Home prices are near historic highs. College tuition continues to climb. The average new car now costs more than many Americans once paid for their first home.

Measured in dollars, these increases look dramatic.

But there’s another way to evaluate long-term affordability: price those same assets in ounces of gold instead of dollars.

When we do that, the results tell a very different story.

Gold as a Measuring Stick for Real Value

For most of history, gold functioned as money — or as the anchor behind it. Even after the United States left the gold standard in 1971, gold continued to act as a benchmark for purchasing power.

Unlike fiat currency, gold’s supply cannot be expanded at will. Global mine production increases the total above-ground supply by roughly 1–2% per year on average. In contrast, fiat money supply growth can accelerate rapidly during periods of fiscal stress or economic intervention.

Since 1971:

- The U.S. dollar has lost over 88% of its purchasing power according to CPI data.

- U.S. federal debt has grown from roughly $370 billion in 1970 to nearly $37 trillion today — an increase of more than 9,000%.

- Broad money supply (M2) has grown more than 30X — with an unprecedented acceleration during 2020–2022, when it expanded by over $6 trillion in just two years.

When we price assets in gold instead of dollars, we filter out much of that monetary distortion.

The Financial System Isn’t Safer — And You Know It As risks mount, see why gold and silver are projected to keep shining in 2026 and beyond.

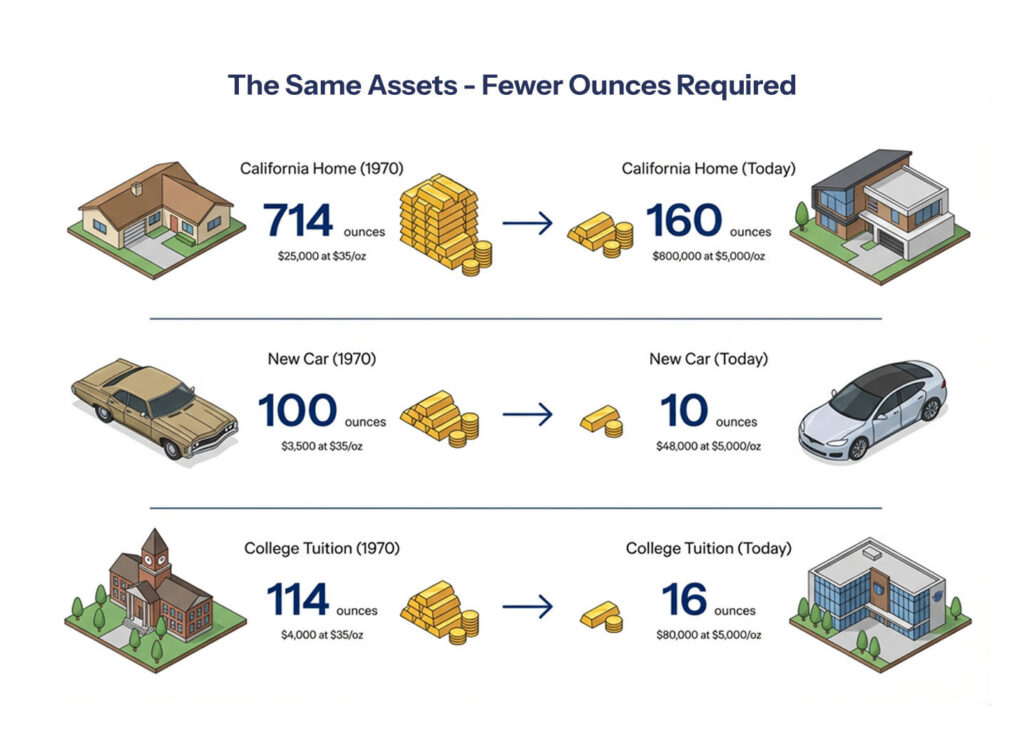

How Much Gold to Buy a House in 1970 vs. Today?

In 1970, a modest California home cost approximately $25,000. At the time, gold was priced at $35 per ounce. That meant it took roughly 714 ounces of gold to purchase a home.

Today, a comparable California home might cost around $800,000. For simplicity and clean math, we’ll use a gold price of $5,000 per ounce, which means that same home would require approximately 160 ounces of gold.

Measured in dollars, home prices have risen more than 30-fold. Measured in gold, the number of ounces required has declined by nearly 80%.

Looking at how much gold to buy a house across decades provides a clearer measure of purchasing power than nominal dollar prices alone. This comparison does not suggest that homes became “cheap.” Rather, it highlights how the purchasing power of the dollar has declined relative to a hard asset like gold.

When evaluating how much gold to buy a house over multiple decades, the evidence suggests gold has maintained — and in many cases increased — its purchasing power relative to real assets.

The dollar did not.

Cars and College Tell a Similar Story

The same pattern appears across other major life expenses.

In 1970, a new car averaged about $3,500 — roughly 100 ounces of gold at the time. Today, with new vehicles averaging around $48,000, that translates to approximately 10 ounces of gold using the same $5,000 benchmark price.

Four years of college tuition in 1970 averaged roughly $4,000, or about 114 ounces of gold. Today, an $80,000 degree equates to approximately 16 ounces of gold at $5,000 per ounce — and fewer still at current spot prices.

(Note: With gold trading above $5,300 at the time of this writing, the number of ounces required would actually be even lower — further strengthening gold’s purchasing power comparison.)

Measured in dollars, these costs appear to have exploded. Measured in gold, they have declined significantly. Over extended periods, gold has tended to preserve purchasing power even as fiat currencies gradually lose it.

For a deeper explanation of what changed when the U.S. left the gold standard, explore our Hidden Secrets of Value series.

What This Means for Long-Term Investors

For investors focused on retirement or generational wealth, the question is not simply whether asset prices are rising. The more important question is whether savings will maintain their purchasing power over time.

Since the early 1970s:

- The U.S. money supply has expanded exponentially.

- Federal debt has increased dramatically.

- Inflation has compounded year after year.

Gold operates outside that system. It does not rely on corporate earnings, government policy, or debt issuance. It carries no counterparty risk. While it does experience price volatility in the short term, its long-term role has been as a store of value.

This is one reason central banks continue accumulating gold reserves. According to data from the World Gold Council, central bank gold purchases have reached multi-decade highs in recent years. It is also why gold often performs strongly during periods of elevated inflation, monetary uncertainty, or financial stress.

When investors examine how much gold to buy a house across different decades, they are effectively evaluating gold’s ability to retain real purchasing power.

The Dollar Illusion

When people say that homes are unaffordable or that college costs are out of control, they are usually evaluating prices in nominal dollars. However, nominal prices can obscure what is actually happening beneath the surface.

If the measuring unit itself is losing value, rising prices do not necessarily reflect rising real costs. They reflect currency depreciation.

Gold provides an alternative lens. By pricing assets in ounces rather than dollars, we gain perspective on whether real value has changed — or whether the currency has.

Over the past five decades, the data suggests that much of what appears to be explosive price growth is, in part, a reflection of dollar weakness.

Is Gold a Perfect Hedge?

No asset is without limitations. Gold does not generate income. It does not produce dividends or interest. Its price can fluctuate significantly in the short term.

However, over long periods — particularly during inflationary cycles — gold has demonstrated an ability to maintain purchasing power relative to tangible assets. That characteristic makes it less of a speculative instrument and more of a strategic allocation for wealth preservation.

For investors concerned about inflation, fiscal instability, or long-term currency erosion, gold functions as a monetary anchor within a diversified portfolio.

Investors seeking direct exposure can explore physical bullion options through our resource page.

A Broader Perspective on Wealth Preservation

Ultimately, the question of how much gold to buy a house is not about predicting real estate markets. It is about understanding monetary systems and how purchasing power evolves over time.

Currencies change. Policy shifts. Debt accumulates. Economic cycles rise and fall.

Gold has remained a consistent store of value through those cycles.

For investors seeking clarity in an uncertain environment, measuring wealth in real terms — rather than nominal ones — can provide a more stable foundation for decision-making.

The numbers suggest that while dollar prices fluctuate dramatically, gold’s long-term relationship to real assets has been remarkably resilient.

That is the deeper lesson history offers.

Investing in Physical Metals Made Easy

People Also Ask

How much gold does it take to buy a house today?

At a gold price of $5,000 per ounce, an $800,000 home would require about 160 ounces of gold. With gold trading above $5,300 at the time of writing, the number of ounces required would be even lower. Measuring home prices in gold helps reveal long-term purchasing power trends rather than just nominal dollar increases.

Was it cheaper to buy a house in gold in 1970?

In 1970, a $25,000 home required roughly 714 ounces of gold at $35 per ounce. Today, a comparable home requires far fewer ounces. While dollar prices have surged, the gold comparison shows how purchasing power has shifted over time.

Why compare house prices in gold instead of dollars?

Most people don’t price homes in gold when buying or selling. However, economists and investors sometimes use gold as a benchmark to evaluate long-term purchasing power. Comparing how much gold to buy a house over time can help isolate the effects of inflation and currency expansion from real asset value.

Does gold really protect against inflation?

Historically, gold has tended to preserve purchasing power during inflationary periods, especially when real interest rates are negative. While it doesn’t produce income, it has often acted as monetary insurance during currency debasement cycles. You can follow ongoing inflation trends and gold analysis in GoldSilver News.

Is gold a better long-term store of value than the dollar?

Over the past 50 years, the dollar has steadily lost purchasing power due to inflation. Gold, by contrast, has maintained its ability to command real assets across monetary cycles. Many investors hold physical gold as part of a diversified strategy focused on long-term wealth preservation.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Past performance is not indicative of future results. Always consult a qualified financial advisor before making investment decisions.

You May Also Like:

- Gold vs. Silver: Roles, Risks, and Portfolio Strategy

- Gold Silver Prices: Short-Term Noise, Long-Term Signal

- Silver Canadian Maple Leaf: Why It’s One of the World’s Top Bullion Coins

- Gold Portfolio Allocation 2026: What J.P. Morgan’s Forecast Means for Investors

- How Government Debt Affects Gold and Silver

- Gold vs Silver: The Liquidity Difference That Matters