Published: 04-29-2026, 05:16 pm | Updated: 04-29-2026, 05:35 pm

Gold and silver market update — April 29, 2026

Key Takeaways

- On April 20, 2026, Agnico Eagle Mines committed approximately $3.8 billion across three deals to consolidate 2,492 km² of Finland’s Central Lapland Greenstone Belt — paying 67% and 46% premiums to acquire Rupert Resources and Aurion Resources, with the B2Gold Fingold stake closing April 23, 2026.

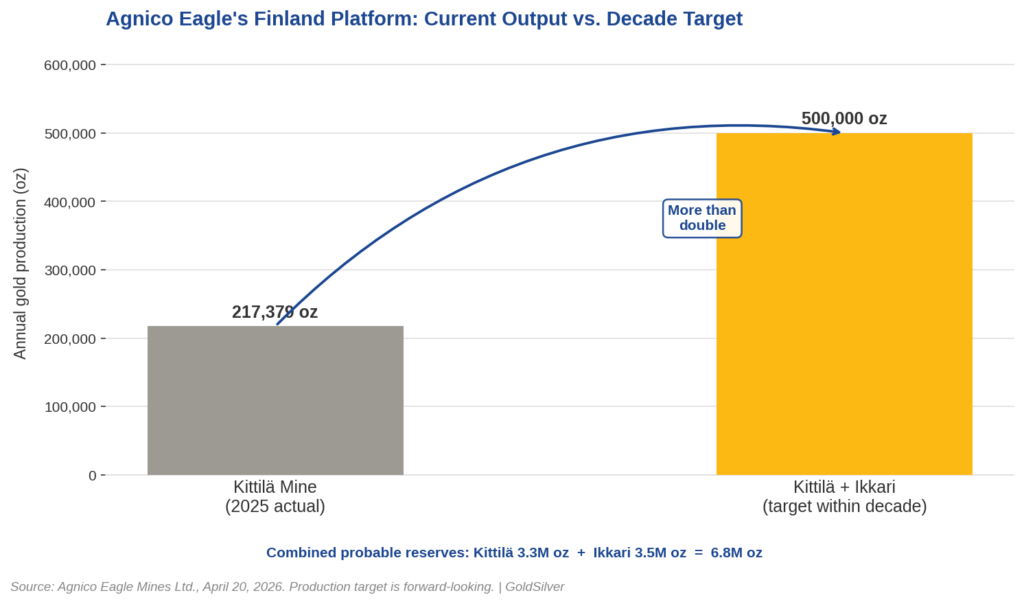

- The combined Kittilä-Ikkari platform holds approximately 6.8 million ounces in probable reserves, targets roughly 500,000 ounces of annual production within a decade, and is expected to generate up to $500 million in operating and development synergies.

- A 67% acquisition premium paid during a 19% gold price correction 2026 signals institutional conviction that gold’s structural bull case extends well into the 2030s.

Gold has pulled back 19% from its January 2026 all-time high of $5,589 per ounce. If you’ve been watching that gold price correction 2026 and wondering whether the structural case is still intact, Agnico Eagle Mines (NYSE/TSX: AEM) just answered the question — with $3.8 billion.

On April 20, 2026, the world’s most disciplined gold major announced three simultaneous deals to lock up nearly 2,500 square kilometers of Finland’s most prospective gold belt. It paid a 67% premium to do it. That’s not a company buying a dip. Instead, it’s a company expressing a decade-long view on gold prices — in the only language that matters in finance: committed capital.

Gold is trading near $4,523 per ounce (as of April 29, 2026), down from its January record.

What Did Agnico Eagle Buy in Finland?

The deal has three distinct parts. First, Agnico acquired Rupert Resources Ltd. (TSX: RUP), a Canadian developer holding the advanced Ikkari gold project in northern Finland, for C$2.9 billion in shares and contingent payments — a 67% premium to Rupert’s April 17, 2026 closing price.

Second, it acquired Aurion Resources Ltd. (TSXV: AU), a Finnish gold exploration company, for C$481 million all-cash — a 46% premium. Third, it purchased B2Gold Corp.’s (TSX: BTO) 70% stake in the Fingold Ventures joint venture for US$325 million cash, a deal that closed on April 23, 2026. Because Aurion held Fingold’s remaining 30%, Agnico now wholly owns that joint venture.

Together, these transactions give Agnico a 2,492 square kilometer land package in Finland’s Central Lapland Greenstone Belt. The company already operates Kittilä there — the largest primary gold mine in Europe, which produced 217,379 ounces in 2025.

Notably, the Ikkari gold project, held by Rupert Resources, sits 50 kilometers away and holds estimated probable reserves of 3.5 million ounces. Combined with Kittilä’s 3.3 million ounces, the consolidated platform holds approximately 6.8 million ounces in probable reserves as of April 20, 2026 — before a single drill hole on the new exploration ground.

The Edge Every Investor Needs Smarter precious metals investing starts here. The Nuggets Newsletter brings you essential market insights, Fed updates, global trends, educational videos, and much more.

Why Do the Synergies Matter?

Agnico says integrating Ikkari into its existing Kittilä platform will generate up to $500 million in operating, development, and construction synergies. In particular, the source of much of that value is a property boundary. Their land packages share an edge that previously constrained Ikkari’s open pit design.

Now that the boundary is gone, Agnico can optimize the pit across both packages. As a result, the executives say the combined platform could produce roughly 500,000 ounces annually within a decade — more than double Kittilä’s current output.

Why Did Agnico Pay a 67% Premium?

Agnico Eagle doesn’t overpay. That’s the track record. It absorbed Kirkland Lake Gold Ltd. in 2022 and Yamana Gold Inc.’s Canadian assets in 2023, and consistently grew reserves faster than it mined them. In both cases, the deals looked expensive at signing. In both cases, they proved out.

Paying 67% above market for Rupert sends a clear message: Agnico’s leadership believes the current gold price is not the price that matters. Instead, the price that matters is the one at which 500,000 ounces per year will be sold, a decade from now. They are buying for that world, not this one.

What Do Analysts Say About the Deal?

Jefferies LLC, the U.S. investment bank, estimated roughly 2% NAV per share accretion in an April 20, 2026 analyst note. That’s modest. However, accretion isn’t the point for a company with a $40 billion balance sheet. What they’re acquiring is the right to produce a half-million ounces a year in a top-tier jurisdiction when gold prices are, in their judgment, materially higher.

Doesn’t Buying During a Downturn Carry Risk?

The obvious pushback is that the deal was struck during a correction, with Western institutional gold demand soft and sentiment weak. That’s a reasonable short-term observation. Even so, Agnico has done this before. Agnico acquired both Kirkland Lake and Yamana during periods of mixed gold sentiment. In each case, buying doubt proved more profitable than buying confidence.

The mechanism is straightforward: lower acquisition prices during downturns improve long-run returns per ounce, while the underlying gold thesis remains intact. Agnico isn’t contrarian for its own sake. It’s patient.

Why Is Finland the Right Jurisdiction for a $3.8 Billion Bet?

Where you mine matters as much as what you mine. Finland ranks among the world’s most stable mining jurisdictions — strong rule of law, no nationalization risk, transparent regulation, and full EU membership. That combination is rare. In fact, most of the world’s remaining large undeveloped gold deposits sit in jurisdictions where those guarantees don’t hold.

CEO Ammar Al-Joundi put it plainly at the April 20, 2026 announcement: “This consolidated land package is the most prospective land package, not just in Finland, but in all of the Nordic Region.” A company committing $3.8 billion to a single region is staking its next decade on that claim being true.

Furthermore, the same forces that drive gold demand — monetary instability, fiscal stress, loss of confidence in fiat systems — also create political risk in resource-rich developing nations. Because of this dynamic, Agnico is concentrating capital where those forces are least likely to interrupt production. It’s a hedge within a hedge: bullish on gold, careful about where that gold comes from.

What Does This Tell a Physical Gold Holder?

Agnico Eagle’s $3.8 billion Finland consolidation is a concrete institutional signal that gold’s structural bull case remains intact through at least the mid-2030s. On April 20, 2026 — with gold trading 19% below its January all-time high of $5,589 — Agnico paid 67% and 46% premiums for Rupert Resources and Aurion Resources, and US$325 million for B2Gold’s Fingold stake.

In addition, Agnico estimates up to $500 million in synergies from integrating the Ikkari gold project with Kittilä, which produced 217,379 ounces in 2025. The combined platform holds approximately 6.8 million ounces in probable reserves and targets roughly 500,000 ounces of annual production within a decade, per Agnico’s April 20, 2026 press release.

The Second Corner Most Press Coverage Will Miss

The mainstream press will cover this as an M&A story: deal premiums, shareholder votes, accretion analysis. That’s the first corner. The second corner, however, is harder to see.

Agnico didn’t announce a view on gold prices. It enacted one. Binding legal agreements worth nearly $4 billion are not made on hope — they’re made on conviction backed by capital that cannot be recalled. The most disciplined acquirer in the gold mining industry looked at a 19% correction and decided it didn’t change the decade-long thesis.

That’s the signal. Not the deal mechanics. Not the production targets. The fact that this company, at this moment, moved this much capital in this direction.

What to Watch Next

Two transactions remain open. Specifically, the Rupert Resources and Aurion Resources acquisitions require shareholder votes and regulatory approval, with closing expected in early Q3 2026. The main risk to watch is any pushback from Rupert shareholders on the premium, or regulatory delay in Finland.

Beyond the deal itself, watch Agnico’s Q2 2026 earnings for Ikkari development updates — any acceleration in the timeline would sharpen the 500,000 oz/year production case considerably. On the macro side, the May 2026 CPI print and incoming Fed Chair Kevin Warsh’s first public signals on rate policy are the next meaningful data points for gold. Gold was $5,589 in January. It’s around $4,523 today.

Nevertheless, Agnico looked at that gap and spent $3.8 billion anyway. That context doesn’t expire.

Stay On Top of Gold & Silver Prices

Get important market alerts sent straight to your inbox.

SOURCES

1. Agnico Eagle Mines Ltd. — Finland Consolidation Press Release, April 20, 2026

2. Agnico Eagle Mines Ltd. — SEC Form 6-K, April 20, 2026

3. B2Gold Corp. — Fingold Sale Completion, April 23, 2026

4. Aurion Resources Ltd. — Acquisition Press Release, April 20, 2026

5. Rupert Resources Ltd. — Acquisition Press Release, April 20, 2026

6. Jefferies LLC — Analyst Note via Yahoo Finance, April 20, 2026

7. World Gold Council — Gold Price Data

By the GoldSilver Editorial Team — helping investors understand sound money since 2005. This article is for informational purposes only and does not constitute financial, investment, or tax advice. Always consult a qualified financial advisor before making investment decisions.

You May Also Like:

- Gold, Oil, and the Fed: Why the Old Rules Don’t Apply

- Why Turkey Sold Its Gold Reserves — And What It Proves About Sound Money

- Why Gold Spikes Every Time Hormuz Opens — And Why It Never Holds

- Oil Hits $100 and OPEC Is Fracturing. Gold Knows Why

- How China Restricts Silver Supply Without Touching Silver

- Powell Press Conference: What It Means for Gold

- Iran Blinked — And One Word From Powell Decides What Happens Next

- COMEX Silver First Notice Day April 30: What to Watch