Published: 03-19-2026, 12:35 pm | Updated: 03-19-2026, 12:33 pm

Gold vs Stocks & Bonds — The Quick Answer

- Stocks: Growth, but vulnerable to sharp drawdowns

- Bonds: Income, but losing diversification power

- Gold: Stability, crisis protection, and true diversification

Most portfolios rest on a simple assumption: stocks grow, bonds protect. For decades, that held. But the data tells a more complicated story now.

The classic 60/40 portfolio has a blind spot. When stocks and bonds sell off together — as they did in 2022 — there’s nothing left to cushion the fall. That’s the gap gold fills, and it’s not a small one.

This guide breaks down the case for gold vs stocks and bonds — not to replace them, but to show what gold does that neither asset can replicate.

This isn’t about abandoning equities or fixed income. It’s about what gold actually does that neither asset can replicate — and what the historical record shows when you look at the numbers honestly.

Gold vs Stocks and Bonds — What the Data Shows

The classic 60/40 portfolio rests on one core idea: when stocks fall, bonds rise. That negative correlation was the engine of diversification for decades. That engine is stalling.

The World Gold Council’s February 2026 cross-asset analysis found a decisive shift: stocks and bonds are increasingly moving together, not in opposite directions. The 2022 inflation shock made this impossible to ignore. Stocks fell sharply. Bonds fell too. It was one of the worst years for a 60/40 portfolio in modern history — not because of bad luck, but because the underlying logic had broken down.

The problem isn’t temporary. With US core PCE inflation still sticky near 3%, the Fed has limited room to cut rates. Rate cuts are the usual mechanism that sends bond prices higher during stock downturns. Without that lever, bonds lose their defensive function precisely when investors need it most.

That’s the gap gold fills — and the numbers make the case plainly.

Gold Has Outperformed

Every Major Asset Class

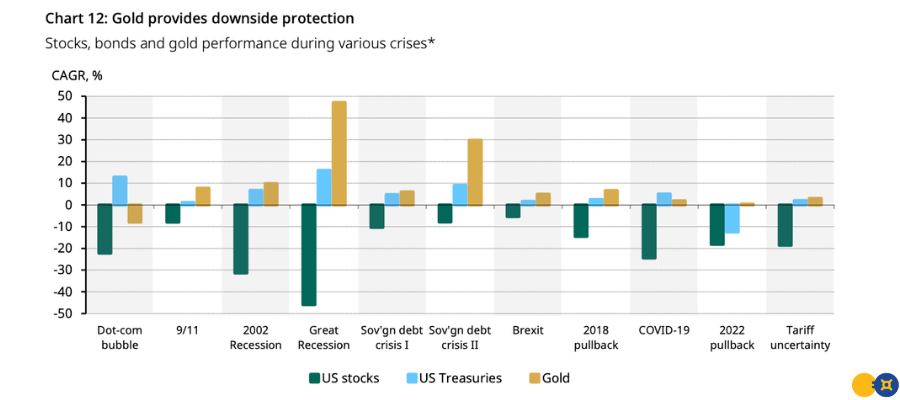

Does Gold Actually Protect You When Markets Crash?

Gold and stocks serve fundamentally different purposes — and the data reflects that clearly.

Over the 2014–2023 decade, gold delivered positive annual returns in seven of ten years. More importantly, its strongest years aligned with periods of stock market stress. In 2020, gold rose more than 25% while global markets reeled from pandemic uncertainty. During the 2008 financial crisis, gold posted positive returns as the S&P 500 fell nearly 40%.

The World Gold Council’s crisis performance data drives this home. Across eleven major shocks — from the dot-com bust and 9/11 to COVID-19 and the 2025 tariff selloff — gold consistently gained or meaningfully cushioned losses when equities were deeply negative.

Source: World Gold Council, Why Gold 2026: Cross-Asset Perspective

Gold’s job isn’t to beat stocks in a bull market. It’s to behave differently when everything else is falling. That’s where its portfolio value comes from.

Stocks respond to earnings, economic growth, and investor sentiment. Gold responds to inflation expectations, real interest rates, and demand for safety. These are different engines running on different fuel — which is exactly why combining them makes a portfolio more resilient.

Are Bonds Still a Better Safe Haven Than Gold?

For decades, long-duration US Treasuries were the go-to hedge against stock market downturns. When equities fell, investors fled to bonds. Yields dropped, prices rose, and portfolios stayed afloat. That relationship is breaking down.

When inflation rises and the Fed tightens, stocks and bonds fall together. Gold doesn’t follow that script. As the World Gold Council notes, rising stock-bond correlation has made Treasuries significantly less effective as a portfolio hedge than they once were.

2022 proved this in real time. Treasuries fell sharply alongside stocks as the Fed hiked rates aggressively. Gold finished the year at -0.3% — a return that looked almost heroic by comparison. It preserved capital when the traditional diversifier failed.

The math also favors gold in today’s environment. Gold tends to perform well when real interest rates — nominal rates minus inflation — are low or negative. The opportunity cost of holding a non-yielding asset shrinks. With inflation risks still elevated and bond yields struggling to keep pace, that’s exactly the environment we’re in.

The Financial System Isn’t Safer — And You Know It As risks mount, see why gold and silver are projected to keep shining in 2026 and beyond.

Does Gold Actually Hedge Against Inflation?

The short answer: yes — but not in the way most people expect.

Over centuries, gold has preserved purchasing power in ways fiat currencies have not. Print enough money, and each dollar buys less. Gold doesn’t work that way. Its supply grows slowly and can’t be conjured by a central bank.

Over shorter time horizons, the relationship is more layered. Gold doesn’t track CPI month-to-month. It responds to expectations — specifically, what households and markets believe about future inflation and whether central banks can contain it. When confidence in monetary policy wavers, gold tends to move.

That’s what makes the current moment notable. The World Gold Council’s 2026 report finds that US household inflation expectations have risen meaningfully — even as policymakers project confidence. That gap matters. When the public stops believing official reassurances, gold historically benefits. Right now, that gap is wide.

Why Do Most Investors Own So Little Gold?

The data on gold is not hidden. The research is abundant, publicly available, and increasingly hard to dismiss. So why do most portfolios still hold little to none of it?

The answer isn’t information. It’s behavior.

Recency bias is the biggest factor. Equities have delivered strong returns for much of the past decade. When one asset dominates long enough, it starts to feel like the only rational choice — and everything else starts to look like a distraction.

Income bias compounds the problem. Gold doesn’t pay a dividend or coupon, so many investors dismiss it outright. But that framing misses the point. Gold’s value isn’t income — it’s what happens to your portfolio when income-generating assets are in freefall.

Institutional inertia does the rest. The 60/40 portfolio has been the default framework for decades. Advisors, models, and retirement strategies are still built around it — even as its core assumption, that bonds offset stock losses, continues to erode.

The result is a portfolio optimized for a world that may no longer exist: falling rates, low inflation, and reliable bond protection. Gold has historically delivered its greatest value in exactly the environment investors now face. Most portfolios aren’t positioned for it.

What Percentage of a Portfolio Should Be Gold?

Most investors ask this eventually. The data gives a clearer answer than you might expect.

The World Gold Council’s research points to an optimal gold allocation of between 5–8% of a portfolio. At these levels, gold has historically improved risk-adjusted returns — reducing drawdowns without meaningfully sacrificing long-run gains.

That range holds across different investor profiles. A conservative, capital-preservation-focused investor may lean toward the higher end, using physical gold or gold ETFs as a buffer. A growth-oriented investor can still benefit: even a 5% allocation has historically improved the Sharpe ratio of an equity-heavy portfolio.

The more striking finding isn’t the optimal range — it’s how far most portfolios fall short of it. Despite years of strong price appreciation, gold’s share of global private investment portfolios remains near historical lows. Most investors are significantly underweight in an asset that the data consistently supports holding.

That’s not a minor oversight. It’s a structural gap with real consequences for portfolio resilience.

Is the Stock Market Overdue for a Correction — And What Happens to Gold If It Does?

The conditions that have historically preceded major market dislocations are present right now.

US equity valuations are approaching dot-com era levels by forward P/E metrics. Margin debt — the amount investors borrow to buy stocks — surged in late 2025 to levels that have preceded equity bear markets before. Credit spreads on corporate and high-yield bonds remain compressed near historical lows. Markets are pricing in remarkably little risk.

That’s a problem. Compressed spreads don’t eliminate risk — they just delay and concentrate it. When sentiment shifts, the repricing can be fast and severe.

The World Gold Council’s 2026 analysis flags this directly, describing the current environment as one of stretched valuations and persistent macro risks — a combination that has historically driven safe-haven demand sharply higher.

Gold isn’t a speculative bet on a crash. It’s a hedge against the risks already embedded in today’s market pricing — risks that most portfolios aren’t built to absorb.

So, Should You Add Gold to Your Portfolio?

The data makes a clear case — not against stocks or bonds, but for completing the picture.

Gold has preserved capital during crises. It has hedged inflation across decades. It provides diversification that bonds are increasingly unable to deliver. No other mainstream asset does all three.

The 60/40 portfolio isn’t dead. But relying on it alone — in an environment of rising stock-bond correlation, sticky inflation, and stretched valuations — is a different kind of risk than most investors account for.

Gold’s role in a portfolio isn’t a historical curiosity. In today’s environment, it’s a structural necessity.

Stay On Top of Gold & Silver Prices

Get important market alerts sent straight to your inbox.

People Also Ask

Does gold outperform stocks over the long term?

Not consistently—but that’s not gold’s job. Gold outperforms stocks during periods of crisis, high inflation, and market stress. Over the 2014–2023 decade, gold delivered positive returns in seven out of ten years, with its strongest gains occurring precisely when equities were under pressure. Its value lies in diversification and downside protection, not in beating the S&P 500 in bull markets.

Why is gold considered a hedge against inflation?

Gold has maintained purchasing power over centuries in ways fiat currencies have not. Unlike paper money, gold cannot be printed or devalued through monetary policy. When inflation expectations rise and real interest rates fall, gold typically appreciates—making it a structural buffer against the erosion of wealth that inflation causes.

What is the correlation between gold and stocks?

Gold has a low to negative correlation with equities, meaning it tends to move independently—or in the opposite direction—from stock markets. This is the core reason gold improves portfolio diversification. During major equity drawdowns like the 2008 Global Financial Crisis and the 2020 pandemic selloff, gold posted positive returns while stocks fell sharply.

How does gold compare to bonds as a portfolio hedge?

Historically, bonds hedged equity risk by rising when stocks fell. That relationship has weakened significantly as stock-bond correlation has increased. In 2022, both stocks and bonds fell simultaneously during the inflation shock. Gold finished that year nearly flat, demonstrating that it can provide the defensive role bonds no longer reliably deliver—especially in high-inflation environments.

How much gold should I have in my portfolio?

Research from the World Gold Council suggests an optimal gold allocation of roughly 5%–8% for most investors, depending on risk tolerance. Even a modest 5% allocation has historically improved risk-adjusted returns by reducing portfolio drawdowns without meaningfully sacrificing long-run gains. Most investors currently hold far less gold than this optimal range.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Always consult a qualified financial advisor before making investment decisions. Past performance is not indicative of future results.

You May Also Like: