Gold and silver market update — April 29, 2026

Key Takeaways

- When the lira came under severe pressure following a regional war shock, Turkey’s central bank sold and swapped over 127 tonnes of gold — its largest reserve drawdown on record

- This was not a sign that gold had failed. It was a distress signal from the lira — the sound money thesis playing out at sovereign scale

- Critically, most of the operations were gold-for-currency swap futures, meaning the gold is contractually scheduled to return to Turkey’s reserves on maturity

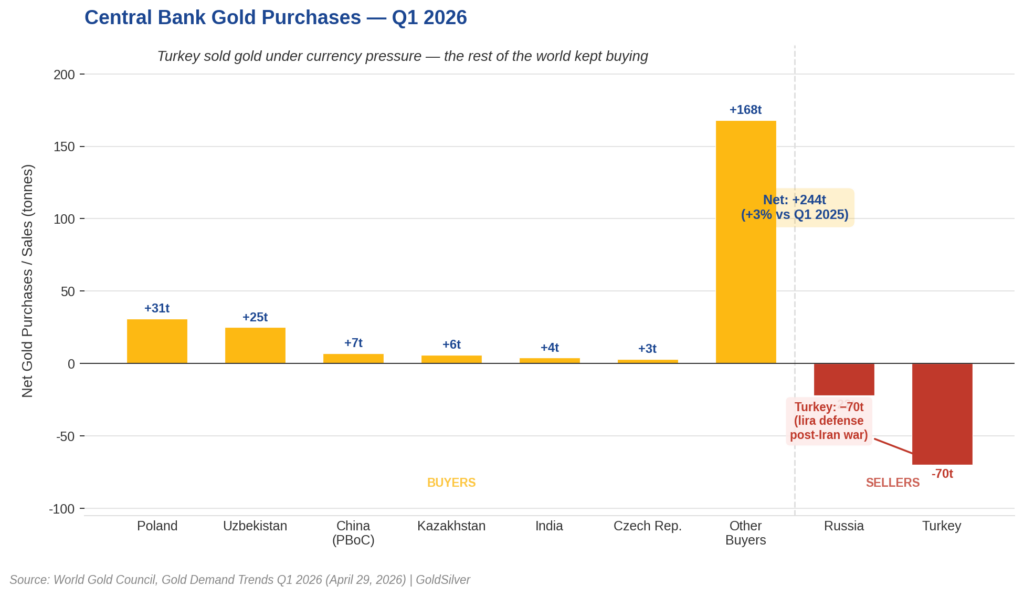

- Central banks globally remain net buyers of gold, with the World Gold Council recording net purchases of 244 tonnes in Q1 2026, up 3% year-on-year — the buyers far outpaced the sellers

- Turkey has since begun rebuilding its gold reserves as pressure on the lira eased — exactly as the historical pattern predicted

Turkey didn’t sell gold because gold was in trouble.

Turkey sold gold because its currency was.

When the US-Israel war on Iran began on February 28, 2026, the resulting energy shock sent the Turkish lira to a fresh record low. Turkey’s central bank, the CBRT, had already spent roughly $26 billion in foreign exchange reserves defending the currency.

When that wasn’t enough, it turned to its gold stockpile — selling and swapping over 127 tonnes in the weeks that followed. Mainstream coverage called it supply pressure. Technically, that’s not wrong. However, it’s the wrong question entirely. The real story is that a sovereign nation just demonstrated, in the most concrete terms possible, exactly why sound money exists.

Why Do Countries Sell Gold Reserves?

The financial media frames central bank gold selling as supply pressure — more gold hitting the market, prices fall. As far as it goes, that’s accurate. But it doesn’t go far enough.

The better question is why a country needs to sell at all. In Turkey’s case, the answer is a decade of monetary failure. The lira has lost over 90% of its value against the US dollar since 2016, falling from roughly 3.0 lira per dollar to a record low near 44.5.

inflation ran above 80% annually at its worst. A currency that far gone has no buffer left. When an external shock hits — in this case, an energy price surge driven by a regional war — the central bank runs out of conventional options fast. Gold becomes the last liquid reserve it can deploy.

Gold is a last resort. When a government reaches for it, that tells you nothing about gold. It tells you everything about the currency.

The mechanism is straightforward: Turkey was trading sound money for paper money because its own paper money had collapsed. That is not a bearish signal for gold. That is the gold thesis playing out, live, at the sovereign level.

This pattern is not unique to Turkey. Countries sell gold reserves for a consistent set of reasons — currency defense, liquidity needs during financial stress, or fiscal emergencies. Venezuela, Argentina, and Lebanon have all drawn down gold reserves in response to currency crises. In each case, the gold sale was a symptom of fiat failure, not a referendum on gold’s value.

Stay Ahead with Gold & Silver News The most important market insights, Fed updates, and global trends — everything investors need to make smarter, safer decisions.

Is Turkey’s Gold Selling a One-Off or a Broader Trend?

Turkey is an outlier, not a trend — and the resolution of this episode proves it.

Shortly after pressure on the lira eased following a ceasefire, the CBRT began rebuilding its reserves. By mid-April 2026, gold holdings had risen back to approximately 730 tonnes, up from a low of around 693 tonnes at end of March. Critically, the CBRT Governor confirmed that a significant portion of the operations were gold-for-currency swap futures — meaning the gold was never permanently sold. It was used as collateral to access liquidity, with the gold contractually scheduled to return to reserves on maturity.

This is consistent with how Turkey has used gold in every prior crisis. During the 2018 currency crisis, the lira lost around a third of its value over the year, with the sharpest single-day drop — roughly 20% — hitting in August after the US imposed new tariffs. The CBRT burned through reserves at a similar pace. Even so, gold held firm and rallied afterward. The same pattern emerged in 2023. In other words, Turkish selling is a finite, policy-driven response to acute stress — not a structural change in direction.

What Does the Global Central Bank Data Actually Show?

Meanwhile, the broader official sector picture remains firmly bullish. The World Gold Council’s (WGC) Q1 2026 Gold Demand Trends report shows central banks purchased a net 244 tonnes in Q1 2026, up 3% year-on-year. The WGC projects roughly 850 tonnes for the full year, nearly matching 2025’s 863-tonne total. Poland led Q1 buying with 31 tonnes, followed by Uzbekistan at 25 tonnes and the People’s Bank of China at 7 tonnes — its 17th consecutive monthly increase, bringing total PBoC holdings to approximately 2,313 tonnes as of March 2026.

There is a legitimate bear case worth addressing. If more central banks follow Turkey and Russia into forced selling, the buying thesis weakens. However, the Q1 data shows net purchases rose 3% year-on-year, even while Turkey was one of the largest sellers. The buyers are outpacing the sellers by a wide margin — and crucially, most of them aren’t selling under duress.

What Does Central Bank Gold Selling Mean for the Gold Price?

A central bank selling gold under duress is a supply shock. It moves prices in the short term. However, it is categorically different from a structural shift in demand.

Turkey’s episode is the clearest recent example of that distinction. At the peak of the drawdown, Turkey’s selling exceeded total global gold ETF outflows over the same two-week period. That’s an enormous volume concentrated into a short window — and yet the broader gold market absorbed it. When the selling stopped, as the CBRT began rebuilding reserves, the supply pressure dissipated.

UBS, in its April 2026 analysis of official sector gold markets, projected global central bank net purchases of 800–850 tonnes for 2026. It characterized Turkey’s moves as liquidity management and called a broader structural selloff “improbable.” That assessment has since been validated by Turkey’s reserve rebuilding.

In short, one country’s currency crisis does not unwind a decade of institutional accumulation. The dip created by forced selling gets absorbed — as it did in 2018, 2023, and again in early 2026 — once the acute pressure lifts.

What Does Turkey’s Crisis Tell Us About Gold’s Long-Term Role?

Turkey’s central bank bought gold for years precisely because it didn’t trust fiat alternatives. When crisis hit, it sold — not because gold failed, but because Turkey’s monetary system failed so completely that even its gold reserves couldn’t fully compensate.

Read that carefully. The lira’s collapse isn’t an argument against gold. Rather, it’s the argument for it, demonstrated in the starkest terms possible. Every Turkish saver who held gold over the past decade preserved real purchasing power. By contrast, every saver who held only liras did not.

Moreover, the episode revealed something that gets overlooked in the headlines. The very fact that Turkey had gold to sell is what gave its central bank options during the crisis. Countries without meaningful gold reserves — those that never accumulated — had no such buffer. Gold didn’t fail Turkey. It bought Turkey time.

Why Every Central Bank Is Paying Attention

The buying rationale across the rest of the world hasn’t changed. In 2022, Western nations froze roughly $300 billion of Russia’s central bank reserves.

As a result, every non-Western central bank received an unmistakable message: dollar reserves can be neutralized by political decision. Gold cannot. Turkey’s crisis reinforces that message from the other direction — a country that ran low on gold reserves found itself with far fewer options than one that hadn’t.

The sound money case doesn’t require catastrophe. It simply requires understanding why events like this keep happening — and who is protected when they do. Turkey is selling because its currency failed. Everyone else is still buying.

Investing in Physical Metals Made Easy

SOURCES

1. Reuters — Turkish Gold Reserves in Largest Drop in 7 Years, Data Shows

2. World Gold Council — Central Bank Gold Statistics: Central Banks Stay the Course on Gold in February

3. Türkiye Today — Turkish Central Bank Rebuilds Gold Reserves, Closes Swap Positions

4. Trading Economics — Turkish Lira Historical Exchange Rate Data

5. Wikipedia — Turkish Economic Crisis (2018–present)

6. World Gold Council — Gold Demand Trends Q1 2026

7. WGC — Gold Demand Trends Full Year 2025: Central Banks

8. WGC Gold Focus — China Gold Market Update: Seasonal Demand Rebound in March 2026

9. UBS Chief Investment Office — Gold’s Diversifying Utility Remains Intact

10. Brookings Institution — Why Do the US and Its Allies Want to Seize Russian Reserves to Aid Ukraine?

11. CNBC — Turkey Crisis: Economy Faces Weak Lira, Inflation, Debt and Tariffs

12. Al Jazeera — Turkey Lira Crisis: Six Things You Need to Know

13. Mining.com — Central Banks’ Gold Buying Momentum Carries Into 2026

By the GoldSilver Editorial Team — helping investors understand sound money since 2005. This article is for informational purposes only and does not constitute financial, investment, or tax advice. Always consult a qualified financial advisor before making investment decisions.

You May Also Like:

- Why Gold Spikes Every Time Hormuz Opens — And Why It Never Holds

- Oil Hits $100 and OPEC Is Fracturing. Gold Knows Why

- How China Restricts Silver Supply Without Touching Silver

- Powell Press Conference: What It Means for Gold

- Iran Blinked — And One Word From Powell Decides What Happens Next

- COMEX Silver First Notice Day April 30: What to Watch

- What Warsh as Fed Chair Means for the Gold Price

- 5 Signals the Mainstream Gold & Silver Narrative Missed