Published: 02-23-2026, 10:30 am | Updated: 02-23-2026, 04:25 pm

Daily News Nuggets | Today’s top stories for gold and silver investors

February 23rd, 2026 | Brandon Sauerwein, Editor

Two major banks have updated their gold price forecast for 2026 — and the numbers are hard to ignore.

Gold Gains as Trump Tariff Plan Hits Legal Roadblock

Gold prices climbed after a federal court blocked former President Trump’s attempt to expand tariffs. The ruling briefly rattled markets and reignited debate over U.S. trade policy. For now, the proposed duties are halted — introducing fresh legal and political uncertainty over what comes next.

Investors responded quickly. The U.S. dollar weakened, Treasury yields slipped, and gold and silver edged higher.

Stay On Top of Gold & Silver Prices

Get important market alerts sent straight to your inbox.

The dynamic is worth understanding. Tariffs can push prices higher by raising import costs. But prolonged trade disputes also risk slowing global growth — and that creates a real tension for markets.

Inflation pressure on one side. Growth risk on the other. That’s precisely the kind of backdrop that tends to favor gold.

When policy uncertainty rises, markets struggle to price the next move. Capital tends to rotate toward assets seen as stable and politically neutral. Gold fits that description well.

The legal pause may delay further tariff escalation. But it doesn’t resolve the underlying uncertainty — and markets know it.

BMO Equity Research: Gold Could Reach $6,500 in 2026

BMO Equity Research has released an aggressive gold price forecast for 2026 — and it’s turning heads. The firm says gold prices could surge to $6,500 an ounce by 2026. The forecast rests on three converging forces: persistent inflation risks, elevated geopolitical tensions, and continued central bank buying. Emerging markets, in particular, are actively diversifying away from the U.S. dollar.

BMO argues that structural demand for gold remains strong — even if rate cuts unfold gradually. That’s a notable point. Gold’s bull case no longer depends on the Fed moving quickly.

The bank is more cautious on silver. It cites industrial demand uncertainty and tighter supply dynamics as factors that could limit near-term upside.

The bigger takeaway is the framing. If BMO’s outlook proves right, gold isn’t just a crisis hedge anymore. It’s becoming a strategic allocation in an increasingly unstable global financial system.

BMO isn’t alone in that view. JPMorgan is making an even bolder case.

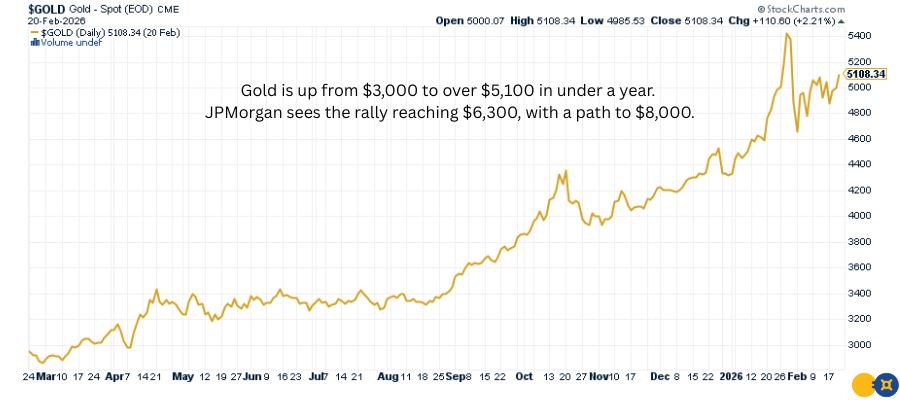

JPMorgan Lifts Gold Target to $6,300, Makes Case for $8,000

JPMorgan’s latest gold price forecast for 2026 and beyond represents one of the most bullish calls on Wall Street. The bank now forecasts prices could reach $6,300 per ounce in the coming cycle — with a potential path to $8,000 under more extreme macro conditions. This isn’t a momentum call. JPMorgan sees structural support driving the move.

The drivers are worth naming. Sustained central bank accumulation — especially among emerging markets. Rising fiscal deficits in developed economies. Growing concerns over long-term currency debasement. Geopolitical fragmentation reinforcing gold’s appeal as a neutral reserve asset.

But the most important part of JPMorgan’s call is what it isn’t about. This isn’t tied to rate cuts. The bank argues gold’s rally is decoupling from traditional real-rate dynamics. Instead, it’s being anchored by broader systemic risk — sovereign debt sustainability, shifts in global reserve strategy, and the slow erosion of confidence in fiat-based systems.

That’s a meaningful distinction. If gold no longer needs a dovish Fed to rally, the ceiling looks very different.

Not every institution is sounding alarm bells. But even the measured voices are recommending cover.

UBS CIO Sees Resilient Growth — But Advises Defensive Positioning

UBS’s Chief Investment Office isn’t telling investors to head for the exits. It’s urging them to stay invested — but to do so carefully. The firm points to resilient economic growth and selective opportunities across asset classes. Long-term fundamentals, it argues, still support equities — particularly in quality sectors with strong balance sheets.

But the tone is measured. UBS flags elevated fiscal deficits, shifting central bank policy paths, and geopolitical tensions as live risk factors. Its recommendation: balanced portfolios with high-quality bonds, selective alternative assets, and geographic diversification.

That’s a notable combination. Stay in the market — but build in protection.

UBS isn’t forecasting a sharp downturn. It’s also not dismissing one. In that kind of environment, strategic allocation matters more than conviction calls. The firm’s message is clear: position for growth, but make sure your portfolio can absorb a policy surprise or macro shock.

It’s a cautious endorsement of resilience — from an institution that has every incentive to stay optimistic. For institutional investors, these are portfolio strategy questions. For millions of Americans, the stakes are far more personal.

The Financial System Isn’t Safer — And You Know It As risks mount, see why gold and silver are projected to keep shining in 2026 and beyond.

America’s Retirement Gap Gets Harder to Ignore

A new report puts a number on a problem most people already sense. The median retirement savings for many American households is just $955. Millions of people approaching retirement have less than $1,000 set aside. They’ll need those funds to last 20 to 30 years.

The reasons are familiar — but no less troubling for it. Many workers lack access to employer-sponsored retirement plans. Those who do often struggle to contribute consistently. Meanwhile, persistent inflation has driven up the cost of groceries, housing, and healthcare. Saving has become harder at the exact moment it matters most.

Social Security offers a floor — but a limited one. It typically replaces only about 40% of pre-retirement earnings. That gap forces real choices: work longer, spend less, or lower expectations.

The deeper issue is purchasing power. Building wealth matters. But for millions of Americans, the more urgent challenge is making sure the wealth they have doesn’t quietly erode over time.

That’s what makes diversification — and inflation-resistant assets — less of an investment strategy and more of a necessity.