KEY TAKEAWAYS:

- Gold’s 2% dip was margin liquidation from the oil spike — not fundamental selling

- The Hormuz blockade adds energy inflation to an already stagflationary backdrop (CPI 3.3%, rate cuts priced out)

- Central banks continue buying: PBOC 17th straight month, Goldman targeting $5,400

- The petrodollar required a naval blockade to defend — gold requires nothing

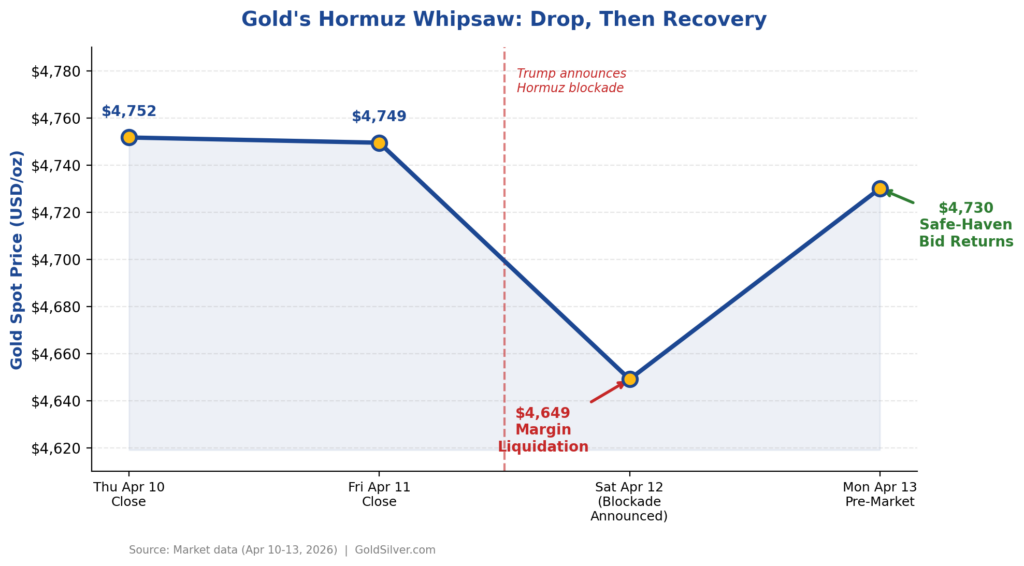

Gold dropped roughly 2% in early trading Monday after President Trump ordered the U.S. Navy to blockade the Strait of Hormuz, sending oil above $100 a barrel for the first time in over a year.

Silver took an even harder hit, falling nearly 4%.

But here’s the part that matters more than the headline number: gold started recovering almost immediately. By mid-morning, spot gold had clawed back above $4,700 — and the reasons for that recovery tell you far more about where this market is heading than the initial dip.

How 21 Hours of Failed Diplomacy Closed 20% of the World’s Oil Supply

The blockade announcement came Sunday evening after 21 hours of U.S.-Iran nuclear talks collapsed in Islamabad. Vice President Vance returned without a deal. The sole sticking point: Iran’s nuclear program.

Trump’s response was blunt. On Truth Social, he ordered the Navy to blockade “any and all ships” trying to enter or leave the Strait — the chokepoint that carries roughly 20% of the world’s seaborne oil. CENTCOM confirmed enforcement would begin at 10 a.m. ET Monday.

Oil reacted exactly the way you’d expect. Brent crude surged more than 7%. Energy stocks ripped higher. And gold — the asset that’s supposed to rise when the world gets dangerous — dropped.

Your Gold Buying Guide Most investors overpay when they buy gold. Then overpay again when they sell. This guide shows you exactly what to own — and why.

Why Did Gold Drop When Geopolitical Risk Rose?

This is where it gets educational for anyone holding physical metal or thinking about starting a position.

When oil spikes suddenly, it triggers margin calls across commodity markets. Traders who are leveraged in energy positions need to post collateral fast, and the easiest way to do that is to sell their most liquid asset. That’s gold.

This is margin liquidation — forced selling that has nothing to do with gold’s fundamental value. It’s a plumbing problem, not a thesis problem.

The evidence: gold’s recovery started within hours. Safe-haven demand reasserted once the initial margin shock cleared. This is a pattern that repeats in virtually every geopolitical crisis that spikes energy prices. Gold dips on the liquidity squeeze, then rallies on the structural bid.

The Structural Case Just Got Stronger

Here’s what the Hormuz blockade changes for the medium-term gold thesis:

Energy inflation is back. CPI already printed 3.3% — the hottest reading since May 2024. With oil above $100 and Iran threatening to close the Bab el-Mandeb strait through the Houthis (another 12% of global energy supply), the inflation pipeline just got longer and wider. The Fed’s rate cuts for 2026? Priced out entirely.

Central banks aren’t slowing down. China’s PBOC just bought gold for the 17th consecutive month. Goldman Sachs raised its end-2026 gold target to $5,400 an ounce. JPMorgan sees $5,055 by Q4. These aren’t retail speculators chasing momentum — they’re institutions front-running what they see as a structural shift in global reserves.

The petrodollar just got defended by military force. This is the detail that the sound money community noticed immediately. Chinese vessels were among the primary ships transiting the Strait, purchasing Iranian crude in yuan — the most advanced live experiment in petrodollar displacement ever attempted. Under this arrangement, oil-exporting nations receive yuan rather than dollars, reducing demand for U.S. currency in global trade settlement. When that experiment operates at scale through a critical global chokepoint, it represents a direct challenge to dollar hegemony. Trump’s blockade kills that experiment by interdicting vessels operating outside the dollar system. When a currency system requires a naval blockade to enforce, it tells you something about the durability of the alternative: gold doesn’t need a navy.

What This Means for You

The 10-year Treasury yield has climbed to 4.40%, up 45 basis points in recent weeks. That sounds like it pays you to hold cash. But with CPI at 3.3% and rising energy costs feeding through the supply chain, the real yield on your savings — what you actually earn after inflation — is thinner than it looks. And if oil stays above $100, it gets thinner still.

Gold doesn’t pay a yield. But it doesn’t lose purchasing power to an inflation rate that the central bank can’t control without triggering a recession either.

That’s the trade-off every saver faces in a stagflationary environment: accept a shrinking real return on paper assets, or hold something that has preserved purchasing power through every monetary crisis for 5,000 years.

The Hormuz blockade didn’t change gold’s fundamental story. It sharpened it.

Gold closed Friday at $4,749.46. Weekend trading saw prices drop to approximately $4,649. By Monday morning, spot gold had recovered to approximately $4,730.

Investing in Physical Metals Made Easy

People Also Ask

Why did gold drop when the Strait of Hormuz was blockaded?

Gold fell initially because an oil price spike triggers margin calls across commodity markets. Traders holding leveraged energy positions are forced to sell their most liquid asset — gold — to post collateral quickly. This is margin liquidation, not fundamental selling. It has nothing to do with gold’s underlying value and typically reverses within hours once the liquidity shock clears, which is exactly what happened Monday.

What is the Strait of Hormuz and why does it matter for gold?

The Strait of Hormuz is a narrow waterway between Iran and Oman that carries roughly 20% of the world’s seaborne oil supply. When it is threatened or closed, energy prices spike, inflation expectations rise, and real yields on cash and bonds compress — all conditions that historically drive institutional and retail demand for gold as a store of value outside the financial system.

Is gold a good hedge against stagflation?

Gold has historically performed well in stagflationary environments — periods where inflation stays elevated while economic growth slows. When real yields (the return on savings after inflation) turn negative or compress, the opportunity cost of holding gold falls. With CPI at 3.3%, oil above $100, and rate cuts priced out for 2026, the current environment fits that pattern closely. Central banks at the PBOC and major institutions including Goldman Sachs and JPMorgan are positioning accordingly.

SOURCES

1. World Gold Council — China PBOC Gold Reserves Data

2. Goldman Sachs — Gold Price Outlook 2026

3. JPMorgan — Commodities Research: Gold Price Forecast Q4 2026

4. U.S. Central Command (CENTCOM) — Strait of Hormuz Enforcement Statement

5. U.S. Energy Information Administration — Strait of Hormuz: World’s Most Important Oil Transit Chokepoints

6. U.S. Bureau of Labor Statistics — Consumer Price Index, March 2026

7. U.S. Department of the Treasury — 10-Year Treasury Yield

This article is for informational purposes only and does not constitute financial or investment advice. Always consult a qualified financial advisor before making investment decisions.

You May Also Like

- $88 Billion a Month: Why U.S. Debt Is Driving Gold Prices

- CPI Hits 3.3%, GDP Stalls — Is Stagflation 2026 Here?

- War Risk, Stagflation Signals, and a $6,300 Gold Target

- Gold and Oil Brace for the Strait of Hormuz Deadline

- Iran War Deadline Puts Gold and Silver Prices on Edge

- Why Is Gold Falling When the World Is on Fire?

- Gold Jumps 2% as Trump Plans Iran War Address Tonight