Updated June 2026 · GoldSilver Editorial Team

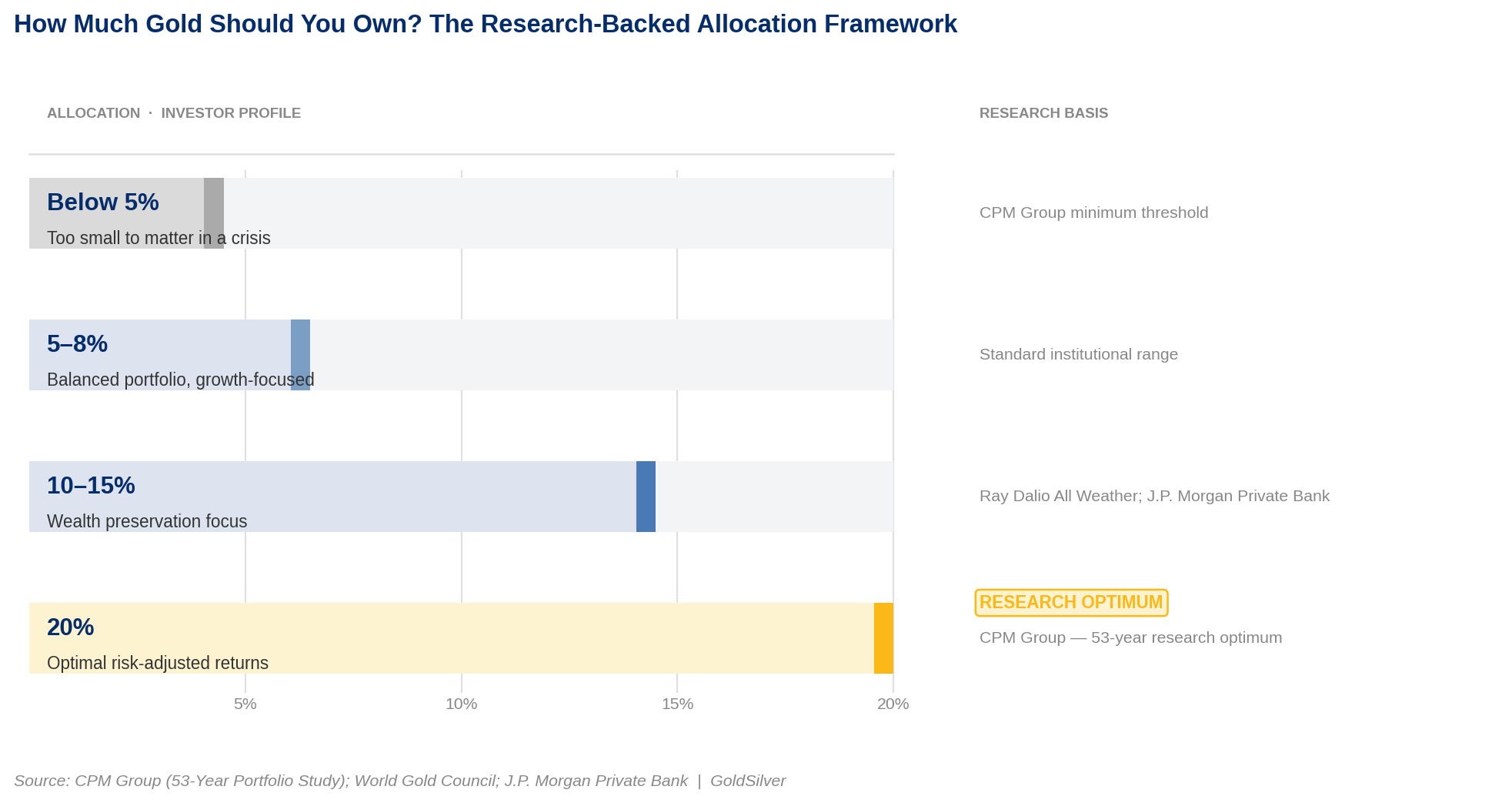

The Short Answer: Most financial strategists recommend holding 5–15% of your investable assets in physical gold, depending on your risk tolerance and time horizon. CPM Group's research across 53 years of market data identifies 20% as the optimal allocation for risk-adjusted returns (CPM Group, 53-Year Portfolio Study). Anything below 5% is unlikely to move the needle when it matters most.

How much gold should you own? Not enough to say you own some. Enough that if inflation ran hot for five years, or the stock market dropped 40%, or the dollar lost another decade of purchasing power — you'd feel it in a good way. The answer has a floor. CPM Group's analysis of 53 years of market data puts that floor at 5%, with 20% as the research optimum for risk-adjusted returns (CPM Group, 53-Year Portfolio Study). Most financial advisors recommend 5–15%. The evidence suggests you should be toward the higher end of that range right now.

5% is the minimum. 20% is the research optimum. Your number lives somewhere between — and three questions will help you find it.

What "Enough Gold" Actually Means: Three Portfolio Roles

Gold serves three distinct functions in a portfolio. The right allocation depends on which role — or combination — you are asking it to fill.

Role 1 — Portfolio Insurance

Gold's job as portfolio insurance is to limit drawdown during equity bear markets. According to J.P. Morgan Private Bank, across the last five instances where the S&P 500 fell 20% or more, gold averaged a 6% return (J.P. Morgan Private Bank, "Is It a Golden Era for Gold?", 2026). In 2008, for example, the S&P 500 fell 37% on the year and over 50% peak to trough. Gold, however, gained approximately 5.5% that calendar year. It then climbed roughly 163% from its late-2008 trough to its September 2011 peak (World Gold Council). The goal isn't to profit from a crash. It's to give the rest of your portfolio time to recover.

Role 2 — Purchasing Power Protection

Gold's second function is protecting the long-run value of your savings. Dollar erosion doesn't arrive as a single crash — it accumulates quietly through deficit spending, money creation, and the compounding effect of a government carrying too much debt. This isn't a hedge against a market event. It's a hedge against the slow devaluation that shows up as things costing more every year.

Role 3 — Financial Sovereignty

Physical gold held outside the banking system carries no counterparty risk. No government can inflate it away, no institution can rehypothecate it, and no counterparty can default on it. It moves independently of your stock portfolio and owes nothing to any financial intermediary's solvency. That independence is a structural property of the metal itself — no ETF or financial instrument replicates it.

Most long-term holders are holding for all three reasons simultaneously. The allocation math reflects that.

The Research-Backed Framework: Why the Gold Allocation Range Is 5–20%

The optimal gold allocation, based on 53 years of market data, is 20% of a balanced portfolio (CPM Group, 53-Year Portfolio Study). That's where gold adds the greatest risk-adjusted return without dragging on performance in sustained equity bull markets.

Most advisors, however, cite a lower figure: 5–15%. That range reflects gold's 20-year correlation with equities of approximately 0.14 — effectively zero (World Gold Council, "Relevance of Gold as a Strategic Asset"). Because gold and stocks move largely independently, even a small position provides real diversification. A 5% gold allocation reduces overall portfolio risk by nearly 5%, while contributing just 1.9% to total portfolio volatility (World Gold Council, Gold Focus, December 2025).

The CPM Group's 20% figure comes from studying portfolios through multiple recessions, two major equity bear markets, and sustained inflationary periods. In those environments — not stable ones — higher gold allocations came out ahead. As of mid-2026, the current macro environment fits that second description, not the first.

The Minimum Gold Allocation That Actually Works

The minimum allocation that can materially protect a portfolio is 5% of investable assets (CPM Group). Below that threshold, even a strong gold performance cannot meaningfully offset losses elsewhere.

Here's the arithmetic. If you hold 5% in gold and your equities fall 50%, gold would need to rise 400% to get your total portfolio back to breakeven. That's not realistic in a single bear market. At 10%, the required offset drops to 200%. At 20%, gold needs to rise 100% — which is closer to what it has historically delivered in major downturns. It rose approximately 163% from its late-2008 trough to its September 2011 peak (World Gold Council).

Consider current prices near $4,500 per ounce. At that level, one ounce is a rounding error in a $200,000 portfolio. A position too small to matter fails its purpose — regardless of how well gold performs. Most investors who take portfolio protection seriously end up somewhere between 10% and 20%, adjusted for the three personal factors below.

How to Size Your Personal Gold Allocation: Three Questions

Three questions determine where your number lands within the research range.

1. What Is Your Time Horizon?

Over the 20-year period ending 2025, gold delivered approximately 12% in average annual returns (J.P. Morgan Private Bank, 2026). However, that number comes with real volatility attached. Gold hit an all-time high near $5,595 in late January 2026, then pulled back sharply through spring before stabilizing. Short-term swings are simply part of the deal.

If your horizon is shorter than five years, keep the allocation smaller — you have less runway to absorb corrections. If you're holding for a decade or more, those corrections become buying opportunities rather than reasons to exit.

2. How Much Do You Trust the Dollar's Purchasing Power?

This is the single most important variable in the gold allocation decision.

The US fiscal deficit is projected at approximately $1.9 trillion for fiscal year 2026 (Congressional Budget Office, Budget and Economic Outlook 2026). Interest payments on the national debt have reached $1 trillion annually — a first in US history (Congressional Budget Office; Peter G. Peterson Foundation, 2026). Meanwhile, gold mine supply has been essentially flat for nearly a decade, growing at well under 1% per year and approaching a production plateau (World Gold Council, "Is Mined Gold Production Peaking?", January 2026). The dollar has no supply constraint. Gold does.

When the gap between money creation and value creation widens persistently, purchasing power erodes. Gold has historically filled that gap. Goldman Sachs calls this dynamic the "debasement trade" — structural buying by investors hedging long-term fiscal and monetary policy risk. Their year-end 2026 gold price target is $5,400 per ounce, reaffirmed in April even after gold's sharpest monthly decline since 2013 (Goldman Sachs, April 2026). J.P. Morgan Private Bank holds a 2026 price outlook of $6,000–$6,300 per ounce (J.P. Morgan Private Bank, February 2026). When two of Wall Street's most scrutinized research desks sit well above current prices, that alignment is data worth registering — though no price forecast should drive an allocation decision alone.

3. How Would You Actually Use Your Gold If You Needed It?

Physical gold has one constraint that paper assets don't: liquidity takes steps. Selling a stock takes seconds. Converting physical gold to cash takes a phone call, a shipping decision, and a day or two. That's fine if you're thinking in years. It matters if you might need the funds within days.

Work out the ounces needed to cover a specific income gap. Supplementing income by $1,000 per month for two years — $24,000 total — requires approximately 5–6 ounces at current prices near $4,500. That needs-based floor sits alongside the portfolio insurance math and gives your allocation a concrete lower bound.

Why the Current Macro Environment Favors a Higher Gold Allocation

The case for gold in 2026 is structurally stronger than it was in 2019. The long-term thesis hasn't changed. However, the conditions supporting the higher end of any allocation range have all shifted at once.

Central bank buying has structurally reset. Global central banks purchased 863 tonnes of gold in 2025 — the fourth-largest annual expansion on record and well above the pre-2022 average of 473 tonnes (World Gold Council, Gold Demand Trends Full Year 2025). The World Gold Council described 2025 demand as "surprisingly resilient" given how far prices had risen. Buying has continued at elevated levels into 2026.

Gold displaced US Treasuries as the world's largest reserve asset. In late 2025, global central bank gold holdings approached $4 trillion — edging past approximately $3.9 trillion in foreign Treasury holdings — for the first time since 1996 (World Gold Council, 2026). Central banks don't make momentum trades. They accumulate over decades. When institutions buy at record price levels while cutting Treasury exposure, the signal is structural, not tactical.

The traditional 60/40 portfolio no longer provides reliable downside protection. For decades, stocks and bonds moved inversely during market stress — a built-in hedge. However, when core inflation exceeds 2.5%, that negative correlation deteriorates. Both assets can fall together in the same inflationary shock (World Gold Council, "Gold's Optimal Portfolio Weight in a Higher Correlated Environment," May 2025). That's precisely the regime markets have been navigating since 2022.

Gold vs. Silver: How to Split the Precious Metals Allocation

Most long-term holders should weight 60–70% of their precious metals allocation toward gold and 30–40% toward silver. The two metals serve related but distinct purposes.

Gold is the more stable monetary metal. It is more universally recognized as a store of value and more predictable under financial stress. In a genuine systemic event — where counterparty risk on financial institutions becomes real — gold is the deeper anchor.

Silver, in contrast, is significantly more volatile. That volatility creates larger upside in a precious metals bull market, but also deeper drawdowns in bear periods. Silver also carries meaningful industrial demand that gold doesn't — solar panels, electronics, electric vehicles — generating price catalysts independent of the monetary story. Silver broke above $100 per ounce for the first time in history in January 2026, then reached an all-time high of $121.62 on January 29, before falling sharply in early February (World Gold Council, Q1 2026). Extraordinary upside followed by rapid reversal — that's silver's defining pattern.

The practical split is straightforward: weight your allocation toward gold for stability and purchasing power protection. Add silver in proportion to how much volatility you can hold without selling.

The Mistake Most Gold Investors Make: Skipping Annual Rebalancing

The single most common error in gold allocation is treating it as a set-and-forget position. It isn't.

Gold's correlation with equities is approximately 0.14 over the past 20 years — near zero (World Gold Council). That independence is precisely why gold works as a diversifier. However, it also means that during a sustained equity bull market, your gold weighting quietly drifts down as equities rise. A portfolio at 10% gold can find itself at 6–7% gold after a strong equity run — without you selling a single ounce. That drift leaves you under-allocated exactly when protection matters most: at the tail end of a bull market.

Annual rebalancing — restoring your target gold percentage once a year — maintains the insurance you built. It also enforces a discipline most investors find difficult: trimming equities when they've risen and buying gold at relative lows. Investors who held a 10% gold allocation and rebalanced annually over the past five years captured gold's structural move without predicting a single price point. Those who chased gold after its January 2026 all-time high paid a significant premium for the same protection.

Own enough to matter. Write the number down. Rebalance it once a year.

People Also Ask

Does Age or Retirement Timeline Change How Much Gold You Should Hold?

The conventional instinct — reduce risk as you age, shift from equities to bonds — doesn't map cleanly onto gold. A bond is income-generating and nominally principal-preserving. Gold is neither. Its job is to preserve purchasing power and perform when financial systems are under stress. That function doesn't diminish in retirement. A retiree drawing down a portfolio has less time to recover from a currency debasement event than someone still accumulating — making the purchasing power argument stronger in later years, not weaker.

What changes with age is not the allocation percentage but the form. A 35-year-old building a position over decades has full flexibility. A 65-year-old in drawdown wants some portion of their holding in a size and format that converts to cash quickly — standard 1-oz coins rather than larger bars for the liquidity tranche, and a custodied vault account for the bulk. The 5–20% range applies across age groups. What changes with retirement is how the position is structured and accessed, not how large it is.

What Are the Tax Implications of Owning Physical Gold?

The IRS classifies physical gold — bullion, coins, and bars — as a collectible. Long-term capital gains are therefore taxed at a maximum federal rate of 28%, compared to the 15–20% long-term rate that applies to most stocks and ETFs (IRS, Topic 409; IRS Publication 590-A). This 28% ceiling also applies to physically-backed gold ETFs — the IRS treats them identically to owning the metal directly. Short-term gains, from gold held less than one year, are taxed at ordinary income rates, which can be higher still.

The 28% rate is a ceiling, not a flat charge. Investors in lower tax brackets simply pay their marginal rate. Gold mining stocks are not classified as collectibles and are therefore taxed at the standard long-term capital gains rate of up to 20%.

Three practical takeaways: hold gold long-term, use tax-advantaged accounts where possible, and factor the 28% ceiling into your after-tax return projections.

Can I Hold Physical Gold Inside an IRA or 401(k)?

Yes — through a self-directed IRA, commonly called a Gold IRA. It follows the same contribution limits and tax rules as a standard IRA but allows physical precious metals as a qualifying investment. The 2026 IRA contribution limit is $7,500 per year ($8,600 for those 50 and older) (IRS, Publication 590-A; IRS Notice 2025-67). Gold must meet a minimum purity of 99.5% fineness, be purchased through an IRS-approved custodian, and be stored at an approved depository. Home storage disqualifies the account and constitutes a taxable distribution.

The tax advantage is meaningful. Gains inside a traditional Gold IRA are tax-deferred until withdrawal — the 28% collectibles rate doesn't apply while the metal sits in the account. Distributions are taxed as ordinary income. A Roth Gold IRA works differently: contributions are after-tax, but qualified withdrawals — including all appreciation — are tax-free. The trade-off is cost. Gold IRAs typically carry setup fees of $50–$150, annual custodian fees of $75–$300, and storage fees of roughly 0.5–1% of value annually. For a long-term holder expecting meaningful appreciation, the tax benefit usually outweighs the fee drag. For a smaller initial position, the math is tighter.

Should I Buy All at Once or Spread Purchases Out Over Time?

For most assets, lump-sum investing wins. Research across equities shows it outperforms dollar-cost averaging in roughly two-thirds of historical periods — because asset prices tend to rise over time, and sitting on the sidelines costs you part of that rise (Vanguard Research).

Gold, however, is different enough to complicate that rule. It is more volatile than a broad equity index, with 10–20% drawdowns occurring even within multi-year bull markets. For a large initial deployment — $50,000 or more — anchoring your entire cost basis to a single entry point is a real risk. Spreading purchases over 6–12 months reduces that exposure and makes the position easier to hold through early corrections, which matters more than most investors expect.

The practical approach: deploy roughly half your target allocation upfront to establish the position, then build the rest systematically over the following months. Gold's all-time high near $5,595 in January 2026, followed by a sharp spring pullback, illustrates exactly why spreading entry points has value.

What Is the Difference Between Physical Gold and a Gold ETF?

Physical gold and gold ETFs are not the same asset, even when they track the same price. Physical gold — bullion held in a vault in your name or in your possession — carries zero counterparty risk. No institution stands between you and the metal. A gold ETF is a financial security issued by a fund company. Its value tracks gold, but the underlying metal is held by a custodian on behalf of shareholders. If that institution is sanctioned, fails, or suspends redemptions, your access to the metal becomes legally and operationally complicated in ways that direct ownership is not.

The CPM Group portfolio study, the World Gold Council's allocation data, and every institutional framework in this article address physical gold — not paper claims on it. The diversification, sovereignty, and counterparty-risk properties they measure belong to the metal itself, not to a financial instrument tracking its price (CPM Group; World Gold Council).

In practice, a gold ETF is a reasonable vehicle for short-to-medium-term exposure, or as a placeholder while building toward a physical position. For the core of a long-term allocation — the portion held as a genuine store of value and systemic hedge — physical metal outside the banking system is what the research is actually measuring. In the crisis scenario this allocation is designed for, the two are simply not interchangeable.

What This Means for Your Gold Allocation

Most institutional frameworks recommend 5–15%. CPM Group's 53-year research says 20% for optimal risk-adjusted returns (CPM Group). The current macro environment reinforces that higher figure. Four consecutive years of structurally elevated central bank buying, gold displacing US Treasuries as the world's largest reserve asset for the first time in three decades (World Gold Council, 2026), and fiscal deficits that make dollar debasement a policy reality rather than a hypothetical (Congressional Budget Office, 2026) — all of these conditions argue for the higher end of your chosen range, not the lower.

The minimum is 5%. Below that, the position is too small to matter when it counts. The ceiling is wherever you would feel overexposed if gold pulled back 20% in a strong equity year — which will happen eventually, because gold is volatile even in a long-term bull market.

What physical gold offers that no stock, bond, or ETF can match is a specific combination: no counterparty risk, a genuinely constrained supply, and independence from the financial system. It works precisely when the rest of the system doesn't.

SOURCES

1. CPM Group — Optimizing Your Portfolio with Gold and Silver

2. World Gold Council — Gold Demand Trends: Full Year 2025 — Central Banks

3. World Gold Council — Gold Demand Trends: Full Year 2025

4. World Gold Council — The Relevance of Gold as a Strategic Asset — Portfolio Impact

5. World Gold Council — Gold Focus: Is Gold's Appeal Fading on Rising Volatility? (December 2025)

6. World Gold Council — Gold's Optimal Portfolio Weight in a Higher Correlated Environment (May 2025)

7. World Gold Council — Is Mined Gold Production Peaking? (January 2026)

8. J.P. Morgan Private Bank — Is It a Golden Era for Gold? (February 2026)

9. GoldSilver — The Debasement Trade Explained: Mechanism, History, and What It Means for Gold

10. Congressional Budget Office — The Budget and Economic Outlook: 2026 to 2036 (February 2026)

11. Peter G. Peterson Foundation — Interest Costs on the National Debt Are Reaching All-Time Highs (February 2026)

12. Internal Revenue Service — Topic No. 409: Capital Gains and Losses

13. Internal Revenue Service — Publication 590-A: Contributions to Individual Retirement Arrangements (IRAs)

14. Internal Revenue Service — Retirement Plans FAQs Regarding IRAs

15. Vanguard — Lump-Sum Investing Versus Dollar-Cost Averaging