Published: 05-19-2026, 03:24 pm

Key Takeaways

- The mechanism, not the headline: BRICS gold buying matters not because a new currency is imminent. It matters because it reduces demand for US Treasuries at the margin — slowly eroding the dollar’s reserve role and the purchasing power of dollar savings.

- Physical over paper: The hedge you want for a dollar debasement scenario is physical gold and silver. ETFs and futures carry counterparty risk in the exact conditions you’re protecting against.

- Position before the headline: BRICS central banks are building reserves now, not after the announcement. The time to position is while the shift is still being dismissed.

- Silver complements gold: Silver offers the same monetary properties as gold with higher volatility and a lower entry price per ounce. It’s a natural complement to a gold core position.

Most news coverage of the BRICS gold story gets one thing wrong: it treats this as political drama rather than a portfolio signal.

It asks whether a BRICS currency will succeed. Whether it’ll topple the dollar. Whether the summit announcements are serious or just rhetoric. Those are interesting questions. However, they’re also the wrong ones if you’re trying to protect and grow your savings.

The more useful question is this: If the world’s largest emerging economies are buying gold as a reserve asset, what does that mean for the purchasing power of your dollars over the next decade?

That question has an answer. Let’s work through it.

Your Gold Buying Guide Most investors overpay when they buy gold. Then overpay again when they sell. This guide shows you exactly what to own — and why.

What’s Actually Driving the BRICS Gold Accumulation?

Start with the structural reality, because the portfolio implication flows directly from it.

The global monetary system rests on a simple but fragile premise. At its core, the US dollar is the world’s reserve currency. Global trade is priced in dollars. Foreign central banks hold dollar-based assets — primarily US Treasuries — as their primary reserves. This arrangement gives the United States something no other country has. It can run persistent deficits, issue debt at scale, and effectively export inflation simply by printing money.

BRICS+ nations have spent years building an alternative to that arrangement. The group now includes Brazil, Russia, India, China, and South Africa, plus six new full members admitted in 2024 and 2025: Egypt, Ethiopia, Iran, the UAE, Indonesia, and Saudi Arabia. Together, they have built settlement systems that bypass SWIFT, bilateral trade agreements in local currencies, and — most critically — a systematic accumulation of physical gold at the central bank level.

As we covered last month, central banks globally bought 1,037 tonnes of gold in 2023. That was the second-highest annual total on record. Moreover, they exceeded that pace in 2024 with 1,045 tonnes [World Gold Council, Gold Demand Trends Full Year 2023]. China’s People’s Bank of China added gold for 18 consecutive months through April 2024.

It then paused for six months as prices hit records, resumed in November 2024, and has continued buying since [Bloomberg, December 2025]. Russia has effectively replaced its dollar reserves with gold. India’s Reserve Bank repatriated 100 tonnes from the Bank of England in spring 2024, then a further 102 tonnes by year-end.

The common thread is simple. Gold cannot be frozen. It cannot be sanctioned. It belongs to whoever holds it physically. No government can revoke that.

Does a Gold-Backed Currency Need to Succeed for This to Matter?

No. And that’s the point most commentators miss.

The BRICS proposal for a gold-backed trade currency is usually framed as binary. Either it replaces the dollar, or it fails and nothing changes. Neither is right.

A gold-backed settlement unit doesn’t need to replace the dollar. It just needs to exist as a credible option for bilateral trade between willing parties. If China and Saudi Arabia can settle oil in a unit partly backed by gold, they have one less reason to hold US Treasuries. As a result, demand for dollar-based debt falls at the margin. The US government’s ability to borrow cheaply becomes slowly constrained.

That’s the mechanism. Not a dramatic collapse — but a slow tightening of the conditions that make dollar dominance sustainable.

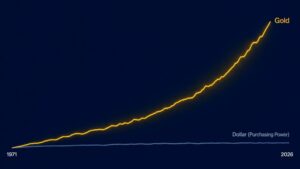

The dollar’s share of global foreign exchange reserves has already fallen from roughly 72% in 2001 to around 58% today [IMF Currency Composition of Official Foreign Exchange Reserves (COFER), 2024]. That 14-point decline happened quietly over two decades. It didn’t make front pages. Instead, it showed up as higher consumer prices, a more constrained Federal Reserve, and a steady erosion of dollar purchasing power.

That’s how these shifts work. Not with a bang.

Why Hasn’t Your Financial Advisor Mentioned Any of This?

Because they’re not paid to.

The financial advisory industry is built around US market assets. Fee structures, product shelves, and compliance frameworks all centre on dollar-based investments. Recommending that a client move a meaningful portion of their portfolio outside that system is awkward at best. At worst, it opens conversations advisors would rather avoid.

This isn’t a conspiracy. It’s an incentive structure. Moreover, it creates a gap that a well-constructed portfolio can exploit.

The answer isn’t to abandon conventional assets. Instead, it’s to add a layer of physical gold and silver that sits entirely outside the dollar system. Not a gold ETF. Not a gold miner stock. Metal you own outright, with no counterparty between you and the asset.

How Should You Actually Position for This?

Step 1: Know what you’re hedging. This isn’t a crash hedge — though gold tends to perform well in crises too. The real risk is slow-moving. It’s a structural decline in the purchasing power of the dollar relative to hard assets, playing out over 10 to 20 years. The BRICS gold buying is one of the clearest signals that this risk is rising.

Step 2: Own the metal, not the contract. Gold ETFs and futures track the gold price. However, they’re claims on gold, not gold itself. In normal conditions, the distinction barely matters. In a monetary stress scenario — precisely what you’re hedging against — it matters enormously. Paper gold fell 10% during the inflation war. Physical told a different story. When the hedge is most needed, paper breaks down.

Step 3: Size it for a multi-decade thesis. Standard guidance places precious metals at 5–10% of a diversified portfolio. Given accelerating central bank buying, rising BRICS+ coordination, a declining dollar reserve share, and an unconstrained US fiscal trajectory, 10–15% in physical gold and silver is a defensible position. Not a speculation — an insurance policy sized to the risk.

Step 4: Move before the headline does. By the time a BRICS gold-backed currency is functioning and on the front page, the positioning window will largely have closed. The central banks buying gold right now aren’t waiting for confirmation. Neither should you.

Where Does Silver Fit?

Gold dominates the de-dollarization conversation. It’s the reserve asset central banks actually buy. But that creates an opening, because central banks can’t accumulate silver at scale. Individual investors can.

Silver carries the same monetary properties as gold: scarcity, durability, and no counterparty risk. At roughly 1/62nd the price per ounce at current market levels, the gold-to-silver ratio sits near its long-run historical average [GoldSilver, The Gold-Silver Ratio Is Expanding — and Being Misread, May 2026].

In addition, silver has a growing industrial demand floor. Solar panels, electric vehicles, and AI data centre framework all require it. Gold doesn’t have that same industrial backstop. That demand floor doesn’t replace the monetary thesis — it reinforces it.

Silver also moves faster than gold in both directions. That volatility is the feature, not the bug, for investors willing to hold through it. The logical structure: gold as the anchor, silver as the higher-upside complement.

Stay On Top of Gold & Silver Prices

Get important market alerts sent straight to your inbox.

People Also Ask

Is a BRICS gold-backed currency actually going to happen?

A fully gold-backed BRICS reserve currency is unlikely in the near term. The eleven member nations have conflicting economic interests and no shared monetary authority. However, the framework is already being built. Central banks are accumulating gold at record levels. Bilateral trade is increasingly settled in local currencies. Payment systems outside the dollar framework are expanding. The currency doesn’t need to launch for the structural pressure on the dollar to be real.

Why are central banks buying so much gold right now?

The trigger was the 2022 freezing of around $300 billion in Russian foreign exchange reserves. Central banks across emerging markets drew the obvious conclusion: dollar-based assets can be seized; domestically held gold cannot. That realisation accelerated a shift already underway. Central banks have been net buyers every year since 2010. However, the annual pace roughly doubled after 2022 — from a prior average of 473 tonnes to over 1,000 tonnes in each of 2022, 2023, and 2024 [World Gold Council].

Does the dollar losing reserve status mean it will collapse?

No. The decline from roughly 72% of global reserves in 2001 to around 58% today took more than two decades. Moreover, the dollar remains the world’s dominant reserve currency by a wide margin. The risk isn’t collapse. Instead, it’s a sustained erosion of purchasing power as the dollar’s structural advantages slowly weaken and the US government’s cost of borrowing rises.

What is the difference between physical gold and a gold ETF?

A gold ETF is a financial contract that tracks the gold price. The holder owns fund shares, not metal. Physical gold is the metal itself — in your possession or in allocated storage in your name. In ordinary conditions, the distinction barely matters. However, under monetary stress — exactly when gold is most valuable as a hedge — ETFs introduce counterparty risk. The fund must remain solvent. The custodian must remain trustworthy. Physical gold has none of those dependencies.

How much of my portfolio should be in gold and silver?

Conventional guidance puts precious metals at 5–10% of a diversified portfolio. Investors with a strong view on long-term dollar debasement often argue for 10–15% in physical gold and silver combined. The right number depends on your time horizon, your existing dollar-asset exposure, and how much of your wealth you want held entirely outside the financial system.

The Signal the Market Is Sending

The BRICS gold story isn’t really about a currency. That’s the surface layer.

What’s underneath is a collective verdict. Central banks representing more than 40% of global GDP — measured at purchasing power parity — are moving out of dollar-based assets and into gold. They are voting with their reserves. This has been going on for years. The scale is without modern precedent outside the Bretton Woods transition itself.

You don’t have to believe the BRICS alternative succeeds. You just have to take the signal seriously. These institutions know their own balance sheets, their inflation dynamics, and what persistent dollar dominance has cost them. And they’re hedging accordingly.

Owning physical gold and silver isn’t a bet against the dollar. Instead, it’s a recognition that the dollar faces structural pressures decades in the making. Those pressures are intensifying. An asset that has preserved purchasing power through every prior monetary transition deserves a place in your portfolio.

That’s financial sovereignty. And if you’re ready to act on it, you can open an account here.

SOURCES

1. World Gold Council — 2024 Central Bank Gold Reserves Survey

2. World Gold Council — Gold Demand Trends Full Year 2023: Central Banks

3. IMF — Currency Composition of Official Foreign Exchange Reserves (COFER)

4. Federal Reserve — The International Role of the U.S. Dollar, 2025 Edition

5. Bloomberg — China Resumes Buying Gold Reserves After 6-Month Halt, December 2024

6. Bloomberg — China’s PBOC Extends Gold-Buying Streak, December 2025

7. Business Standard — RBI Brings Home 102 Tonnes of Gold from Bank of England, October 2024

8. BRICS Official — About the BRICS

9. GoldSilver — The Gold-Silver Ratio Is Expanding — and Being Misread, May 2026

Disclaimer: This article is for informational and educational purposes only. It does not constitute investment advice. Please consult a qualified financial adviser before making any investment decisions.

You may also like:

- Gold to Oil Ratio: The Ultimate Guide for Economic & Portfolio Analysis

- Dollar-Cost Averaging Into Gold and Silver: The Investor’s Practical Guide

- The Silver-to-Dow Ratio: How to Spot the Shift from Paper to Physical

- What Moves Gold Prices? 6 Key Gold Price Factors Explained

- World Bank: Precious Metals to Surge 42% This Year

- Silver Price Outlook May 2026: Stop Chasing the Number

- Dollar Dominance Is Fading. Gold and Silver Are Paying Attention.

- GoldSilver: Home Storage and Vault in One Account