Published: 05-26-2026, 11:41 am | Updated: 05-26-2026, 12:17 pm

Key Takeaways

- The US dollar has not been backed by gold since August 15, 1971 — the date President Nixon formally ended dollar-to-gold convertibility under the Bretton Woods system.

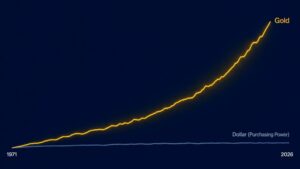

- Since leaving the gold standard, the dollar has lost approximately 87% of its purchasing power [Bureau of Labor Statistics, CPI-U]. As a result, M2 money supply has grown from ~$630 billion in 1971 to over $22 trillion in 2026 [Federal Reserve H.6 Release] — a 35x expansion.

- Central banks purchased a net 244 tonnes of gold in Q1 2026 alone [World Gold Council, Gold Demand Trends Q1 2026]. Consequently, the world’s largest reserve managers are reducing dollar exposure — a shift that accelerated after the 2022 freezing of approximately $300 billion in Russian central bank reserves [US Congressional Research Service].

What Backs the US Dollar?

So what backs the US dollar, if not gold or silver? The answer has been the same since August 15, 1971: nothing physical. The dollar is a fiat currency — from the Latin fiat, meaning “let it be done.” Its value rests on a government declaration that it is legal tender. Beyond that, it rests on trust.

That trust, however, has real and measurable consequences. As of Q3 2025, the dollar accounted for approximately 57% of global foreign exchange reserves [IMF Currency Composition of Official Foreign Exchange Reserves (COFER), Q3 2025]. No other currency comes close. Moreover, the dollar remains the default unit for international trade, oil pricing, and sovereign debt.

However, trust — unlike gold — has no physical limit on its supply. That distinction is at the heart of everything that follows. How the dollar went from redeemable metal to redeemable promise is one of the most consequential financial shifts of the past century.

The Knowledge That Changes Everything

Two essential guides — yours free. Understand why gold matters and why fiat currencies always fail.

When Did the Dollar Leave the Gold Standard?

For most of American history, dollars tied directly to precious metals. Under the classical gold standard, anyone could exchange paper dollars for a fixed weight of gold at any bank. The Bretton Woods system, established at the 1944 conference in Bretton Woods, New Hampshire, extended this logic internationally. Specifically, foreign governments could exchange dollars for gold at $35 per ounce. The dollar was, effectively, as good as gold for international trade.

That ended on August 15, 1971. President Richard Nixon announced that the US would no longer honor foreign requests to convert dollars to gold. The reason was straightforward: America spent far more than it produced. Financing the Vietnam War and Great Society programs simultaneously had drained the gold reserves. Furthermore, foreign nations — France most prominently — were accelerating their redemptions. As a result, the US simply could not honor the commitments.

Nixon called it a “temporary” measure. Fifty-five years later, however, the gold window has never reopened.

What Did Removing the Gold Standard Actually Do?

Before 1971, the gold standard was a hard ceiling on money creation. The government could not print dollars faster than it could acquire gold to back them. Remove the ceiling, and the supply expands. Indeed, that’s exactly what happened.

M2 money supply grew from approximately $630 billion in 1971 to over $22 trillion in 2026 [Federal Reserve H.6 Money Stock Measures, March 2026] — a 35x increase in just over five decades. For a deeper look at why this pattern repeats across history, see our analysis of why fiat currencies fail.

The purchasing power math is just as stark. According to the Bureau of Labor Statistics’ Consumer Price Index, a 1971 dollar buys roughly 13 to 14 cents worth of goods today [BLS CPI-U, 2026]. For example, a $100 purchase in 1971 costs nearly $800 now. In addition, gas at 36 cents a gallon now costs over $3.50. Similarly, a median home at $24,000 in 1971 now sells for over $400,000 [US Census Bureau, New Residential Sales].

Those prices didn’t go up. The dollar shrank.

The Dollar Has Lost 97% of Its Purchasing Power Since 1913

Value of $1 in 1913 dollars — what one dollar could buy, over time

Source: U.S. Bureau of Labor Statistics, CPI-U | GoldSilver

What Gives the Dollar Its Value Now?

Three structural pillars replaced gold as the foundation of dollar demand. However, none of them limits how many dollars can be created. That’s the constraint gold used to provide.

The petrodollar system. From 1974, the US reached agreements with Saudi Arabia and other oil producers to price oil exclusively in dollars. As a result, every country that imports oil — which is nearly every country — needs dollars to do it. That created sustained global demand for the currency. In recent years, the arrangement has frayed as BRICS nations pursue alternatives, but it remains a significant structural support.

US Treasury debt as a global reserve asset. Foreign governments and central banks hold trillions in US Treasury bonds as their primary reserve asset. It’s self-reinforcing: you need dollars to buy Treasuries, and you hold Treasuries because you need a place to park dollars. The long-term cost of that arrangement is visible in the dollar’s 87% purchasing power decline since 1971.

Network effects and institutional inertia. The dollar runs through global trade contracts, commodity pricing, SWIFT payment infrastructure, and international debt. Consequently, unwinding that takes decades, not quarters. De-dollarization is real — it’s just slow.

Is the Dollar Losing Its Reserve Currency Status?

Yes — but gradually. The dollar’s share of global foreign exchange reserves has fallen from approximately 72% in 2001 to about 57% in Q3 2025 [IMF COFER, Q3 2025]. That’s 15 percentage points over 25 years. In other words, not a collapse — a slow drift.

What’s changing faster, however, is where the diversification is going. Central banks bought over 1,000 tonnes of gold annually in 2022, 2023, and 2024 [World Gold Council, Central Bank Gold Reserves Survey]. Net purchases hit 244 tonnes in Q1 2026 alone [World Gold Council, Gold Demand Trends Q1 2026]. For context, the five-year average before 2022 was roughly 473 tonnes per year. Therefore, the recent three-year pace was nearly double that. For a full breakdown of who is buying and why, read BRICS gold accumulation and what it means.

In 2022, the US and its allies froze approximately $300 billion in Russian central bank reserves held in Western financial institutions [US Congressional Research Service, IF12062]. Reserve managers in Beijing, New Delhi, and Riyadh took note: dollar-denominated assets can be frozen. Gold in a sovereign vault, however, cannot.

The dollar isn’t being replaced. Nevertheless, it’s being hedged — systematically, by the world’s most sophisticated financial institutions.

Why Is the Dollar’s Problem Arithmetic, Not Politics?

People argue about the Fed, government spending, and inflation as if these are political problems with political solutions. They’re not. The constraint is math.

As of May 2026, total US gross national debt stands at nearly $39 trillion [US Treasury, Debt to the Penny; Joint Economic Committee Monthly Debt Update, May 2026]. Furthermore, annual net interest payments will reach $1 trillion in fiscal year 2026. That figure surpasses both the defense budget and Medicare individually, ranking second only to Social Security [Congressional Budget Office, Budget and Economic Outlook 2026].

In a fiat system, the only way to service $39 trillion in debt without defaulting is to keep enough dollars in circulation to make the payments. Consequently, the money supply can’t meaningfully contract. The Fed can slow its expansion, but it cannot reverse it. Moreover, even the most hawkish chair in recent memory — Kevin Warsh, sworn in May 22, 2026 [CBS News, May 22, 2026] — can’t change the arithmetic. The debt already exists.

Economists call this fiscal dominance: the condition where debt is so large that monetary policy must serve fiscal needs rather than constrain inflation. No conspiracy is required. In other words, just compounding obligations and a currency with no hard limit on its supply.

As a result, the 87% purchasing power loss since 1971 [BLS CPI-U] isn’t a political outcome. It’s the predictable consequence of removing the constraint — and then spending.

Stay On Top of Gold & Silver Prices

Get important market alerts sent straight to your inbox.

People Also Ask

Is the US dollar still backed by gold?

No. The US dollar has not been backed by gold since August 15, 1971, when President Nixon ended dollar-to-gold convertibility under the Bretton Woods system. Since then, the dollar has been a fiat currency — its value rests on government decree, institutional trust, and structural demand, not any physical commodity.

What replaced gold as the backing for the US dollar?

Three structural pillars replaced gold: the petrodollar system (from 1974, oil was priced in dollars, creating sustained global demand), US Treasury debt (foreign governments and central banks hold trillions in Treasuries as their primary reserve asset), and the dollar’s deep network effects in global trade and payment infrastructure. However, none of these pillars constrains money supply the way gold did.

Why has the dollar lost so much purchasing power since 1971?

The gold standard limited how many dollars the government could create — each dollar had to be backed by physical gold. Once that constraint was removed in 1971, the money supply expanded freely. As a result, M2 has grown from approximately $630 billion in 1971 to over $22 trillion in 2026 — a 35x expansion [Federal Reserve H.6, March 2026]. The Bureau of Labor Statistics’ CPI-U puts the cumulative purchasing power loss at approximately 87%.

Are central banks moving away from the US dollar?

Gradually, yes. The dollar’s share of global foreign exchange reserves has fallen from approximately 72% in 2001 to about 57% in Q3 2025 [IMF COFER]. Furthermore, central banks purchased over 1,000 tonnes of gold annually in 2022, 2023, and 2024, and 244 tonnes in Q1 2026 alone [World Gold Council]. The 2022 freezing of approximately $300 billion in Russian central bank reserves [US Congressional Research Service] accelerated the shift — demonstrating that dollar-denominated assets carry political risk that physical gold does not.

What is fiscal dominance and why does it matter for savers?

Fiscal dominance is the condition where a government’s debt is so large that monetary policy must accommodate it rather than constrain inflation. The US carries nearly $39 trillion in national debt [US Treasury, May 2026], with net interest payments projected to exceed $1 trillion in fiscal year 2026 [CBO]. Because of this, the money supply must keep growing to service existing debt — which is structurally bearish for the purchasing power of savings held in that currency.

What Should Individual Investors Do About It?

Start with an accurate picture of the system. The dollar works fine as a medium of exchange. However, it has never been a reliable long-term store of value — not since 1971.

Physical gold and silver have preserved purchasing power across centuries. They do so precisely because geology constrains their supply, not policy decisions. Specifically, gold’s annual mine supply grows at roughly 1–2% per year [World Gold Council, Supply Data 2025]. No government can authorize more of it into existence.

This isn’t an argument for abandoning dollar-denominated assets. Instead, it’s an argument for understanding what backs each asset you hold. Central banks around the world — the most sophisticated reserve managers on the planet — have reached the same conclusion. Moreover, they have been acting on it for three years running.

If you’ve read this far, you already understand more about what backs the US dollar — and what doesn’t — than most people ever will. The next step is a practical one. Create a free GoldSilver account to start buying physical gold and silver — the same assets central banks have been quietly accumulating while most investors weren’t paying attention.

SOURCES

1. Bureau of Labor Statistics — CPI-U: Purchasing Power of the Consumer Dollar

2. Federal Reserve — H.6 Money Stock Measures, March 2026

3. IMF — Currency Composition of Official Foreign Exchange Reserves (COFER), Q3 2025

4. World Gold Council — Gold Demand Trends Q1 2026

5. Gold Demand Trends — Central Bank Gold Reserves Survey (World Gold Council)

6. Annual Gold Supply Data 2025 — World Gold Council

7. Congressional Research Service — IF12062: Russia’s War on Ukraine: Financial and Trade Sanctions

8. US Treasury — Debt to the Penny, May 2026

9. Joint Economic Committee — Monthly Debt Update, May 2026

10. Congressional Budget Office — Budget and Economic Outlook 2026

11. US Census Bureau — New Residential Sales

12. CBS News — Kevin Warsh Sworn In as Federal Reserve Chair, May 22, 2026

Disclaimer: This article is for informational and educational purposes only. It does not constitute investment advice. Please consult a qualified financial adviser before making any investment decisions.

You may also like:

- Why Is Gold Valuable? The 5,000-Year Answer Most Investors Get Wrong

- 72% of Family Offices Hold No Gold. What They’re Missing.

- Gold Remonetization: Six Forces Restoring Gold’s Monetary Role

- Silver Industrial Demand: Solar, EVs, and the Supply Gap

- Bank of America’s $6,000 Gold Forecast Isn’t a Price Call. It’s a System Call.

- Silver IRA Complete Guide: Rules, Limits, and Custodians Explained

- Silver’s Tesla Moment: The Solid-State Battery Thesis

- Physical Gold vs. Digital Gold: Which Is the Ultimate Safe Haven?