Published: 05-06-2026, 12:22 pm | Updated: 05-06-2026, 02:09 pm

Gold has evolved from a crisis hedge into a core portfolio asset — and the data supports treating it as one permanently. In 2025, total global gold demand surpassed 5,000 tonnes for the first time in history, with central banks purchasing 863 tonnes despite prices at record levels. The forces driving gold’s long-term value — monetary debasement, fiscal deficits, and the breakdown of stock-bond diversification — remain firmly in place. A 5–15% gold portfolio allocation has historically improved risk-adjusted returns across portfolio types, without requiring investors to call short-term price movements.

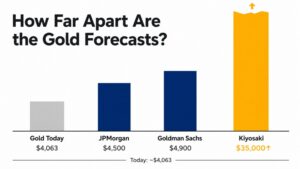

Gold is trading near $4,700 per ounce as of early May 2026 — approximately 16% below its all-time high of $5,589.38, set on January 28, 2026 [CBS News]. To the short-term trader, that looks like a pullback. To the long-term investor, it looks like an entry point. The real question isn’t whether gold will make new highs. It’s whether you have any exposure when it does.

What Makes Gold a Core Asset Rather Than Just a Hedge?

A hedge is reactive. You buy it when fear spikes, and sell it when the crisis passes. A core asset, however, is different — it earns its place because of what it consistently does across full market cycles: reduce portfolio risk, protect purchasing power, and hold value when other assets fail. It’s held for structural reasons, not timing decisions.

For most of the past 40 years, gold was treated as the former. That framing is now obsolete. The conditions that once made bonds reliable portfolio ballast — low inflation, stable growth, and negative stock-bond correlations — have fundamentally shifted. As a result, bonds no longer provide the diversification investors assumed they would. Gold does.

Your Gold Buying Guide Most investors overpay when they buy gold. Then overpay again when they sell. This guide shows you exactly what to own — and why.

Why the 60/40 Portfolio Can’t Do the Job Alone

The 60/40 model was built on one critical assumption: stocks and bonds move in opposite directions. When equities fall, bonds rise, and the portfolio stabilizes. That relationship held for three decades. It has since broken down.

In a world of structural fiscal deficits, elevated sovereign debt, and higher-for-longer interest rates, bonds and equities increasingly move together during stress events. Consequently, the ballast investors relied on has quietly disappeared.

Gold fills that vacancy. Its correlation with U.S. equities over the past 20 years is approximately 0.14 — effectively zero. That means it tends to hold its value, or rise, precisely when the rest of a portfolio is under pressure. European institutional investors have already drawn that conclusion. In WisdomTree’s 2025 Investor Survey of 802 participants across Europe and the U.K., average gold allocations reached 5.7% — equal to developed-market sovereign debt holdings [WisdomTree]. Gold isn’t being treated as a fringe position anymore. It’s sitting alongside sovereign bonds as a mainstream portfolio anchor.

What Are Central Banks Telling Us About Gold?

Central banks are the most patient investors in the world. They don’t chase momentum. When they buy gold at scale — year after year, at record prices — it reflects a long-term strategic calculation, not a reaction to headlines.

In 2025, central banks purchased 863 tonnes of gold. That’s the fourth-largest annual expansion of global official gold reserves on record, and nearly double the 2010–2021 annual average of 473 tonnes. Furthermore, 95% of central banks surveyed expected global reserves to increase over the next 12 months — the highest level of optimism in the survey’s eight-year history, with none anticipating a reduction [World Gold Council]. Late in 2025, gold overtook U.S. Treasuries to become the world’s largest reserve asset by value — a milestone not seen since 1996.

Poland’s National Bank was the single largest buyer. It added 102 tonnes, bringing total holdings to 550 tonnes — representing 28.2% of its official reserves as of 31 December 2025, up from 16.9% just one year earlier [National Bank of Poland]. Similarly, Kazakhstan recorded its highest annual purchase since 1993, and Brazil returned to the gold market after a four-year absence.

Gold is a liquid asset with no counterparty risk, no issuer that can default, and no government that can freeze it. When nation-states treat it as a primary reserve asset, that’s about as strong an institutional endorsement as the metal can receive.

How Does Gold Actually Perform When Markets Turn?

Gold isn’t designed to beat equities in every environment. In a sustained bull market, stocks will produce higher returns — that’s by design. Gold’s job is to hold its ground when everything else doesn’t.

Consider the historical record. During the 2008 financial crisis, the S&P 500 fell 38.5%, while gold ended the year with a small positive return, outperforming virtually every other major asset class. Similarly, in 2020, gold gained approximately 25% for the full year. In 2025 — a year with 53 new all-time highs — total gold demand surpassed 5,000 tonnes for the first time ever, generating $555 billion in total value, a 45% year-over-year increase [World Gold Council].

The more telling detail is who was buying. Bar and coin investment hit a 12-year high of 1,374 tonnes in 2025, up 16% year-over-year. Meanwhile, jewelry fabrication fell 19% to 1,638 tonnes as record prices squeezed volume buyers. These are patient, long-term holders — not traders chasing momentum. When investment demand surges while consumer fabrication contracts, it signals durable price support rather than a speculative run.

That resilience isn’t coincidental. Gold carries no credit risk, has no issuer that can default, and can’t be frozen by any government. In a world where geopolitical fragmentation and sovereign debt expansion are permanent features rather than passing phases, those properties only become more valuable over time.

What Is the Right Gold Portfolio Allocation?

The research converges on a clear range: 5–15%. Yet most individual investors hold far less.

Adding gold at 2.5%, 5%, 7.5%, or 10% improved risk-adjusted returns for a standard USD portfolio across the past 20 years, while also reducing maximum drawdown. Even a 5% allocation improved the Sharpe ratio meaningfully — and that’s real data across multiple economic cycles, not a theoretical projection [World Gold Council].

Several institutional voices have pushed that range even higher. Sprott Asset Management advocates for a permanent 10% allocation to physical gold. Flexible Plan Investments’ 2025 research identifies 18% as the historically optimal allocation from a risk-reward standpoint, with positions up to 35% still remaining mathematically efficient. At the Greenwich Economic Forum, Ray Dalio put his number at 15%, calling gold the optimal diversifier for a portfolio exposed to debt and currency debasement risk.

The institutional price outlook reinforces that picture. On February 2, 2026, J.P. Morgan revised its year-end 2026 gold price target to $6,300 per ounce — up from an earlier base case of $5,055 — citing an “ongoing, unexhausted trend of reserve diversification” [TheStreet]. If your current allocation is below 5%, you may therefore be underexposed by the standards of what institutional models now consider prudent.

Above all, the most important principle is consistency. A 10% allocation held through volatility and rebalanced annually outperforms a 20% position that gets sold at the first drawdown. Gold rewards patience. To think through the right sizing for your own portfolio, How Much of Your Portfolio Should Be in Precious Metals? is worth reading next.

Stay On Top of Gold & Silver Prices

Get important market alerts sent straight to your inbox.

People Also Ask

Why is gold considered a core portfolio asset and not just a hedge?

A hedge is reactive — bought in fear and sold when the crisis passes. A core asset, by contrast, earns its place through what it consistently delivers across full market cycles: lower volatility, reduced drawdowns, and purchasing power protection. Gold’s correlation with equities over the past 20 years is approximately 0.14 — effectively zero. That means it diversifies in normal markets, not just in crises. That’s what makes it a core holding rather than a tactical position.

What are the benefits of including gold in a diversified investment portfolio?

Gold improves risk-adjusted returns without requiring investors to time the market. Specifically, World Gold Council analysis shows that allocating 5–10% to gold improved Sharpe ratios and reduced maximum drawdowns for a standard USD portfolio over a 20-year period. Beyond the performance data, gold also provides structural protection against inflation, currency debasement, and geopolitical risk — forces that aren’t temporary.

How does gold perform compared to traditional assets like stocks and bonds?

Equities outperform gold over the very long run — that’s not in dispute. However, gold consistently outperforms both stocks and bonds during periods of financial stress, elevated inflation, and currency debasement. In 2025, for example, gold set 53 new all-time highs and generated $555 billion in total demand value, a 45% year-over-year increase, while equity markets experienced significant volatility.

What percentage of a portfolio should be allocated to gold?

Most institutional research converges on 5–15% for individual investors. World Gold Council data shows risk-adjusted improvements at 5%, 7.5%, and 10% allocation levels. In addition, Sprott recommends 10% as a permanent position, and Ray Dalio has publicly cited 15% as his own target. The right number ultimately depends on portfolio composition, time horizon, and risk tolerance.

How does gold’s role change during economic uncertainty or market volatility?

During stress periods, gold’s near-zero equity correlation tends to turn mildly negative — meaning it often rises when equities fall hardest. That’s when its protective function is most visible. However, the long-term case isn’t built on crisis performance alone. Fiscal expansion, monetary debasement, and de-dollarization are ongoing structural trends. As a result, gold’s properties — no credit risk, no counterparty, no issuer — make it relevant across all market environments, not just volatile ones.

The Shift Has Already Happened — Has Your Portfolio Caught Up?

Something has fundamentally changed in the way serious money thinks about gold. It no longer needs to be argued for in the abstract, because the data makes the case on its own. Central banks bought 863 tonnes in a single year at record prices. Moreover, European institutional allocations now match sovereign bond holdings, and the 60/40 model that anchored a generation of financial planning has broken down. None of this is a forecast — it has already happened.

What hasn’t caught up, for most individual investors, is the portfolio itself. The research is clear: a 5% gold portfolio allocation is not a bold bet. It’s the threshold at which the World Gold Council’s 20-year data shows meaningful improvement in risk-adjusted returns. Nevertheless, the average private investor is well below it.

The current pullback from January’s all-time high doesn’t change the structural case. If anything, it creates the kind of entry point that long-term holders look back on and wish they’d used. Gold rewards people who treat it for what it is — a permanent piece of a resilient portfolio, not a trade to time.

If you’re ready to think seriously about what the right allocation looks like, GoldSilver.com is a good place to start.

SOURCES

1. CBS News — What Is the Highest Gold Price in History?

2. WisdomTree — Rethinking the Golden Allocation

3. World Gold Council — Gold Demand Trends Full Year 2025: Central Banks

4. Poland Daily — NBP President Glapiński: Gold Reserves Will Grow to 700 Tonnes

5. World Gold Council — Gold Demand Trends Full Year 2025

6. World Gold Council — Portfolio Impact: Risk/Reward Profile

7. TheStreet — J.P. Morgan Revises Gold Price Target for 2026 (via Reuters)

8. GoldSilver.com — Is Gold Still a Strategic Asset for Your Portfolio?

9. GoldSilver.com — Why Gold and Silver Are Shifting from Crisis Hedges to Return Drivers

10. GoldSilver.com — The Quiet Revolution in Central Bank Gold Buying

Disclaimer: This article is for informational and educational purposes only. It does not constitute investment advice. Please consult a qualified financial adviser before making any investment decisions.

You may also like:

- Silver vs. Gold: A Clear 5-Year Investment Guide (2026–2031)

- $5,500 Gold by Q1 2027? The Central Bank Risk Driving It

- Why Gold Stabilizes — and Silver Amplifies

- COMEX Silver Coverage Ratio: Is Your Paper Silver Real?

- What the Gold Price Per Ounce Really Tells You

- The Gold Inflation Paradox Most Investors Miss

- Insurance vs. Upside: Balancing Your Portfolio with Gold and Silver

- Gold Bullion vs. Jewelry: Why Serious Investors Choose the Bar