Published: 04-27-2026, 05:16 pm

Gold and silver market update — April 27, 2026

Key Takeaways

- The rate decision tomorrow is priced in at 99.5% hold — what moves gold is Powell’s language, specifically whether he ties any future cuts to Hormuz or oil conditions.

- Iran submitted a new Hormuz ceasefire proposal on April 27; a credible deal announced alongside Powell’s press conference would compound into gold’s strongest near-term catalyst.

- The structural case for gold and silver — $1 trillion in annual US debt service, 863 tonnes of central bank buying in 2025, and six months of COMEX silver stress — does not change regardless of what Powell says.

The Fed opens its two-day meeting today. Jerome Powell chairs his last FOMC session as Federal Reserve chair. Tomorrow’s rate decision isn’t the story — the CME FedWatch tool puts a 99.5% probability on a hold at 3.50–3.75%, so no one is waiting on that. What matters is the language Powell uses at his 2:30 PM ET press conference on April 29. One sentence could move gold 2–3% within the hour.

Here is what that sentence looks like, why the Iran situation makes the timing unusual, and what each scenario means for your metals position.

Where Are Gold and Silver Prices Today?

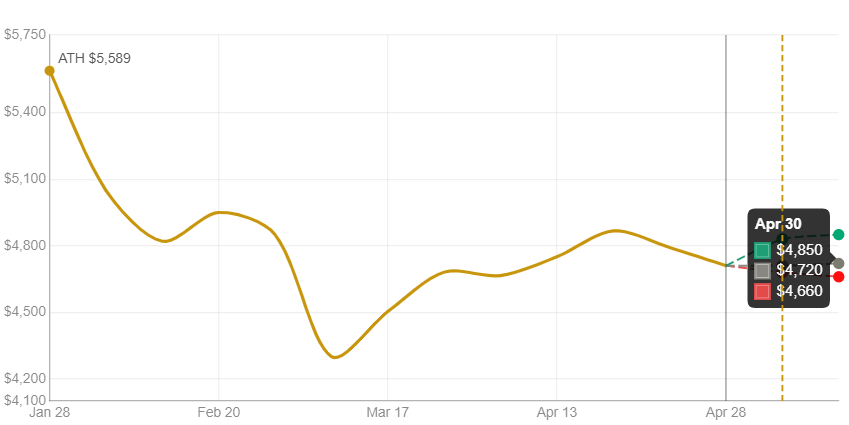

Gold opened this week at $4,700–$4,720 per ounce — 16% below its January 28 all-time high of $5,589, but still up 42% year-over-year. Silver is at $75–$76, down sharply from its January record of $121.64. Meanwhile, the gold-silver ratio sits at 62:1, below its long-run average of 70:1 — silver sharply outperformed gold over the past year, even after the correction.

Both metals are stuck. The US-Iran war that started on February 28 sent oil surging, pushing March CPI to 3.3% year-over-year — up from 2.4% in February. That inflation gives the Fed reason to hold rates, which puts a ceiling on gold. With Brent crude still elevated, that ceiling has not shifted.

The Edge Every Investor Needs Smarter precious metals investing starts here. The Nuggets Newsletter brings you essential market insights, Fed updates, global trends, educational videos, and much more.

What Does Powell Need to Say to Move Gold?

Tomorrow’s press conference is a non-SEP meeting — no dot plot, no updated projections. As a result, every forward signal has to come from statement language and Powell’s answers.

The sentence gold markets need sounds roughly like this: “Should energy prices moderate and Strait of Hormuz conditions improve, the committee sees a path back to easing in 2026.”

That conditional does something specific. It tells the market the rate ceiling on precious metals is not structural — it’s geopolitical. Geopolitical problems get solved. Structural ones don’t. A ceiling tied to the Strait of Hormuz is, therefore, a ceiling with an expiration date. Gold would likely rally 2–3% on language like that alone.

The worst outcome isn’t a hike. Instead, it’s a hold statement with no conditions — language implying the Fed will sit tight regardless of oil or the Strait. That keeps the ceiling in place and would likely push gold back below $4,700 by Thursday’s close.

Does the Iran Hormuz Proposal Change the Situation?

On Monday, April 27, Iran submitted a new ceasefire proposal via Pakistani mediators. The terms: extend the ceasefire, defer nuclear negotiations, and reopen the Strait of Hormuz — in exchange for the US lifting its naval blockade of Iranian ports. Brent crude pulled back modestly on the news, and silver briefly recovered above $76 before settling flat.

The timing matters for a specific reason. If any credible Hormuz deal is announced before or alongside Powell’s press conference tomorrow, the two events compound each other. Lower oil directly reduces CPI. That, in turn, opens the door to rate cuts, which compress real yields — and compressed real yields are gold’s strongest tailwind.

Natixis analyst Bernard Dahdah estimates the war has suppressed gold by up to $750 per ounce through the inflation-and-rate-hold mechanism. That gap won’t close in a single day. However, a reopening announcement is the trigger that starts closing it.

What Does Powell’s Exit Mean for Gold Under Warsh?

Powell is the 16th Federal Reserve chair. Starting February 5, 2018, he took over from Janet Yellen, inheriting a $4.5 trillion balance sheet and near-zero inflation. In contrast, he now leaves behind a $6.7 trillion balance sheet, the worst inflation reading since 1981, three regional bank failures in 2023, and an active oil war. His term expires May 15.

Warsh’s path to the chair cleared sharply on Friday, April 24, when the DOJ dropped its criminal probe into Powell over alleged Fed headquarters renovation cost overruns. Subsequently, Polymarket odds on Warsh being confirmed by May 15 jumped from 27% to 84% in a single session (Benzinga, April 24, 2026). Kalshi placed the probability even higher, at 86%.

Gold rose on April 25. That surprised many traders who expected the opposite. The logic: markets had been pricing in a risk — that the next chair would operate under political pressure. When the DOJ decision resolved that uncertainty, gold went up not on rate expectations but on institutional credibility. That distinction matters going forward. Specifically, it means gold’s structural bid doesn’t depend on Warsh being dovish. It depends on the Fed remaining credible — which, for now, markets believe it will.

Tomorrow is Powell’s farewell press conference. One question matters above all others: does he signal the March dot plot’s single 2026 cut is still alive, or has deteriorating growth data quietly closed that door?

Why Is Silver’s Setup Different from Gold’s Right Now?

Silver enters this week carrying a structural dynamic that gold doesn’t have.

The COMEX May 2026 silver contract still has 26,963 open contracts — representing 134.8 million ounces — ahead of First Notice Day on Thursday, April 30. Moreover, the coverage ratio (registered, deliverable inventory against open interest) has been below the 15% stress threshold for six consecutive months. That physical delivery pressure acts as a structural floor under silver, independent of anything Powell says tomorrow.

The complication is silver’s industrial half. A stagflation signal — inflation up, growth down — could weigh on silver’s industrial demand even as the monetary bid holds. Silver is, in effect, two metals at once, and this week tests both identities simultaneously.

On the physical demand side, however, the picture is less ambiguous. China’s silver imports in March 2026 ran 173% above the 10-year seasonal average (Kitco, April 23, 2026). Two distinct buyer groups drove it at the same time: retail investors priced out of gold, and solar manufacturers front-running a policy deadline. Demand of that magnitude doesn’t reverse on a single Fed press conference.

What Are the Three Scenarios for Gold and Silver?

Scenario 1 — Powell signals a conditional easing path Gold moves toward $4,800–$4,850. Silver follows, and the gold-silver ratio tightens toward 60:1. This is the week’s clearest bullish trigger. To materialise, it requires Powell to explicitly link Hormuz or oil conditions to the rate-cut timeline.

Scenario 2 — Hold with neutral language Both metals trade sideways. Markets already priced the hold, so attention shifts to Thursday’s Q1 GDP print on April 30. The Atlanta Fed’s GDPNow model is tracking Q1 2026 growth at 1.24%, down from 3.1% in late February. Consequently, a print near that level alongside CPI at 3.3% would formally confirm stagflation — and likely push gold higher on safe-haven demand, even as it weighs on silver’s industrial bid.

Scenario 3 — Hawkish hold, no conditions Gold breaks below $4,700. Silver tests $74. The ceiling holds. This is the near-term bear case — though it also sets up a sharp rebound once Hormuz shifts and the rate-cut window opens.

Does the Structural Case for Gold Still Hold?

Yes — and it holds regardless of which scenario plays out.

Four things remain unchanged after Powell’s press conference:

- US annual debt service has crossed $1 trillion for the first time — rivaling the entire defense budget (CBO, FY2026)

- The US fiscal deficit is projected at $1.9 trillion for FY2026

- Central banks bought 863 tonnes of gold in 2025 and have continued buying in 2026, across more countries than any prior year (World Gold Council)

- COMEX silver has been in coverage-ratio stress for six consecutive months, with a sixth consecutive annual supply deficit projected for 2026 (Silver Institute)

Gold ran from $2,600 to $5,589 in fourteen months. The forces behind that run — debt, central bank buying, fiat erosion — aren’t resolved by a press conference. Nor are they resolved by a chair transition.

The ceiling on gold right now is oil. Oil depends on the Strait. The Strait is a negotiating table, not a permanent wall. When that ceiling lifts, the move will be fast. Powell’s language tomorrow tells us how close we are.

Stay On Top of Gold & Silver Prices

Get important market alerts sent straight to your inbox.

SOURCES

1. CME Group — FedWatch Tool: FOMC Rate Probability, April 28–29 2026

2. Federal Reserve Bank of Atlanta — GDPNow Q1 2026 Estimate, April 21 2026

3. Bloomberg — China’s Silver Imports Jump to Record on Retail and Solar Demand, April 21 2026

4. Benzinga — DOJ Drops Powell Probe: Betting Markets Say Warsh Is Fed Chair by May 15, April 24 2026

5. World Gold Council — Gold Demand Trends: Full Year 2025, January 2026

6. Silver Institute / Metals Focus — World Silver Survey 2026: Sixth Consecutive Annual Deficit, April 15 2026

7. Congressional Budget Office — The Budget and Economic Outlook: 2026 to 2036, February 2026

8. Natixis / Bernard Dahdah — Gold Price War Suppression Estimate of $750/oz, via Bloomberg, March 11 2026

By the GoldSilver Editorial Team — helping investors understand sound money since 2005. This article is for informational purposes only and does not constitute financial, investment, or tax advice. Always consult a qualified financial advisor before making investment decisions.

You May Also Like:

- Iran Blinked — And One Word From Powell Decides What Happens Next

- COMEX Silver First Notice Day April 30: What to Watch

- What Warsh as Fed Chair Means for the Gold Price

- 5 Signals the Mainstream Gold & Silver Narrative Missed

- Before the Fed Speaks, Watch This Number for Gold

- Gold Price Today: What to Watch Before the April 29 FOMC

- What’s Driving Gold Prices? Oil, PMI, and Newmont

- Dollar Weakens, Gold Falls — and That’s Actually Bullish