionary earned approximately 2.31 ounces per year under Emperor Augustus. Despite 2,000 years of intervening monetary history, that gold-denominated figure remains in a comparable range to modern base pay [Erb and Harvey].

How much purchasing power has the dollar lost since 1971?

According to Bureau of Labor Statistics Consumer Price Index data, the U.S. dollar has lost approximately 87% of its purchasing power since August 15, 1971, when President Nixon ended the dollar’s convertibility into gold. In practical terms, what cost $1.00 in 1971 now costs roughly $8 today. This erosion did not happen in a straight line. It accelerated during the 1970s oil shocks, the post-2008 quantitative easing programs, and the 2020–2022 pandemic expansion that increased M2 by 41% in 26 months [Federal Reserve FRED, M2SL].

What is the Cantillon Effect and how does it affect savers?

The Cantillon Effect describes how newly created money enters the economy unevenly. Banks, financial institutions, and large asset holders receive the new money first. Prices have not yet adjusted upward, so they can buy assets and goods at pre-inflation prices. By the time the new money reaches ordinary savers and wage earners, prices have already risen. The net result is a quiet, non-legislative wealth transfer from savers and fixed-income holders toward those with early access to newly created money. Richard Cantillon first described this mechanism in his 1755 work Essay on the Nature of Trade in General.

SOURCES

1. Bureau of Labor Statistics — Consumer Price Index Summary, June 2026; Federal Reserve Bank of St. Louis — CPI-U Purchasing Power of the Consumer Dollar, FRED series CUUR0000SA0R

2. Federal Reserve Bank of St. Louis — M2 Money Supply (M2SL), FRED; Cleveland Fed — PCE vs. CPI Differential Analysis

3. World Gold Council — Central Bank Gold Reserves, Net Purchases Data 2025; Gold Demand Trends Full Year 2025, Mine Supply Data

4. Erb, Claude B. and Harvey, Campbell R. — The Golden Dilemma, Financial Analysts Journal, 2013

5. U.S. Energy Information Administration / Federal Reserve Bank of St. Louis — Gold-to-Oil Ratio Historical Data

6. Cantillon, Richard — Essay on the Nature of Trade in General, 1755

7. Defense Finance and Accounting Service — 2026 Military Pay Tables, effective January 1, 2026

8. GoldSilver — 87% Dollar Devaluation Since 1971: Why Central Banks Keep Buying Gold; Gold vs. Inflation: What 100 Years of Data Shows

Disclaimer: This article is for informational purposes only and does not constitute financial or investment advice. Always consult a qualified financial adviser before making investment decisions.

You May Also Like:

- Why Hong Kong? Inside GoldSilver’s Offshore Gold Storage Network

- Silver Price Outlook July 2026: Two Catalysts, One Setup

- Why the 10-5-3 Rule Fails Gold and Silver Investors

- Why Is Silver So Hard to Mine? The Primary Supply Problem Explained

- Gold Price Outlook July 2026: The Price Fell. Case Intact.

- Buying the Top: A Survival Guide for Gold and Silver Investors

- How Do Gold Price Cycles Work? A Framework Across Four Time Horizons