Daily News Nuggets | Today’s top stories for gold and silver investors

February 25th, 2026 | Brandon Sauerwein, Editor

Trump Shrugs Off Affordability Fears in State of the Union

President Trump used his State of the Union address to double down on his economic agenda — largely brushing aside persistent voter concerns about affordability. He touted strong job growth and rising investment. But he offered few specifics on housing costs, insurance premiums, or the everyday expenses still squeezing middle-class households.

Markets are paying attention. Consumer sentiment has been fragile for months, and affordability remains a top political and economic flashpoint heading into the second half of the year.

The math is straightforward: when voters feel squeezed, spending slows. That ripples into corporate earnings, growth expectations, and eventually Fed policy. It’s the kind of slow-burn risk markets tend to underestimate — right up until they can’t.

Nowhere is that pressure more visible than in the U.S. housing affordability crisis.

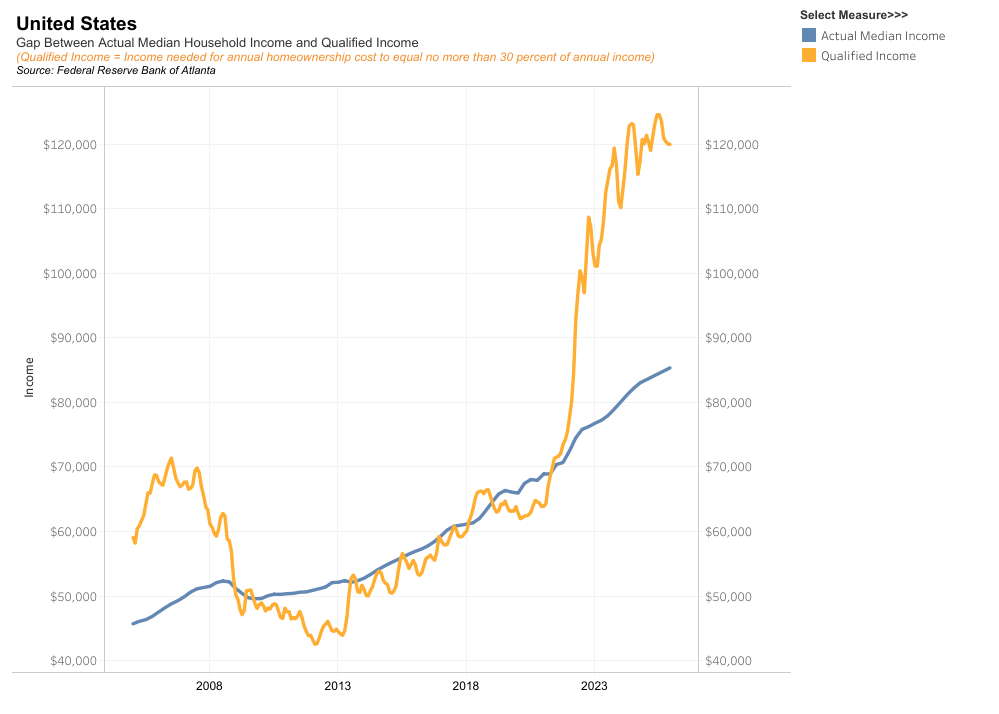

The Housing Affordability Crisis in One Chart

Despite headline economic growth, the housing market tells a different story. According to Federal Reserve data, prospective buyers now need to earn 43% more than the average U.S. household just to afford a typical home.

Actual Median Household Income and Qualified Income

The chart above shows why. “Qualified income” is what a household must earn to keep homeownership costs — mortgage, taxes, and insurance — below 30% of annual income. That’s the long-standing affordability benchmark. Since 2020, the required income has surged. Actual median income has barely kept pace.

The housing affordability crisis remains wide and unresolved. Mortgage rates have eased recently, but home prices remain elevated. Borrowing costs are still well above pre-pandemic levels. For most households, the numbers simply don’t add up.

Housing is the single largest expense for most families. When the gap between wages and what ownership actually costs stretches this far, no jobs report or GDP print changes how people feel at the kitchen table.

There is one small bright spot — at least for now.

Stay Ahead with Gold & Silver News The most important market insights, Fed updates, and global trends — everything investors need to make smarter, safer decisions.

When Lower Rates Raise Bigger Questions

U.S. mortgage rates have fallen to their lowest level in months — a small but welcome sign for a housing market that’s been stuck in neutral. The average 30-year mortgage dropped 8 basis points to 6.09% for the week ended Feb. 20, according to Mortgage Bankers Association data. Five-year adjustable rates fell to 5.23%, the lowest since September 2022.

The move tracks a pullback in Treasury yields, as investors increasingly price in Fed rate cuts later this year. Lower borrowing costs could help thaw buyer demand heading into spring. But affordability is still stretched. Home prices remain elevated and inventory is tight — rate relief alone won’t fix that.

There’s a bigger signal here too. When rates fall because growth is slowing, that’s not the same as rates falling because inflation is beaten. The market may be telling us something. That’s the kind of environment where capital starts looking for cover.

And while households weigh every percentage point, markets are reacting to a much broader set of risks.

Recession Warning Signal Flashes for 13th Straight Month

Americans are feeling slightly better about the economy — but not by much. The Conference Board’s consumer confidence index nudged up to 91.2 in February, bouncing back after a sharp drop in January.

The headline number isn’t the story. The expectations index — which tracks short-term outlook for income, jobs, and business conditions — has now come in below 80 for 13 consecutive months. That threshold has historically signaled recession risk. It hasn’t been this persistently low since the early 2000s.

What’s driving the gloom? Prices. Write-in responses from survey participants pointed overwhelmingly to inflation and the cost of goods as their top concerns. Spending intentions for 2026 are tilted toward necessities and “cheap thrills” — and away from big discretionary purchases.

The headline ticked up. The worry didn’t.

While Nobody Was Watching, Silver Climbed 25%

While the headlines have been consumed by tariffs and political noise, silver prices have been making a quiet and remarkable run. Since dropping to around $70/oz on February 5th, silver is up over 25% — back above $90/oz as of Wednesday morning. Gold is up too, gaining 0.90% to $5,188, but silver is the standout.

Investing in Physical Metals Made Easy

With markets already on edge over slowing global growth and sticky inflation, any escalation in trade tensions is enough to revive safe-haven demand. While equities wavered and bond yields fluctuated, precious metals found support from a softer dollar and renewed geopolitical concerns.

Traders are also recalibrating expectations for Federal Reserve rate cuts. When policy uncertainty rises, defensive assets tend to catch a bid — and that’s exactly what we’re seeing.