Published: 06-08-2026, 03:23 pm | Updated: 06-08-2026, 05:14 pm

Key Takeaways

- Every bank deposit is an unsecured loan to the bank. Allocated physical gold is not. The two carry completely different risk profiles.

- In February 2022, Western governments froze approximately $300 billion in Russian central bank foreign currency reserves. Non-Western central banks drew a clear lesson: reserve currencies carry political risk as well as inflation risk.

- World Gold Council data shows central bank gold purchases reached multi-decade highs in 2022, 2023, and 2024 — led by non-Western buyers systematically reducing dollar-denominated reserves.

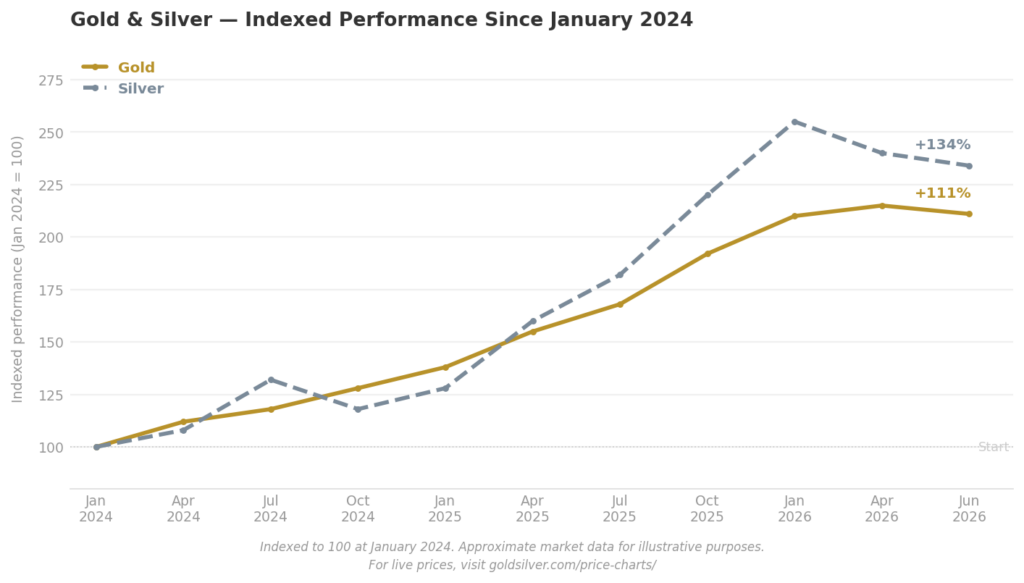

- Gold has roughly doubled from its early 2024 lows. Silver has gained more than 130% over the same period. For live prices, see goldsilver.com/price-charts/.

- GoldSilver’s InstaVault lets investors hold institutional-grade allocated storage and home-held physical metal through a single account — with no minimums and full delivery flexibility.

Does Physical Gold Have Counterparty Risk?

Most investors know what diversification means. Spread your money across different assets so one bad day doesn’t wipe you out. Smart. But there’s a second kind of diversification almost nobody talks about — and it’s just as important.

It’s not what you own. It’s where you keep it and who’s responsible for it.

When it comes to gold and silver, that question has a clear answer. Does physical gold have counterparty risk? No. And once you understand why, you’ll never think about your savings the same way.

What Is Counterparty Risk? Here’s a Story

Imagine you hand your neighbor $10,000 to hold onto. He gives you a note saying he owes you $10,000. Now imagine he loses his job, runs up debts, and can’t pay you back. You don’t have $10,000. You have a note from someone who can’t honor it.

That’s counterparty risk. The other party in your financial arrangement fails to meet their obligation.

Now here’s the part most people don’t realize: that’s exactly what a bank deposit is.

When you deposit money at a bank, you are not storing it. You are lending it. The bank takes your money, uses it, and owes it back to you. Your savings account is a line on the bank’s balance sheet. It’s a liability they owe you. Not your property sitting untouched in a vault.

The Federal Deposit Insurance Corporation (FDIC) covers up to $250,000 per depositor per institution if a bank fails. That protection matters. But it covers individual bank failures — not simultaneous problems across multiple major institutions at once. And it covers a dollar amount, not the purchasing power of that amount.

Physical gold? Different story entirely.

The Knowledge That Changes Everything

Two essential guides — yours free. Understand why gold matters and why fiat currencies always fail.

Does Physical Gold Have Counterparty Risk? The Definitive Answer

The Bank for International Settlements defines counterparty risk simply: one party in a contract fails to deliver. Physical gold isn’t a contract. It is not a claim. Nobody owes it to you — you simply own it.

Allocated gold held in a vault is not on anyone’s balance sheet. No institution can freeze it. A central bank decision cannot dilute it. And if a bank fails, it doesn’t disappear.

Your bank runs business hours. Gold trades 24 hours a day, 365 days a year. Your bank account can be restricted, frozen, or capped on wire transfers. Your gold can’t.

This is why gold has worked as money for thousands of years across dozens of collapsed monetary systems. The systems come and go. The metal remains.

The mechanism is simple. With physical gold, there is no counterparty. With a bank deposit, there are many.

Why Central Banks Made the Same Calculation in 2022

This isn’t just theory for individual investors. In February 2022, Western governments froze approximately $300 billion in Russian central bank foreign currency reserves. The assets were in Western institutions, denominated in Western currencies. They were gone in a weekend.

Every non-Western central bank watching drew the same conclusion. Currencies held in someone else’s system carry political risk on top of inflation risk. The only reserve asset that doesn’t is gold.

According to World Gold Council data, central bank gold purchases hit multi-decade highs in 2022, 2023, and 2024. China, India, central banks across the Middle East — all systematically increasing gold and reducing dollar exposure. These were not trades. They were permanent structural shifts.

Individual investors face a smaller version of the same question. Your savings held in a bank are subject to the bank’s health, the government’s policies, and the dollar’s purchasing power. Your gold is subject to none of those things.

How to Think About Gold vs. Silver

Gold and silver are not the same asset, and they don’t need to play the same role.

Gold is the anchor. It holds purchasing power over long periods. It moves less violently and is the right choice when stability matters most.

Silver moves faster. It tends to lag gold during calm markets. During dislocations — when industrial demand slows and monetary demand surges — silver often outperforms. Silver has gained more than 130% from its 2024 lows. Gold has roughly doubled over the same period. For live prices, see goldsilver.com/price-charts/.

The gold-silver ratio is one signal experienced investors watch for allocation shifts. It fluctuates with market conditions. It works best alongside real yield trends and central bank data — not as a standalone trigger.

Price corrections happen within any long-term bull market. The underlying drivers remain intact. Monetary expansion. Shrinking real returns on savings. Central banks moving steadily out of paper and into metal.

GoldSilver Vault Storage: Not a Deposit. Every Ounce Is There.

Here’s the critical difference between a bank and a vault storage program: GoldSilver storage is not a deposit. Your metal is not lent out. It is not used as collateral. It does not appear on anyone’s balance sheet as a liability. Every ounce you own is physically sitting in a vault, allocated in your name.

That matters because of what happens to insurance. FDIC protection covers up to $250,000 — a dollar cap on a bank’s debt to you. GoldSilver vault storage carries full market replacement value insurance. If gold is at $5,000 an ounce when something goes wrong, that’s what you’re covered for. Not a fixed dollar ceiling.

Vaults are operated by Brinks, Loomis, and Malca-Amit in six locations: Salt Lake City, Dallas, Toronto, Singapore, and Hong Kong. Every position is independently audited by third parties. Class 3 security under Underwriters Laboratories standard UL 608 — the highest burglary-resistance classification available. Armed guards. 24/7 surveillance. No hidden fees.

Storage runs at 0.06% per month — $6 a month on $10,000 of metal. No minimum. No long-term commitment. Start, stop, or take delivery whenever you choose.

If you want to understand the full breakdown of allocated vs. segregated storage options, this guide covers the difference in detail.

Getting Started Is Easier Than You Think

Most people assume institutional-grade storage is for large accounts. It isn’t.

GoldSilver’s InstaVault lets you start with no minimum. You get fractional ownership of institutional-weight bars — 400-oz gold bars and 1,000-oz silver bars — sitting in third-party vaults. Storage fees come off your card, never your metal. You can convert to physical delivery at any time.

For investors who want whole bars or coins, that’s available too. GoldSilver supports personal accounts, joint accounts, trusts, corporate accounts, and tax-advantaged IRAs. If you have metals in an existing IRA, in-kind transfers to a GoldSilver account are available through their preferred custodian. Offshore vault locations — Singapore and Hong Kong — give internationally-minded investors jurisdiction options most platforms don’t offer.

Everything runs through one account. Home-held metal and vaulted metal sit side by side in the same dashboard. There’s no second platform, no separate vendor, and no choosing between approaches. You can hold some at home and store the rest — and see both in one place.

For a full comparison of home storage vs. vault storage risks, this article lays out how the two strategies work together.

The Question Nobody Asks Until It’s Too Late

Most investors spend hours deciding how much gold and silver to own. Most spend almost no time deciding where to keep it.

Home storage means zero counterparty risk. Nothing between you and your metal. The tradeoff is that security and insurance become your problem. Standard homeowners’ policies typically cap bullion coverage at $200 to $250 per claim — almost nothing for a serious position.

Vault storage adds professional security, third-party auditing, and full replacement insurance. The tradeoff is a small layer of institutional reliance.

The answer isn’t one or the other. The answer is both. Some metal at home for true independence. Some in a vault for liquidity, insurance, and ease of accumulation. GoldSilver is one of the few platforms built to handle both in one place. Here’s how that works in practice.

Where to Start

One question cuts through it. What does each portion of your metals need to do?

If it’s your backstop — the metal you’d reach for if the system locked up — keep it at home. Accessible to no one but you.

If it’s the portion you want insured and easy to build, put it in an allocated vault. One that lets you take delivery whenever you choose.

Neither approach is complete on its own. Together, they cover what the other can’t. That’s not a doomsday strategy. That’s sound money thinking applied to where you actually live.

Start with GoldSilver’s vault storage program here.

Stay On Top of Gold & Silver Prices

Get important market alerts sent straight to your inbox.

People Also Ask

Does physical gold have counterparty risk?

No. Allocated physical gold held in institutional storage carries zero counterparty risk. It is not a claim on any institution, does not sit on any bank’s balance sheet, and cannot be frozen, diluted, or devalued by a central bank’s policy decision. It belongs to you entirely, independent of any intermediary.

What is the difference between a bank deposit and physical gold?

A bank deposit is an unsecured loan to the bank. The institution owes you the money and can restrict access during stress events. Physical gold is property you own outright. It carries no default risk, no institutional dependency, and no exposure to bank solvency or government policy.

Why are central banks buying gold instead of holding dollars?

In February 2022, Western governments froze approximately $300 billion in Russian central bank foreign currency reserves. The lesson was clear: reserve currencies carry political risk, not just inflation risk. Gold held domestically cannot be frozen by a foreign government. World Gold Council data shows central bank gold purchases reached multi-decade highs in 2022, 2023, and 2024.

Is it safer to store gold at home or in a professional vault?

Each approach protects against different risks. Home storage eliminates counterparty risk entirely — nothing stands between you and your metal. Professional vault storage provides institutional-grade security, independent auditing, and full replacement insurance. Most experienced investors hold metal in both forms, using home storage for true independence and vaulted storage for liquidity and insurance.

What does allocated gold storage mean?

Allocated storage assigns specific metal to your ownership record by weight and type. Your holdings are not pooled into a fund or used as collateral. Every position is backed one-to-one by physical bullion in a vault, verified by independent auditors. It differs from unallocated storage, where you hold a claim against a pool rather than a direct ownership stake in specific metal.

SOURCES

1. Bank for International Settlements — Counterparty Credit Risk: Framework and Definitions

2. World Gold Council — Gold Demand Trends

3. Ludwig von Mises Institut — The Theory of Money and Credit

4. Underwriters Laboratories — UL 608: Standard for Burglary Resistant Vault Doors and Modular Panels

5. Insurance Information Institute — What Is Covered by Standard Homeowners Insurance?

6. Federal Deposit Insurance Corporation — Understanding Deposit Insurance

7. GoldSilver — Vault Storage: Allocated and Segregated Options

8. GoldSilver — Home Storage and Vault in One Account

Disclaimer: This article is for informational purposes only and does not constitute financial or investment advice. Always consult a qualified financial adviser before making investment decisions.

You may also like:

- Why Is Gold Still a Safe Haven? Switzerland’s Biggest Refiner Just Answered.

- Rate Hike Odds Just Hit 85%. Gold Is Up. Here’s Why.

- Gold Confiscation: Could the Government Take Your Gold Again?

- Gold Price History: From $35 to $4,500 in 100 Years

- The Debasement Trade Explained: Mechanism, History, and What It Means for Gold

- Gold or Silver First? A First-Time Buyer’s Framework

- Gold Reserves by Country: The 2026 Rankings

- Gold Portfolio Allocation: Why Wall Street Is Rewriting the 60/40

- What Does the SILVER Act Mean for Precious Metals Investors?

- What Backs the US Dollar? Not Gold. Not Silver.