Published: 05-28-2026, 09:52 am

Key Takeaways

- The 60/40 portfolio’s core diversification premise has broken down. The negative stock-bond correlation that made bonds a reliable equity hedge turned positive in 2022 and has stayed elevated — bonds now move with equities during drawdowns rather than offsetting them. [Incrementum AG, In Gold We Trust 2025]

- Three major Wall Street institutions now recommend gold allocations beyond 5%. Morgan Stanley Chief US Equity Strategist Mike Wilson proposed a 60/20/20 model (60% equities, 20% short-term bonds, 20% gold). BlackRock Investment Institute Head Jean Boivin and Goldman Sachs commodities analyst Lina Thomas have both called gold a permanent portfolio holding, not a tactical trade. [Morgan Stanley; BlackRock Investment Institute; Goldman Sachs]

- The shift is really a verdict on government bonds. Recommending gold as a bond replacement is a judgment that fiscal deficits have made the traditional “safe” asset fundamentally less safe — and that a real asset outside the financial system is needed to fill the gap. [Morgan Stanley; Goldman Sachs]

The Model That Broke

For forty years, the 60/40 portfolio was the default prescription for the serious investor: sixty percent equities for growth, forty percent bonds for ballast. The model worked because stocks and bonds moved in opposite directions when markets got scared. Bonds rose when equities fell, cushioning the blow. That relationship is broken, and the institutions that built trillion-dollar businesses on it know it.

In the past 18 months, Morgan Stanley, BlackRock, and Goldman Sachs have independently arrived at the same revision: replace a significant portion of the bond allocation with gold. The models differ in specifics — Wilson proposed 60/20/20, Boivin called for “structural” gold beyond 5%, Thomas recommended the same.

However, the direction is identical. When three of the most mainstream research desks on Wall Street reach the same conclusion on gold portfolio allocation independently, the underlying data has changed.

As of May 2026, Morgan Stanley, BlackRock, and Goldman Sachs all recommend a gold portfolio allocation of 10–20% in diversified portfolios — a significant departure from the 2–5% “strategic hedge” that defined mainstream financial planning for decades. [Morgan Stanley; BlackRock Investment Institute; Goldman Sachs] The catalyst is a broken correlation: since 2022, stocks and bonds have moved together during drawdowns, eliminating the diversification benefit that was the entire premise of the classic 60/40. [Incrementum AG, In Gold We Trust 2025]

According to Incrementum AG’s In Gold We Trust 2025 report, a higher gold portfolio allocation has produced meaningfully better risk-adjusted returns under current conditions. Gold is trading at $4,446 per ounce (as of May 27, 2026), up approximately 35% year-over-year. Not because of a crisis. Not because of war. Because the math on the existing model no longer works, and the institutions have finally run it.

The Knowledge That Changes Everything

Two essential guides — yours free. Understand why gold matters and why fiat currencies always fail.

Is the 60/40 Portfolio Still a Good Strategy?

The 60/40 portfolio is not dead, but its core diversification mechanism is compromised. The model was built on a specific empirical pattern: equities and investment-grade bonds tend to be negatively correlated during market stress.

When growth fears drove stocks down, investors fled to Treasuries, pushing bond prices up and yields down. That “flight to safety” dynamic made a 40% bond position function as automatic insurance. When your equities bled, your bonds typically didn’t.

That negative correlation held from roughly 1998 to 2021. [Incrementum AG, In Gold We Trust 2025] Then 2022 broke it. The Federal Reserve began its fastest rate-hiking cycle in 40 years. Stocks and bonds fell simultaneously. The S&P 500 dropped 19.4%. Long-duration Treasuries dropped more than 30%. For investors holding the classic 60/40, it was the worst year for that construction in modern financial history.

That deeper problem is this: 2022 was not an anomaly. The conditions that broke 60/40 — sustained inflation running above bond yields — remain in place.

When inflation exceeds the yield on “safe” bonds for an extended period, those bonds stop diversifying a portfolio. Instead, they become a second source of loss rather than a hedge against the first. Reassessing gold portfolio allocation is, therefore, not a market call — it is a structural response to a broken model.

The mechanism is precise. The 60/40 portfolio’s diversification benefit requires negative stock-bond correlation. That correlation is determined by the type of shock hitting the economy.

A pure growth shock — recession without inflation — pushes stocks down and bonds up. 60/40 works. An inflation shock pushes both down. 60/40 fails. [Incrementum AG, In Gold We Trust 2025] Furthermore, the current environment — inflationary with elevated fiscal deficits — raises the probability of inflation shocks persisting throughout the coming decade.

Why Are Institutional Investors Adding Gold to Portfolios?

The institutional case for gold rests on three independent arguments: gold’s near-zero correlation with both equities and bonds under current conditions, its track record during inflationary regimes, and the demand floor created by central bank accumulation. [Morgan Stanley; BlackRock Investment Institute; Goldman Sachs]

Morgan Stanley Chief US Equity Strategist Mike Wilson put the most specific stake in the ground: a 60/20/20 model. Sixty percent equities. Twenty percent short-duration bonds — explicitly not long-duration, to limit interest rate sensitivity. Twenty percent gold. [Morgan Stanley] Wilson’s case centred on gold’s near-zero correlation with both equities and short-duration bonds. He also pointed to gold’s performance in prior inflationary regimes as further evidence.

BlackRock Investment Institute, led by Jean Boivin, went further than an allocation number. Their research called gold a “structural” holding — a term with a specific meaning in institutional portfolio theory. A structural allocation belongs in a portfolio based on the asset’s inherent properties, regardless of timing or price level. [BlackRock Investment Institute]

This is categorically different from “buy gold because the price looks good.” It means gold belongs in the portfolio permanently, by design, not as a trade.

Goldman Sachs commodities analyst Lina Thomas built her case on three distinct pillars. [Goldman Sachs] First, central bank buying has created a persistent price floor for gold. Second, real yield dynamics have historically favoured gold even in higher-rate environments when deficits are large. Third, gold provides a diversification premium that no other asset replicates when stock-bond correlation is positive.

Three independent research desks reached the same conclusion. That convergence is the signal. The correlation structure of global financial markets has changed. As a result, the portfolio theory that served investors for two decades was built for a world that no longer exists — and getting gold portfolio allocation right is now the central question.

What Happens to Bonds When Inflation and Stocks Both Fall?

In an inflationary environment with rising rates, bonds lose value on two fronts at once: inflation erodes their real purchasing power, and rising yields push their market price down. This double-hit is what makes bonds unreliable as portfolio insurance today. It also explains why gold, not cash or other bonds, is the sound replacement.

Consider the mechanics. A bond is a fixed cash flow promise: lend $1,000 today, receive $30 per year for ten years, get $1,000 back at maturity. If inflation runs at 3%, real return is approximately zero. At 5% inflation, purchasing power erodes every year the bond is held.

Now add rising rates to that picture. When new bonds are issued at 5%, a bond paying 3% falls in market price. The result is simultaneous purchasing-power loss and price decline. That is exactly what happened in 2022, and in the inflationary 1970s before that.

Gold has none of those vulnerabilities. It carries no fixed cash flow for inflation to erode. Unlike bonds, gold is not a nominal instrument — it is a real asset whose value tracks the purchasing power relationship between major currencies, not the level of any central bank’s policy rate. [World Gold Council]

Both gold and bonds get called “safe havens,” but they protect against different threats. A bond hedges equity volatility in low-inflation environments. Gold hedges currency debasement in any environment.

The US government is currently running a deficit of approximately $1.8 trillion per year. [US Congressional Budget Office, FY2024] That level of deficit spending raises the long-run probability of sustained inflation. Consequently, long-duration bonds become a liability disguised as insurance in this environment — and gold becomes the actual insurance.

How Much Gold Should Be in a Portfolio?

The institutional consensus, as of 2025–2026, is that a sound gold portfolio allocation in a diversified long-term portfolio falls between 10% and 20%. [Morgan Stanley; BlackRock Investment Institute; Goldman Sachs; Incrementum AG] This is a major departure from the 2–5% “strategic allocation” that defined financial planning for decades. That old figure was calibrated for low inflation and negative stock-bond correlation — neither of which reliably holds today.

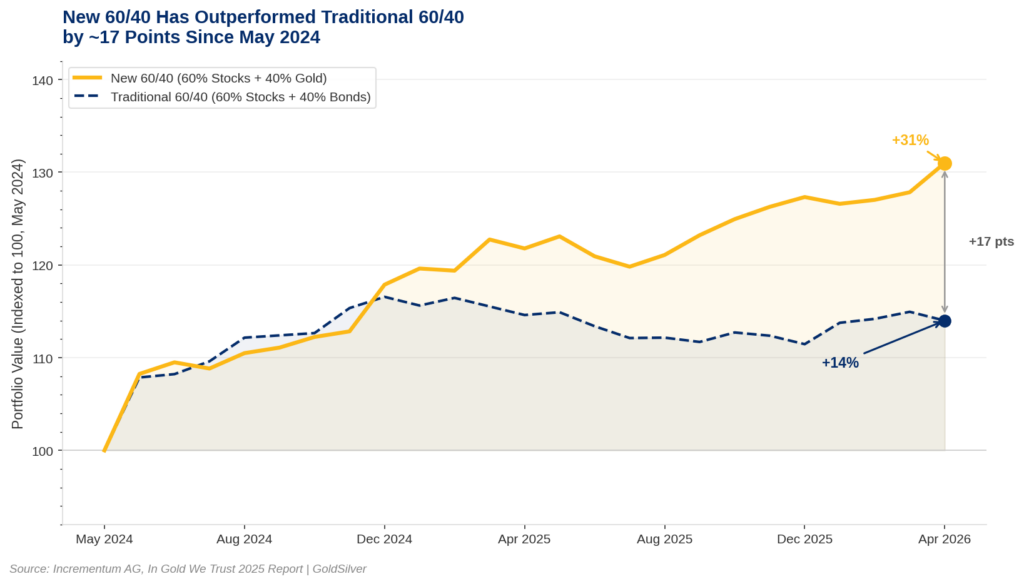

Incrementum AG’s annual In Gold We Trust report argues that a 20% gold weighting produces superior risk-adjusted returns under the conditions most likely to prevail over the next decade: above-target inflation, elevated fiscal deficits, and persistently positive stock-bond correlation. [Incrementum AG, In Gold We Trust 2025] Their “New 60/40” model — 60% equities, 40% gold, replacing bonds entirely — outperformed the classic version from May 2024 through the period covered in the 2025 report.

Morgan Stanley’s 60/20/20 is a middle path. It keeps a 20% short-duration bond position as a growth-shock hedge while giving gold a permanent 20% stake. [Morgan Stanley] The model doesn’t argue that bonds are worthless. Short-duration bonds still work when the shock is a recession without inflation. However, the old 40% weighting dramatically overstates their reliability in the current regime.

Ten percent is the lower bound in most institutional “structural gold” research. Twenty percent is the upper bound Morgan Stanley has explicitly recommended for gold portfolio allocation. [Morgan Stanley] The right figure for any individual depends on inflation expectations, time horizon, and risk tolerance. Nevertheless, 2–5% is no longer defensible on the evidence.

What Does the Performance Data Actually Show?

According to Incrementum AG’s In Gold We Trust 2025 report, a “New 60/40” portfolio — 60% equities, 40% gold — has outperformed the traditional 60/40 by approximately 17 percentage points on a total return basis since May 2024. [Incrementum AG, In Gold We Trust 2025]

The reason is arithmetic, not magic. Gold returned approximately 70%+ over the two years from mid-2024 to mid-2026 — validating what the case for a higher gold portfolio allocation predicted. By contrast, investment-grade bonds returned roughly 2–4% in nominal terms over the same period.

A portfolio holding gold instead of bonds captured a vastly better return from its non-equity sleeve — not because gold “ran,” but because bonds failed to do their job.

The counter-argument deserves a direct answer: gold’s two-year run was exceptional, and past performance doesn’t predict future returns. Fair. Yet the institutional rebuttal is equally fair. The conditions behind gold’s performance — fiscal deficits, above-target inflation, positive stock-bond correlation, central bank buying — are the defining features of the post-2020 monetary regime. Moreover, no credible mechanism for their rapid reversal currently exists. [Incrementum AG, In Gold We Trust 2025; Goldman Sachs]

Incrementum AG’s In Gold We Trust 2025 report also includes a long-range scenario model called the Gold Allocation 2045. Under a base-case debasement scenario, it projects gold prices of up to $20,800 per ounce by 2045. [Incrementum AG, In Gold We Trust 2025]

This is a scenario projection, not a price forecast. Specifically, it shows what the model produces when current trends — dollar debasement, central bank accumulation, de-dollarization — are extended at their present pace. Whether the specific figure proves right or not, the directional logic is consistent with everything the institutional research is signalling today.

What Is the Institutional Shift Actually Saying?

The Morgan Stanley / BlackRock / Goldman revision to portfolio theory is not primarily a recommendation about gold — it is a verdict on the reliability of government bonds as a safe asset. [Morgan Stanley; BlackRock Investment Institute; Goldman Sachs]

On the surface: three prominent institutions like gold. Look closer: they no longer trust long-duration bonds to perform the risk-management function they were given. That is a serious judgment about where we stand in the monetary cycle.

These institutions haven’t arrived here because gold is a compelling trade. Instead, they’ve arrived here because the alternative — counting on government bonds as reliable portfolio insurance — requires believing that governments will not continue running the deficits they are currently running. The data does not support that belief. [US Congressional Budget Office; International Monetary Fund] Revising gold portfolio allocation upward is, in that sense, a fiscal judgment more than an investment one.

In plain terms, the bond market is financing government spending at a scale that erodes the risk-free status bonds have historically held. When Morgan Stanley recommends a 20% gold position, the embedded message is this: the asset that was supposed to protect you from equity risk is now itself exposed to fiscal and monetary risk. You need something outside the system. [Morgan Stanley]

Most headlines cover the allocation recommendation. They miss the indictment underneath it. As we recently explored, nearly three-quarters of the world’s most sophisticated private investors hold no gold at all — which means the institutional consensus is moving faster than even the most sophisticated individual allocators have yet to act.

Stay On Top of Gold & Silver Prices

Get important market alerts sent straight to your inbox.

People Also Ask

Is the 60/40 portfolio dead?

Not dead, but compromised at its core. The model depends on stocks and bonds moving in opposite directions during downturns — a pattern that held from roughly 1998 to 2021, then broke in 2022 when the Fed’s rate-hiking cycle pushed both asset classes lower simultaneously. [Incrementum AG, In Gold We Trust 2025]

As long as inflation stays elevated and deficits persist, that diversification benefit is unreliable — which is precisely why gold portfolio allocation has moved to the centre of institutional portfolio debate.

What percentage of my portfolio should be in gold?

The institutional consensus as of 2025–2026 is 10–20%. Morgan Stanley’s Mike Wilson explicitly recommended 20%; BlackRock and Goldman Sachs have both published research supporting allocations beyond 5%. [Morgan Stanley; BlackRock Investment Institute; Goldman Sachs] The traditional 2–5% figure was set for a low-inflation, negative-correlation environment that no longer reliably exists.

Why are major banks recommending more gold now?

Because long-duration bonds — the traditional equity hedge in a 60/40 portfolio — are now exposed to the same forces threatening equities: deficits, monetary expansion, and above-target inflation. [Goldman Sachs; Morgan Stanley] The case for gold is not a bet on the gold price. It is an acknowledgment that bonds have lost a meaningful portion of their risk-free status.

How has gold performed compared to bonds since 2024?

Gold returned approximately 70%+ from mid-2024 to mid-2026, versus roughly 2–4% in nominal terms for investment-grade bonds. [Incrementum AG, In Gold We Trust 2025] A “New 60/40” portfolio replacing bonds with gold outperformed the traditional model by approximately 17 percentage points since May 2024. Gold is currently trading at $4,446 as of May 27, 2026, up approximately 35% year-over-year.

What is the difference between physical gold and a gold ETF for portfolio purposes?

A gold ETF provides price exposure, but the underlying asset sits on a counterparty’s balance sheet. Physical gold eliminates that risk: the investor owns the asset directly, with no institutional intermediary. [World Gold Council]

Most institutional research on gold portfolio allocation references ETF exposure. However, physical ownership delivers the same return with the added protection of direct ownership — which matters most when gold’s protective properties are needed most.

What This Means for Individual Investors

The institutional shift matters not because you should replicate Morgan Stanley’s model exactly. Rather, it matters because it removes the social friction from acting on the logic. Deciding on gold portfolio allocation used to be a contrarian move. Telling your financial advisor “I want 20% in gold” is a different conversation when you can cite Morgan Stanley’s Chief US Equity Strategist, BlackRock’s Investment Institute, and Goldman’s commodity desk. [Morgan Stanley; BlackRock Investment Institute; Goldman Sachs]

One distinction worth holding: the institutional models largely reference ETFs and futures. Physical gold offers something those products don’t — no counterparty, no custodian, no intermediary between the investor and the asset. The institutional models recommend exposure to the price of gold. Physical ownership delivers the asset itself. That difference is most consequential in the scenarios where gold’s protective properties matter most.

The case for a 10–20% gold portfolio allocation is now institutional consensus, not contrarian opinion. [Morgan Stanley; BlackRock Investment Institute; Goldman Sachs; Incrementum AG, In Gold We Trust 2025] Evidence is no longer the issue. Whether your allocation reflects it — that is.

Create your free GoldSilver account and start building the physical gold position that Morgan Stanley, BlackRock, and Goldman are now telling their clients they should have had all along.

SOURCES

1. Morgan Stanley — Investment Insights & Research

2. BlackRock Investment Institute — Research & Commentary

3. Goldman Sachs — Insights & Research

4. Incrementum AG — In Gold We Trust 2025

5. World Gold Council — The Relevance of Gold as a Strategic Asset

6. US Congressional Budget Office — The Budget and Economic Outlook: FY2024

7. International Monetary Fund — Fiscal Monitor

Disclaimer: This article is for informational and educational purposes only. It does not constitute investment advice. Please consult a qualified financial adviser before making any investment decisions.

You may also like:

- What Does the SILVER Act Mean for Precious Metals Investors?

- What Backs the US Dollar? Not Gold. Not Silver.

- Why Is Gold Valuable? The 5,000-Year Answer Most Investors Get Wrong

- 72% of Family Offices Hold No Gold. What They’re Missing.

- Gold Remonetization: Six Forces Restoring Gold’s Monetary Role

- Silver Industrial Demand: Solar, EVs, and the Supply Gap

- Bank of America’s $6,000 Gold Forecast Isn’t a Price Call. It’s a System Call.

- Silver IRA Complete Guide: Rules, Limits, and Custodians Explained