Published: 07-14-2026, 04:58 pm

The chair of the Federal Reserve testified before Congress today and said something that every individual saver should hear. Fed rate policy — the tool that was supposed to serve everyone equally — created a generation of homeowners and, behind them, a generation locked out. Chairman Kevin Warsh put it plainly to the House Financial Services Committee: he wants monetary policies that are “not boom-and-bust, that don’t just make one generation more fortunate about being able to afford their first home than the next.”

That is not an abstract concern. It is an official admission — from the institution that sets the price of money — that the financial system it manages punishes individuals based on timing rather than discipline.

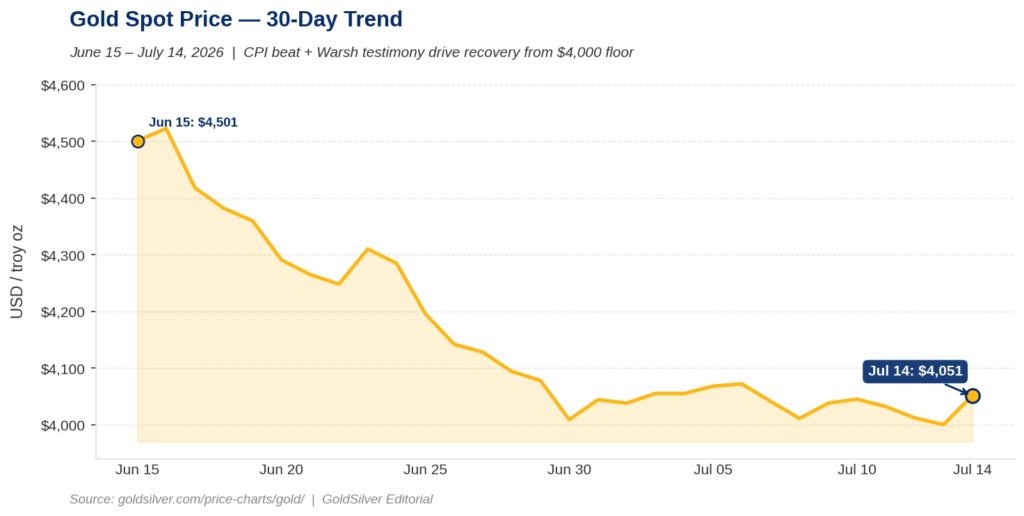

Gold rose to $4,054.67 on Tuesday — up $53.76, or 1.32%, on the session — after June CPI printed a steeper-than-expected decline. Silver advanced to $58.77, up 1.96%. Both metals recovered sharply from Monday’s two-week lows.

Why Did the Fed Chair Raise Housing Policy in a Monetary Testimony?

Warsh’s housing remarks were not a prepared talking point. They came in response to direct questions about the consequences of the Federal Reserve’s post-pandemic rate cycle. He described the mechanism with unusual candor. When the Fed cut rates to near zero in 2020 and 2021, millions of buyers locked in 30-year mortgages between 2.65% and 3.5% — a range that touched an all-time record low in January 2021, according to Freddie Mac. Warsh called that window “a once-in-a-lifetime opportunity to get the first house.”

Those buyers built equity as home prices rose. In contrast, today’s first-time buyers face a 30-year fixed rate averaging 6.49% — per Freddie Mac’s survey for the week of July 9, 2026 — on homes that cost substantially more than they did four years ago. The monthly payment on a median-priced home now consumes approximately 32% of median household income — above the 28–30% threshold that conventional lenders consider sustainable, according to the NAHB/Wells Fargo Housing Opportunity Index for Q1 2026.

The result is a housing market divided not by income or effort but by the year of your mortgage application. Around 80% of outstanding US mortgages carry a rate at or below 6%, according to NAHB. Those holders are rational not to sell. Meanwhile, roughly 62% of Americans say buying a home in 2026 is simply unrealistic, up from 49% just one year ago, according to IPX1031’s 2026 homeownership survey. Two people. Same discipline. Entirely different financial outcomes — because of when the Fed moved.

The Edge Every Investor Needs Smarter precious metals investing starts here. The Nuggets Newsletter brings you essential market insights, Fed updates, global trends, educational videos, and much more.

Why Does Fed Monetary Policy Create Winners and Losers?

This is the mechanism that most financial coverage misses. Fiat currency systems give a single institution — the Federal Reserve — the authority to set the price of money for an entire economy. When the Fed sets that price too low, as it did from 2020 to 2022, asset prices inflate. Housing prices surged. Stock indices hit records. Those who already owned assets saw their balance sheets expand. Savers who held cash watched their purchasing power erode. When the Fed subsequently raised rates to fight the inflation it helped create, it froze the market it had overheated. Consequently, a first-time buyer in 2026 faces both elevated asset prices and elevated borrowing costs — a combination that no individual decision could have avoided. The system produced that outcome, not their choices.

Warsh called this a mistake. He explicitly criticized the Fed’s 2020 flexible average inflation targeting framework as an institution that “asked for a little more inflation and ended up with a lot more.” He said he wants “regime change.” Yet even the most sincere regime change cannot undo five years of compounding distortion. The purchasing power damage is already in the system. The housing market asymmetry is already structural.

What Does This Mean for Gold Holders?

Gold does not have a mortgage rate. It does not have a Fed policy cycle. It does not create winners and losers based on the calendar year you decided to save. An ounce held in 2020 is the same ounce held today, and its purchasing power has moved in the opposite direction of the dollar that priced it. Furthermore, gold sits entirely outside the financial system that Warsh described — the one that transferred wealth from savers-who-waited to asset-holders-who-timed-it. That system cannot reach a physical ounce. It cannot dilute it, refinance it, or lock it out of the housing market.

Goldman Sachs maintains a year-end 2026 gold target of $4,900. JPMorgan’s Q4 target sits at $4,500. Both projections rest on the same structural foundation: a Federal Reserve that is navigating between elevated inflation and unaffordable tightening, and a dollar that bears the full cost of that navigation. Warsh’s admission today does not change the near-term price picture. However, it does something more important — it confirms, from the podium of the institution itself, the structural argument for holding sound money outside the system. Our July 2026 gold price outlook laid out exactly this structural case before today’s testimony landed.

What Should Investors Watch Next?

Warsh testifies before the Senate Banking Committee on Wednesday, July 15. Markets will parse his language for any softening on the rate outlook now that June CPI has come in cooler than expected. The next decisive policy moment is the FOMC meeting on July 28–29. If September rate-hike odds continue to compress — they were near 76% before today’s CPI print — gold’s path back toward $4,200 opens. If Warsh’s hawkish framing holds the September odds firm, watch the $4,000 level as structural support. Either way, today’s admission stands on the record. The institution that manages the dollar has acknowledged, under oath, that its own tools produce outcomes that are neither neutral nor fair to the individual saver.

Stay On Top of Gold & Silver Prices

Get important market alerts sent straight to your inbox.

SOURCES

1. Federal Reserve — Testimony of Chairman Kevin Warsh, Semiannual Monetary Policy Report to Congress, July 14, 2026

2. Bureau of Labor Statistics — Consumer Price Index Summary, June 2026 (July 14, 2026)

3. National Association of Home Builders — NAHB/Wells Fargo Housing Opportunity Index, Q1 2026 (May 21, 2026)

4. Freddie Mac — Primary Mortgage Market Survey, Week of July 9, 2026

5. GoldSilver — Live Gold Spot Price, July 14, 2026

Disclaimer: This article is for informational purposes only and does not constitute financial or investment advice. Always consult a qualified financial adviser before making investment decisions.

You May Also Like:

- Warsh Testified. Gold Jumped $90. The Signal Everybody Missed Was in His Report.

- Gold Jumped $90 This Morning. June CPI Just Explained Why.

- Silver Fell 3.8% Today. Gold Fell 2.9%. The Gap Has a Name.

- Trump’s Hormuz Toll Is an Inflation Tax. Here’s Why Gold Fell.

- Gold Fell 1.4% on an Iran Strike. One Number Tomorrow Morning Could Change Everything.

- Trump Declared the Ceasefire Over. Gold Barely Moved.