For most Americans, something feels off.

You work harder. You earn more. Yet your money buys less.

Groceries. Insurance. Healthcare. Rent. Utilities.

It’s not your imagination. The U.S. dollar has been quietly losing purchasing power for over a century — and the system driving that decline is built on ever-expanding debt.

Here’s what’s actually happening under the hood — and why it matters to your wealth.

The System Most People Never See

In earlier eras, paper currency was redeemable for something tangible. Today, the dollar is backed by government credit — and sustained by debt.

When the federal government spends more than it collects, it issues Treasury securities. Investors, institutions, and banks purchase them. The Federal Reserve can also buy Treasuries, creating new base money in the process. The banking system then expands credit on top of that base layer.

The result is straightforward: when money is created through expanding debt and credit, total currency supply tends to rise over time — and if supply grows faster than real output, purchasing power declines. That isn’t political. It’s supply and demand applied to money.

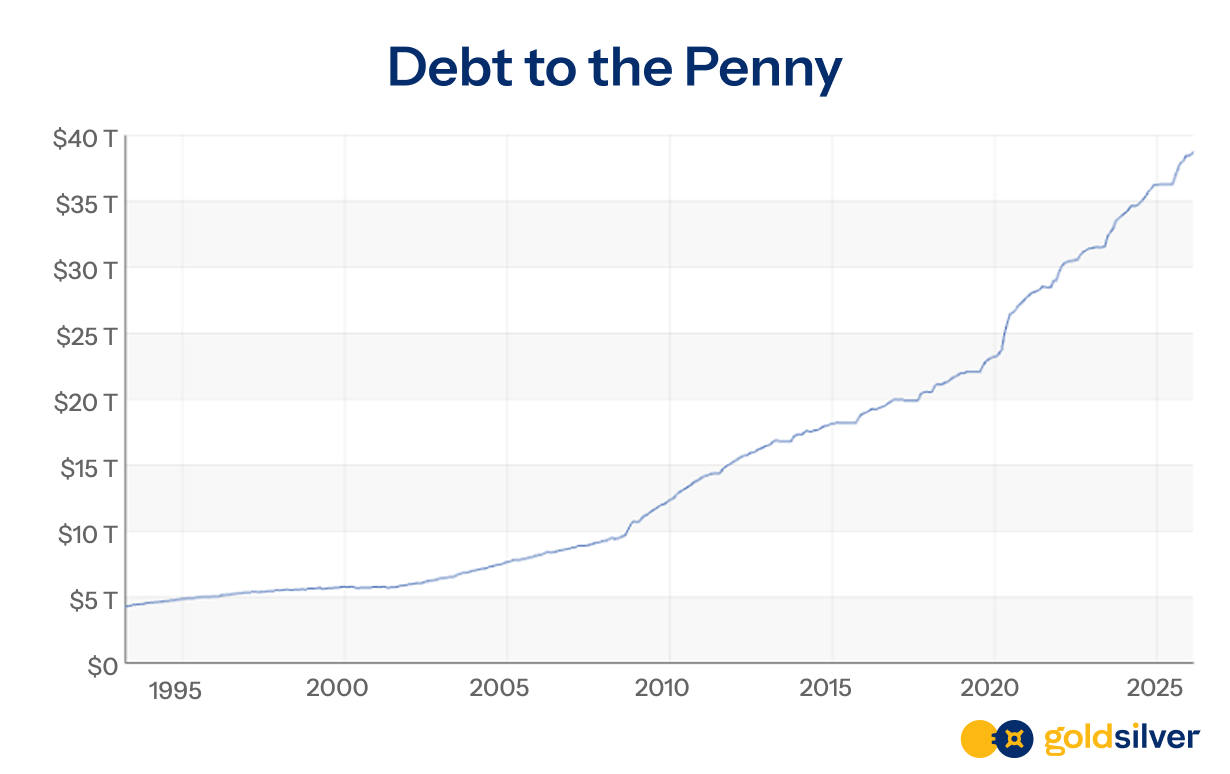

Chart #1: U.S. National Debt 1991–Present

Debt to the Penny, retrieved from https://fiscaldata.treasury.gov/datasets/debt-to-the-penny/, Feb 19, 2026

The trajectory of federal debt has been remarkably consistent. In the early 1970s, total U.S. debt was under $400 billion. Today it stands in the tens of trillions and continues to rise.

Regardless of political leadership, the modern financial system is structured around rolling and refinancing obligations. As existing debt matures, it is typically replaced with new issuance. Interest payments must be funded, which can require additional borrowing.

The structural incentives — not any particular administration or ideology — are what drive the long-term pattern of debt expansion.

For investors, the key point is that sustained debt expansion often coincides with sustained currency expansion. That relationship becomes clearer when examining the money supply directly.

The Financial System Isn’t Safer — And You Know It As risks mount, see why gold and silver are projected to keep shining in 2026 and beyond.

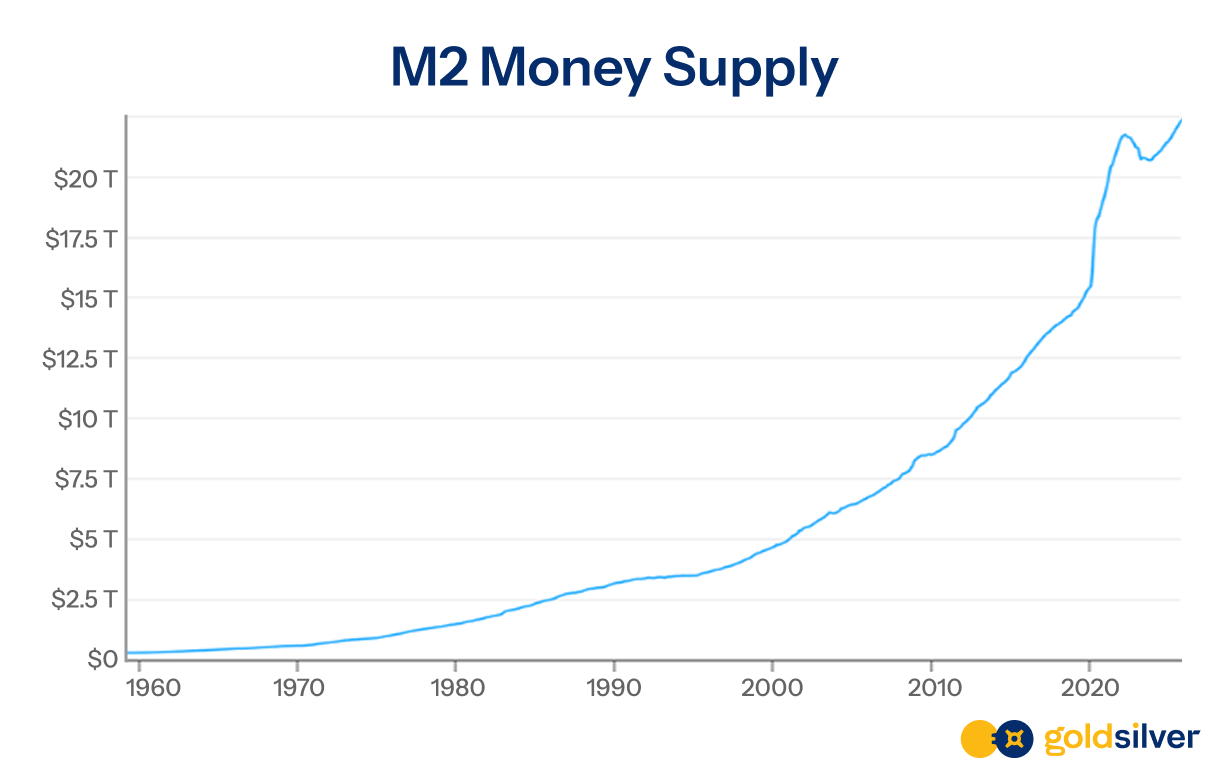

Chart #2: M2 Money Supply Growth (1959–Present)

Source: https://www.macrotrends.net/3005/m2-money-supply , Feb 23, 2026

M2 measures the money most households and businesses interact with: cash, checking deposits, and certain savings accounts. Over the past several decades, its trend has been upward, with notable accelerations during periods of financial stress.

After the 2008 financial crisis and again during the pandemic beginning in 2020, policymakers intervened aggressively to stabilize markets and support economic activity. These interventions included asset purchases, reduced interest rates, and expanded credit facilities — and as a result, trillions of additional dollars entered the financial system in relatively short periods.

Such actions are designed to mitigate instability. But when the supply of currency expands rapidly relative to productive output, each existing dollar represents a smaller claim on real goods and services.

The effects may appear first in asset prices and later in consumer prices, but the underlying dynamic is consistent over time.

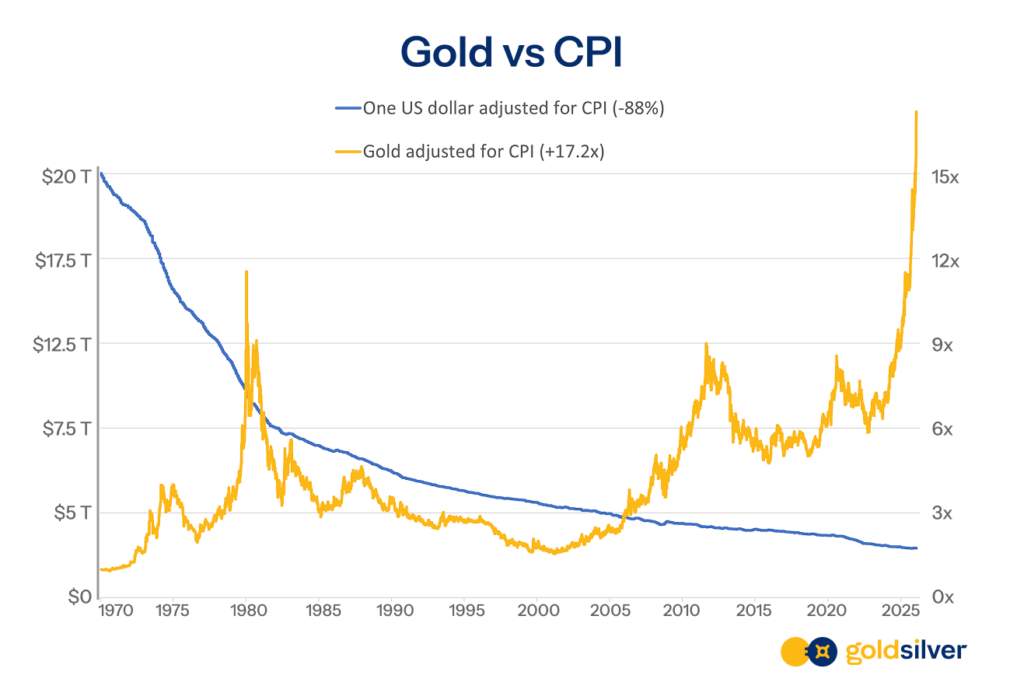

Chart 3: USD vs Gold Purchasing Power Since 1970

Source: Stockcharts.com, Goldsilver.com| *Data as of 1/27/2026

Inflation is often described as rising prices, but the more fundamental issue is the erosion of purchasing power. Over long periods, the dollar has lost a significant share of its ability to buy goods and services. A dollar today purchases substantially less than it did several decades ago.

The contrast with gold is instructive. Although gold prices fluctuate over shorter cycles, its purchasing power over longer historical periods has been more stable relative to fiat currencies. This is one reason central banks continue to hold gold as part of their reserves.

Cash held for liquidity serves an important purpose, but over extended time horizons it typically declines in real value. Financial assets tied to the credit system may grow during periods of expansion, yet they also reflect the same monetary conditions that influence currency supply.

Gold behaves differently. It isn’t created through debt issuance. It isn’t someone else’s liability. Its supply grows slowly and predictably. That difference is why serious investors treat gold not as a trade — but as monetary insurance.

These Charts Aren’t Predictions. They’re Records.

They describe how the system has operated for decades — across administrations, recessions, booms, and crises.

The practical question for investors isn’t whether this dynamic reverses tomorrow. It’s whether the structural incentives driving debt expansion and currency creation are likely to persist over the next 10 to 20 years.

History suggests they will.

Why This Matters Now

This isn’t just history. These reflect our current conditions.

Macro uncertainty, rising volatility across equities and bonds, and the persistence of inflation have prompted investors to rethink what “diversified” actually means. In that environment, capital tends to gravitate toward assets that behave differently from traditional financial instruments — assets that sit outside the credit system and respond to a different set of pressures.

Gold is frequently part of that discussion. Not because it moves up in a straight line or eliminates risk, but because it responds to a specific set of conditions — currency confidence, real interest rates, and systemic stress — that are increasingly relevant today.

Gold’s physical properties haven’t changed in thousands of years. The dollar’s structure has changed repeatedly, and its supply can expand quickly when policymakers choose. One is elemental. The other is engineered.

What Sophisticated Investors Do

Experienced investors don’t respond to this with panic. They respond with structure.

Think of a well-built portfolio as a set of tools, each with a different job: cash for liquidity, equities for long-term growth, bonds for income or stability depending on the environment. Precious metals — especially gold — fill a distinct role as monetary insurance: a non-correlated reserve asset designed to protect purchasing power and diversify risk when confidence is under pressure.

That’s a fundamentally different mindset from speculation. It’s not “all in on gold.” It’s “what percentage protects my base?” And the answer to that question is worth working out before uncertainty forces it.

Learn Before You Allocate

If this article raised questions, that’s a good sign. It means you’re thinking like a serious investor, not a headline-chaser.

Before you buy anything, the most important step is clarity: understanding how monetary systems function, how inflation transfers purchasing power, and how to size a metals allocation that makes sense alongside what you already own.

We created a premium education program designed for investors who want to build conviction before committing capital. It covers how sophisticated portfolios approach gold allocation, the difference between physical metals, IRA options, and storage, and how to integrate precious metals alongside equities in a way that makes sense for long-term wealth protection.

This isn’t a “buy now” pitch. It’s an education-first framework built to help you make decisions you can stand behind.

→ How Much Gold and Silver Should I Buy for My Portfolio?

In an uncertain world, the goal isn’t to guess right. It’s to be prepared.

Investing in Physical Metals Made Easy

People Also Ask:

Why is the U.S. dollar losing value over time?

The U.S. dollar tends to lose purchasing power over time because the money supply expands as government debt and credit grow. When more currency enters circulation faster than goods and services increase, each dollar represents a smaller claim on real value. Understanding this dynamic is central to how long-term investors think about preserving wealth.

How does national debt affect inflation and the dollar?

National debt itself doesn’t automatically cause inflation, but persistent debt expansion often coincides with currency expansion. When deficits are financed through borrowing and monetary policy, the total supply of dollars can increase over time, which may reduce purchasing power. This structural relationship is why many investors pay close attention to debt trends.

What happens to my savings if inflation continues?

If inflation persists, cash savings may lose real purchasing power even if the nominal balance remains the same. Over long periods, this erosion can materially impact retirement planning and wealth preservation. That’s why many investors diversify into assets designed to better withstand currency expansion.

Why do central banks hold gold instead of just cash?

Central banks hold gold because it is a reserve asset that is not tied to another country’s liability or credit system. Unlike fiat currency, gold cannot be created through debt issuance and has historically preserved purchasing power across long time horizons. Its role is stability, not speculation.

Does gold really protect against inflation?

Gold doesn’t eliminate short-term volatility, but historically it has tended to retain purchasing power over extended inflationary periods. Its supply grows slowly and predictably, which contrasts with fiat currencies that can expand rapidly during crises. Many investors view gold as monetary insurance within a diversified portfolio.

You May Also Like

- What Are Margin Requirements? Why CME’s Hike Triggered a Silver Crash

- Why Margin Hikes Could Make Gold and Silver Prices More Volatile

- Silver Price Forecasts Revisited: Why Wall Street Got It Wrong

- Why Metals Dominated Every Asset Class in 2025 [and What It Means for 2026]

- Best Investment Of 2026: Silver’s Setup Is Hard To Ignore