Published: 06-22-2026, 02:10 pm

Key Takeaways

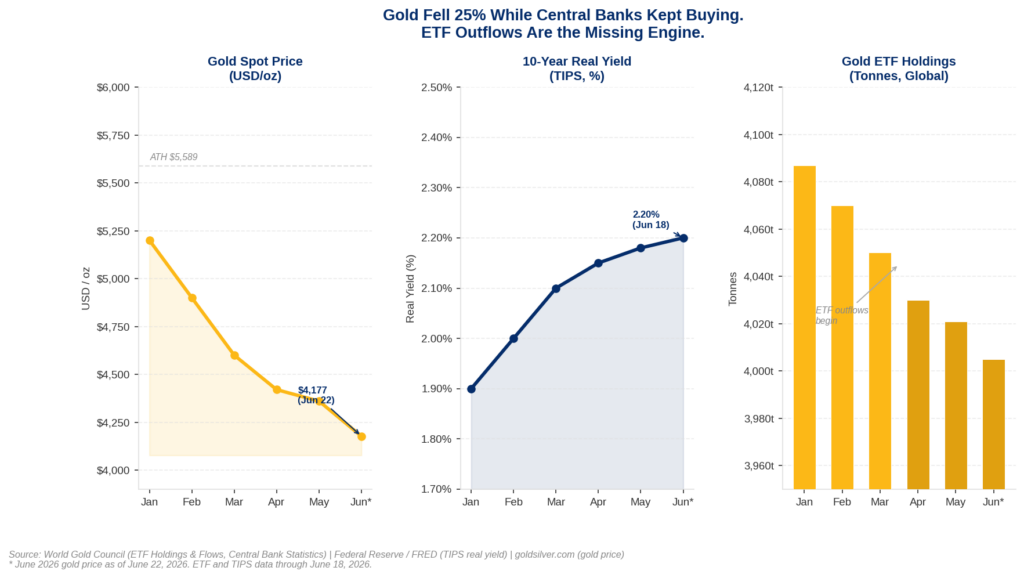

- Gold is at $4,177 today. That is down roughly 25% from its January 2026 all-time high of $5,589. It is still up approximately 28% year-over-year.

- Morgan Stanley maintains an upside bias for gold in H2 2026. Its $5,200 target depends on one specific buyer type returning to the market.

- Bank of America’s June 2026 fund manager survey found that 58% of 198 managers overseeing $540 billion expect stagflation. Gold’s “overvalued” reputation is at its lowest point since February 2024.

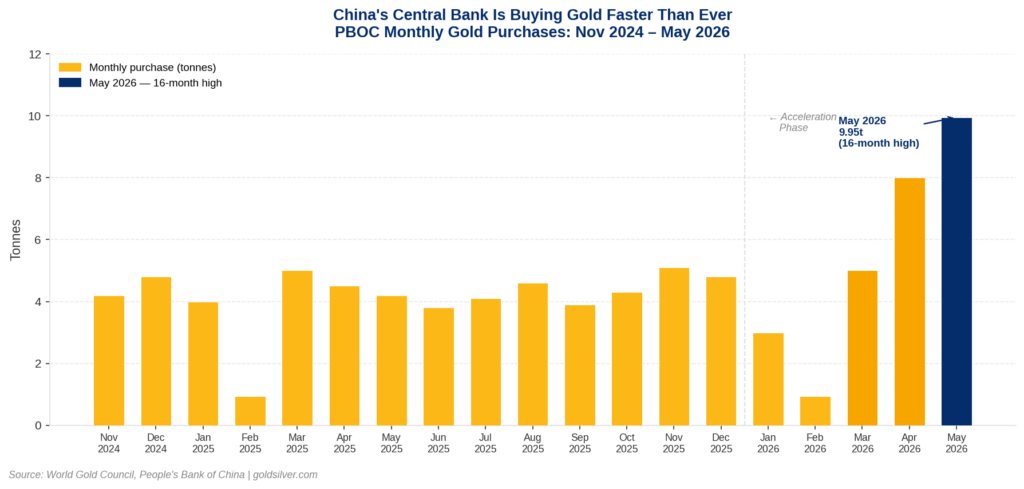

- The People’s Bank of China bought nearly 10 tonnes in May alone. It has now bought gold for 19 consecutive months. Global central banks purchased an estimated 244 tonnes in Q1 2026.

- Historical data shows gold averaged +0.84% in the month after a 25-basis-point Fed hike. In three specific tightening cycles, gold actually rallied as rate hikes triggered growth fears.

- The structural case does not reverse on a single FOMC cycle. Watch energy prices and real yields, not just the Fed statement.

What Is Happening to the Gold Price Right Now?

In January 2026, gold hit $5,589 an ounce. Today it sits at $4,177.

That $1,400 decline has produced two kinds of investors. One group is anxious. The other group understands what is actually happening. The gap between them comes down to one question: which of the three forces that drive gold are currently on, and which one is temporarily off?

Morgan Stanley’s commodities team answered that question in a recent research note. Their conclusion, stated plainly: the structural case for gold in the second half of 2026 remains intact. The $5,200 target is still mathematically reachable. However, getting there requires one specific buyer type to return. That buyer type is the most sensitive to the Federal Reserve.

Understanding the chain is more useful than watching the price.

Which Three Forces Drive Gold — and Which Two Are Already There?

Think of the gold market as having three distinct demand engines. Each one operates on a different time horizon. Each responds to different signals.

Engine one: official sector buying. This means central banks, sovereign wealth funds, and reserve managers. These institutions make decisions on 20-year time horizons. They do not respond to quarterly earnings calls. Furthermore, this engine has been running at record or near-record pace for three consecutive years.

According to data reported by the People’s Bank of China on June 7, 2026, and confirmed by the World Gold Council, the PBOC added approximately 9.95 tonnes in May 2026. This was the largest single-month purchase in 16 months. It extended the buying streak to 19 consecutive months. Since resuming purchases in November 2024, the PBOC has accumulated approximately 67 tonnes. Meanwhile, global central banks purchased an estimated 244 tonnes in Q1 2026, according to the World Gold Council. That exceeded both the previous quarter and the five-year average.

A separate WGC survey found that a record 45% of central banks globally plan to increase their gold allocation in the next 12 months. When the institutions that manage national wealth on a generational timescale are accelerating their buying through a 25% price correction, that is not a signal from momentum traders. It is a signal from institutions that believe something structural has changed about the monetary system.

Engine two: stagflation expectation. Bank of America’s June 2026 Global Fund Manager Survey covered 198 managers overseeing $540 billion in assets under management. The survey ran from June 5 to June 11. It found that 58% of respondents expect stagflation as their dominant economic outlook for the next 12 months. That means stagnant growth combined with persistent inflation.

That combination is historically one of the strongest environments for gold. Gold does not care whether the economy is growing or shrinking. It cares about real returns on competing assets. Therefore, when real yields are elevated but growth is stalling, the case for holding non-yielding physical metal improves structurally.

The BofA survey revealed something else worth noting. Earlier in 2026, approximately 45% of these same managers called gold overvalued. That was the highest such reading since 2012. That number has since fallen to its lowest level since February 2024. In other words, the institutional consensus that gold was a crowded trade has quietly reversed. The skeptics have thinned.

Engine three: Western ETF demand. This is the engine that is currently off. Additionally, it is the one Morgan Stanley is watching most closely.

Why Have Gold ETFs Stopped Buying?

Morgan Stanley commodities strategists Amy Gower and Martijn Rats identified the issue precisely. According to their June 2026 research note, ETF demand is the missing piece. It is likely to remain sensitive to the Federal Reserve’s path, real yields, and the dollar.

That sentence contains a chain worth following carefully.

ETF investors are primarily Western institutional and retail allocators. They make decisions on a quarterly or annual basis. Their opportunity cost of holding gold (which pays no yield) is tied directly to what they could earn holding Treasury bonds instead.

When real yields on 10-year Treasury Inflation-Protected Securities are sitting around 2.2%, as they are today, the math of holding a non-yielding asset becomes harder to defend in a quarterly review. As a result, ETF investors reduce their gold exposure.

Following the June 16 to 17 Federal Open Market Committee meeting, Fed Chair Kevin Warsh held rates steady. However, he signaled that further tightening may be needed. Nine of nineteen Fed policymakers now project at least one rate hike before year-end. Markets are pricing in a hike as early as October. Higher-for-longer rate expectations have driven 10-year nominal yields to around 4.48% this week. That environment has produced net outflows from gold ETFs.

The gating mechanism, fully traced: the Fed’s hawkish posture drives up real yields. Higher real yields raise the opportunity cost for ETF holders. That produces ETF outflows. Those outflows weigh on the gold price.

That chain is real. It explains what has been happening since January. However, the chain also runs in both directions.

The Knowledge That Changes Everything

Two essential guides — yours free. Understand why gold matters and why fiat currencies always fail.

What Changes the Math for Gold ETFs?

Morgan Stanley’s note identifies Middle East de-escalation as an unexpected structural tailwind. Specifically, it is a tailwind for the ETF demand that has not arrived yet.

Here is the mechanism. When Middle East tensions drove oil prices higher earlier this year, oil-importing central banks faced a dual squeeze. Energy costs were inflating their import bills. Their currencies were weakening simultaneously. As a result, some were forced to sell gold reserves to defend their fiscal balances. That selling pressure created a headwind inside the official sector itself.

As the Iran situation de-escalates and oil prices fall, that pressure reverses. Brent crude has been below $80 this month. Central banks that were selling gold to defend their currencies now have breathing room. Moreover, lower oil prices, if they feed through to broader inflation data, begin to soften the case for the Fed’s higher-for-longer stance.

The sequence Morgan Stanley describes is this: softer energy prices reduce inflation readings, which reduces the probability of additional rate hikes, which lowers real yields, which reduces the opportunity cost for ETF investors. The missing engine starts.

Their $5,200 target is not a price prediction in isolation. It is a thesis about the sequencing of those forces.

Does a Hawkish Fed Automatically Mean Lower Gold Prices?

There is a widely held belief that Fed rate hikes are bad for gold. Like most widely held beliefs in financial markets, it is partially true and mostly incomplete.

Morgan Stanley’s note provides the historical data. On average, gold has gained 0.84% in the month following a 25-basis-point Fed hike. That is not much. However, it is also not the loss that the “higher rates equal lower gold” narrative would predict.

More revealing are the specific episodes where gold actually rallied through a tightening cycle. In June 2006, December 2018, and March 2023, gold decoupled from the rate-hike narrative entirely. In each case, the common thread was the same. The rate hikes triggered broader growth concerns, fear of policy error, or acute financial system stress. When investors start wondering whether the Fed has tightened too much, they reach for real assets. When that doubt emerges while inflation is still running above target, gold becomes the most logical expression of that uncertainty.

Therefore, Morgan Stanley’s strategists are watching for a specific environment: a Fed that has hiked into slowing growth, produced a softening in energy-driven inflation, but has not yet credibly solved the structural purchasing power question. In that environment, the gold thesis becomes self-reinforcing.

What Does This Mean for the Individual Gold Investor?

Here is what the three-engine analysis means in practice. This applies to someone who already holds physical gold, or to someone deciding whether to.

The two engines that operate on the longest time horizons are currently active at historically elevated levels. These are official sector buying and stagflation expectation. Central banks do not buy 19 months straight, then suddenly reverse course because of one FOMC meeting. Similarly, fund managers who expect stagflation do not abandon real assets the quarter before stagflation materializes.

The engine that is off is Western ETF demand. It is the most short-term and the most sensitive to rate expectations. It is also, by definition, the most likely to reverse when those rate expectations shift. That shift does not require a rate cut. It requires evidence that inflation is cooling enough to make the next hike optional rather than certain. Lower oil prices are one such evidence point. They are already present in the current data.

What this analysis describes is a structural floor. It has been built by actors with 20-year time horizons. It has been accelerating even through a 25% price correction. Layered on top of that floor is a cyclical overhang from one category of buyer whose return depends on the Fed’s next move.

This is what sound money has always been, in every era where it has mattered: an asset whose case does not depend on the central bank’s next decision. The decision that matters was made by the people who decided to hold it.

Stay On Top of Gold & Silver Prices

Get important market alerts sent straight to your inbox.

People Also Ask

Why is gold falling when inflation is still high?

Gold’s short-term price is being pulled down by elevated real yields. Real yields are the inflation-adjusted return available on Treasury Inflation-Protected Securities. They raise the opportunity cost of holding a non-yielding asset like gold. The Federal Reserve’s hawkish posture has pushed 10-year real yields to around 2.2%. As a result, Western ETF investors have reduced their exposure. This is a cyclical dynamic layered over a structural one. Meanwhile, central banks and long-horizon investors continue buying at record pace regardless of quarterly rate expectations.

What does Morgan Stanley’s $5,200 gold price target depend on?

Morgan Stanley commodities strategists Amy Gower and Martijn Rats identified Western ETF demand as the missing piece for gold to reach $5,200. According to their June 2026 research note, ETF buying is sensitive to the Fed’s rate path, real yields, and the dollar. For ETFs to return, investors need evidence that the Fed’s tightening cycle is near its end. That evidence would likely come through softer energy prices flowing into lower inflation readings. Lower inflation readings, in turn, would reduce the probability of additional rate hikes.

Is 58% of institutional managers expecting stagflation significant for gold?

Yes. Stagflation combines slow economic growth with persistent inflation. That combination is historically a strong environment for gold. When growth stalls, traditional growth assets underperform. When inflation persists, cash and bonds lose purchasing power in real terms. Gold, as a real asset with no counterparty risk, sits at the intersection of both dynamics. Bank of America’s June 2026 survey finding that 58% of 198 fund managers overseeing $540 billion expect stagflation is one of the clearest institutional signals of the macro backdrop gold is currently operating within.

Why has the People’s Bank of China been buying gold for 19 consecutive months?

The PBOC’s sustained accumulation reflects a strategic shift in reserve management. It is not tactical price-chasing. Reserve managers at the PBOC operate on multi-decade horizons. Gold offers three properties central banks prioritize: safety (no counterparty risk), liquidity (globally traded), and portfolio diversification away from dollar-denominated assets. China’s gold now represents approximately 9% of its foreign exchange reserves. Furthermore, the buying continued through three consecutive months of gold price declines. That confirms it is strategic, not speculative.

Does a hawkish Fed automatically mean lower gold prices?

Not necessarily. Historical data cited in Morgan Stanley’s June 2026 research note shows gold averaged +0.84% in the month following a 25-basis-point Fed rate hike. In specific tightening cycles — June 2006, December 2018, and March 2023 — gold actually rallied as rate hikes triggered growth fears or financial system stress. Gold’s relationship with rates is more nuanced than the simple “higher rates equal lower gold” narrative. What matters is whether rate hikes successfully address inflation without triggering growth concerns. When they do not, gold benefits even in a rising-rate environment.

What is the difference between gold ETFs and physical gold for long-term investors?

Gold ETFs provide price exposure to gold. However, they typically do not give the holder legal ownership of a specific bar of metal held in their name. Physical gold — allocated, segregated bars and coins held in a secure facility — gives the holder direct, unencumbered ownership with no counterparty risk. When ETF investors reduce their holdings, they are adjusting a financial position. Physical gold holders are not in that same flow. For investors who own gold as a long-term monetary hedge rather than a quarterly portfolio trade, the ETF outflow dynamic is less relevant. The structural case for physical ownership is built on the same foundations driving central bank buying: safety, financial sovereignty, and a hedge against purchasing power erosion over decades.

SOURCES

1. Investing.com via Yahoo Finance — Gold faces hurdle on path to $5,200 as hawkish Fed dampens ETF demand, MS says

2. Crypto Briefing — Bank of America survey shows gold least overvalued in 2.5 years as stagflation fears dominate

3. TradingView / MaceNews — BofA Global Research Fund Manager Survey, June 5–11 2026

4. Bloomberg — China’s Central Bank Extends Gold-Buying Streak in May

5. World Gold Council — Central Bank Gold Statistics: Central Banks Resume Net Buying in April

6. World Gold Council — China Gold Market Update: A Notable Rise in Gold Reserves

7. Federal Reserve Bank of St. Louis / FRED — 10-Year TIPS Real Yield (DFII10)

8. Morgan Stanley Research — Gold’s Safe-Haven Status Faces a Reality Check

9. World Gold Council — Gold Demand Trends Q1 2026: Central Banks

Disclaimer: This article is for informational purposes only and does not constitute financial or investment advice. Always consult a qualified financial adviser before making investment decisions.

You may also like:

- Solar Cut 19% Silver. The Deficit Widened Anyway.

- Gold Down 26%. Barclays’ $4,791 Target Never Moved.

- Gold Silver Ratio at 64: What It Signals for Silver in 2026

- How Central Banks Decide How Much Gold to Hold

- How Much Does Gold Storage Cost? The $72-a-Year Answer

- Silver Price Outlook June 2026: The Correction Was the Setup

- Wall Street’s $6,000 gold call rests on data most investors never see

- Silver Eagle vs. Maple Leaf vs. Britannia: Which Gives You More Silver?