Most people assume money is tangible — printed at a mint, backed by something real, finite in supply. The reality is stranger.

The U.S. dollar is created through debt, multiplied through lending, and sustained by collective agreement. Understanding how that works is one of the most clarifying things an investor can do — and the mechanics have only grown more relevant since Mike Maloney first explained them in the video below.

What’s the Difference Between Money and Currency?

First, let’s start with what a dollar actually is.

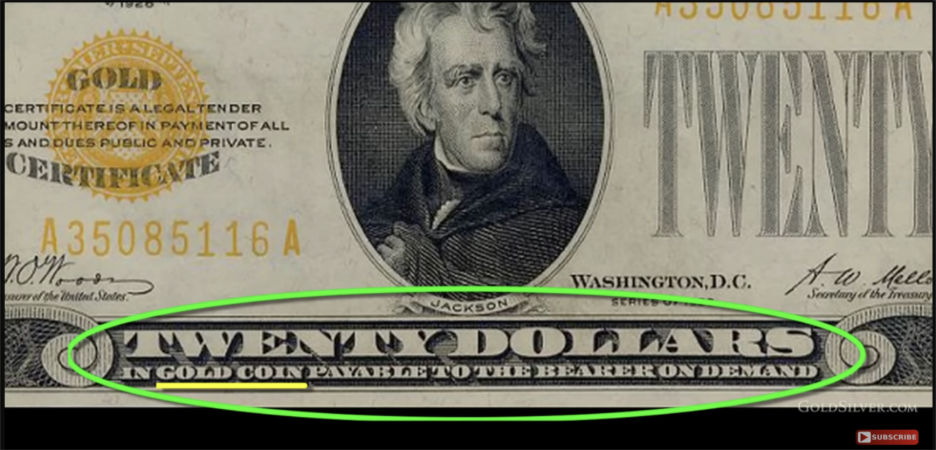

Before World War One, every U.S. note said so right on its face: a claim on physical gold held at the Treasury, redeemable on demand. The paper wasn’t the value. The gold in the vault was. Think of it like a dry cleaner’s ticket — the ticket isn’t the shirt.

That language — payable to the bearer on demand — wasn’t decorative. It was a legal obligation. Anyone holding that bill could walk into a bank and exchange it for the equivalent weight in gold coin. The note derived its value entirely from that guarantee.

Today’s dollar carries no such backing. It’s a receipt for a debt — an IOU that circulates because people agree it has value. Gold and silver, by contrast, have functioned as monetary instruments for more than 5,000 years. They’re portable, durable, divisible, fungible, and finite. Most importantly, they hold purchasing power across long stretches of time.

That’s the distinction between money and currency. It isn’t semantic — it determines how you think about what you’re holding.

How Does the Fed Actually Create Dollars?

The process starts at the U.S. Treasury, which issues bonds to finance government spending. Banks buy those bonds at auction. The Federal Reserve then buys them back from the banks — writing a check to do so.

Here’s the catch: that check is drawn on no existing deposit. The Fed doesn’t move money from one account to another. It creates it. The Federal Reserve Bank of Boston put it plainly in its own published material: when the Fed writes a check, there is no bank deposit on which that check is drawn — writing it is the creation of money [Federal Reserve Bank of Boston, Putting it Simply, 1984].

The Treasury deposits those funds, the government spends them, and newly created dollars flow into the economy. They arrive as debt. Every dollar borrowed into existence must eventually be paid back with interest — meaning more must be borrowed in the future just to cover what’s owed today. The system doesn’t merely tolerate perpetual debt growth. It requires it.

Get Expert Insights from Alan Hibbard Learn from Alan Hibbard, a trusted voice in precious metals delivering clear, actionable analysis on gold, silver and the global economy.

How Does Lending Multiply the Money Supply?

Base currency is just the entry point. Lending is where the real expansion happens. The Federal Reserve Bank of New York described it directly: banks create money by monetizing the private debts of businesses and individuals [Federal Reserve Bank of New York, I Bet You Thought, 1977]. When a bank makes a loan, new money isn’t transferred from somewhere — it comes into existence at the moment of lending.

Historically, U.S. banks operated under a 10% reserve requirement. Keep $10 of every $100 in deposits; lend the rest. That constraint created a textbook multiplier effect: one dollar of base currency could theoretically support ten dollars in total deposits across the system, through successive rounds of lending and redepositing.

In March 2020, the Fed eliminated reserve requirements entirely — setting ratios to zero for all depository institutions [Federal Reserve Board, Regulation D, effective March 26, 2020]. Banks now hold reserves voluntarily, governed by capital requirements and the interest the Fed pays on balances. The formal ceiling on credit expansion is gone.

Fractional reserve money multiplier: how $100 grows to $570 across 8 lending rounds at a 10% reserve ratio

Starting deposit

$100

After 8 rounds

$570

Theoretical max

$1,000

Based on historical 10% reserve ratio, for illustrative purposes. Reserve requirements were set to zero in March 2020.

And to be clear, this example assumes a historical 10% reserve ratio for illustrative purposes. The actual reserve requirements were set to zero in March 2020. Removing that floor didn’t slow credit creation. It eliminated the last formal constraint on it.

Either way, the result is the same: a currency supply built almost entirely from debt. Every dollar in circulation is either an IOU or a receipt for one.

Why Does the System Need Debt to Keep Growing?

Loan repayments destroy money. Every mortgage payment, credit card payoff, and bond redemption pulls currency back out of circulation. To keep the money supply from shrinking, new borrowing must constantly outpace those repayments. Miss that threshold, and the supply contracts.

This isn’t a flaw in the design. It is the design. Consumer price inflation is a lagging indicator — it reflects what already happened in the credit markets, often months or years prior. By the time prices move, the currency supply has already told the story.

The numbers show how far this dynamic has run. Gross federal debt stood at approximately 122% of GDP in Q4 2025, nearly twice the 50-year historical average of around 50% [Federal Reserve Bank of St. Louis, FRED, series GFDEGDQ188S, March 2026]. The Congressional Budget Office projects publicly held debt alone reaching 118% of GDP by 2035 — which would surpass the previous record set in 1946 [CBO, The Budget and Economic Outlook: 2025 to 2035, January 2025]. Annual interest on the national debt reached $970 billion in FY2025, more than defense spending and the third-largest federal expenditure after Social Security and Medicare [U.S. Treasury, Monthly Treasury Statement, FY2025].

Each round of quantitative easing, each emergency bond purchase program, each rate cut to stimulate borrowing — these aren’t evidence that the system is healthy. They’re what intervention looks like when a debt-dependent system runs out of runway.

When the Currency Supply Expands, Where Does That Leave Gold?

Gold and silver are priced in fiat currency. When the supply of that currency grows faster than the supply of the metals, prices adjust. That’s not a theory — it’s arithmetic.

It took the U.S. 200 years to build a monetary base of $825 billion. After the 2008 financial crisis, it tripled in roughly two and a half years. Then came COVID: the base peaked at approximately $6.4 trillion in December 2021 — more than seven times the pre-crisis level [Federal Reserve Bank of St. Louis]. It has since pulled back to around $5.4 trillion, but remains more than six times what it was before the first crisis hit.

History doesn’t offer many examples of that gap closing gently. Across thousands of years of monetary systems, the pattern is consistent: currencies expand, the gap widens, and physical assets reprice. The specific mechanism varies but the outcome doesn’t.

The structural conditions Maloney described here — debt-dependent money creation, perpetual credit expansion, a currency supply with no hard ceiling — are more pronounced today than when he first described them. That’s not an argument. It’s what the data shows.

Investing in Physical Metals Made Easy

People Also Ask

How does the Federal Reserve create money out of nothing?

The Federal Reserve creates money by purchasing government bonds from banks and paying with newly created reserves — not funds transferred from elsewhere. The Federal Reserve Bank of Boston stated this directly in its 1984 publication Putting it Simply: when the Fed writes a check, there is no prior bank deposit backing it. Writing the check is itself the act of creating money. That base money then enters the banking system, where lending multiplies the total supply further.

What is fractional reserve lending?

Fractional reserve lending is the practice of extending loans beyond the reserves a bank actually holds. Under the historical U.S. framework, a 10% reserve requirement allowed each dollar of base currency to support up to ten dollars in total deposits through successive rounds of lending and redepositing. In March 2020, the Federal Reserve eliminated reserve requirements for all depository institutions, setting ratios to zero [Federal Reserve Board, Regulation D, effective March 26, 2020]. Credit creation continues — now without a mandated floor.

What is the difference between money and currency?

Money stores value reliably over long periods. Currency facilitates exchange but may not hold its value over time. Gold and silver qualify as money: they are portable, durable, divisible, fungible, and physically finite. The U.S. dollar is currency: it enables transactions but is backed by government debt, not physical assets, and can be expanded through the credit system without a hard limit.

Why do gold and silver prices tend to rise when the money supply expands?

Gold and silver exist in finite physical supply. Fiat currency does not. When currency in circulation grows substantially faster than available metal supply, the price of that metal — denominated in that currency — rises to reflect the new ratio. This relationship has held across monetary systems and historical periods. It’s why people buy gold when they don’t trust what’s happening to the currency.

What is the Mandrake mechanism?

The Mandrake mechanism describes the full chain of debt-based money creation in modern banking — named for a comic strip character known for conjuring things from nothing. It runs from government bond issuance, through Federal Reserve money creation, to commercial bank credit multiplication through lending. The term was popularized by G. Edward Griffin in The Creature from Jekyll Island (1994).

SOURCES

1. Federal Reserve Bank of Boston — Putting it Simply (1984)

2. Federal Reserve Bank of New York — I Bet You Thought (1977)

3. Federal Register — Regulation D: Reserve Requirements of Depository Institutions (March 2020)

4. Federal Reserve Bank of St. Louis — FRED: Federal Debt as Percent of GDP, series GFDEGDQ188S

5. Congressional Budget Office — The Budget and Economic Outlook: 2025 to 2035 (January 2025)

6. U.S. Treasury Fiscal Data — Monthly Treasury Statement: Summary of Receipts and Outlays, FY2025

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Past performance is not indicative of future results. Always consult a qualified financial advisor before making investment decisions.