Published: 04-30-2026, 09:58 am

Gold and silver market update — April 30, 2026

Key Takeaways

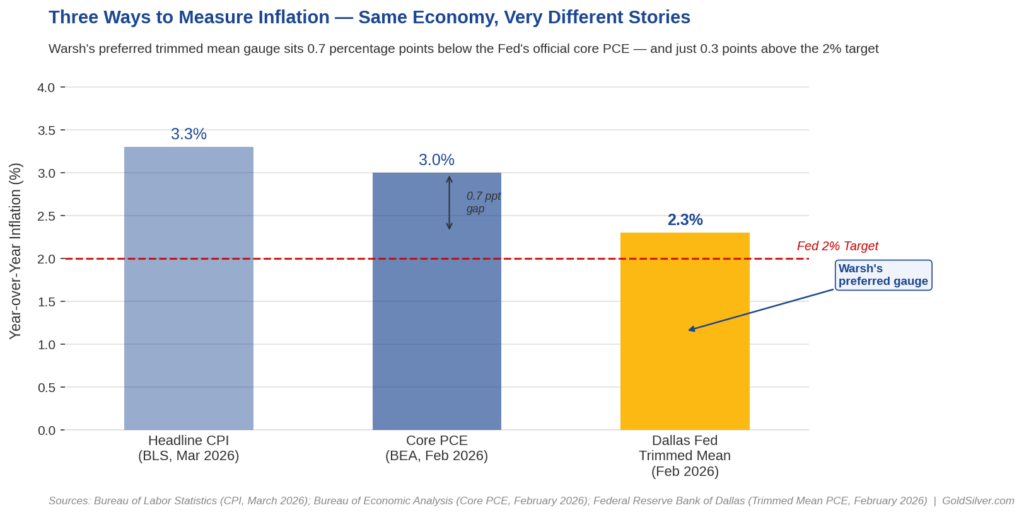

- Incoming Fed Chair Kevin Warsh prefers a “trimmed mean” inflation measure that currently reads 2.3% — versus the official core PCE at 3.0% — meaning he may take the helm treating inflation as already near the Fed’s 2% target

- If Warsh governs by that framework, the path to rate cuts opens. Lower rates compress real yields. Compressed real yields are gold’s primary structural tailwind

- Yesterday’s FOMC vote was the most divided since October 1992 — four dissenters, two opposing directions — and Warsh inherits every one of those fault lines on May 15

Kevin Warsh told the Senate Banking Committee on April 21 that he doesn’t fully trust the Fed’s own inflation measure. The incoming Federal Reserve Chair — taking over from Jerome Powell on May 15, 2026 — wants to shift toward a “trimmed mean” approach. That alternative gauge, published by the Federal Reserve Bank of Dallas, reads 2.3% on a 12-month basis.

The Fed’s official core Personal Consumption Expenditures (PCE) index reads 3.0%. That 0.7 percentage point gap is not a rounding error. It is potentially the difference between a Fed that holds and a Fed that cuts. For the gold price, Warsh’s inflation measurement stance is the most consequential thing said in Washington this month.

Gold climbed to around $4,600 in early US trading this morning, recovering more than 2% from yesterday’s one-month lows.

What Is the Trimmed Mean PCE, and Why Does Warsh Prefer It?

The standard PCE averages all price changes across hundreds of spending categories. The trimmed mean, however, throws out the extreme movers on both ends — the wild outliers — and averages what remains.

Think of it like a figure skating competition. The highest and lowest scores are dropped. What remains is a cleaner read on the middle of the pack.

In February 2026, the Federal Reserve Bank of Dallas stripped out two outliers: a 384% spike in moving and storage services, and a 50% plunge in telephone equipment prices. What remained gave a 12-month inflation rate of 2.3% — versus the official core PCE reading of 3.0%.

Warsh’s argument is that oil shocks, tariff-driven price spikes, and other one-off disruptions shouldn’t dictate monetary policy. At his April 21 confirmation hearing, he dismissed core PCE as a “rough swag as to what was going on” with prices. “We don’t have to do a rough swag any more,” he said.

Here’s what mainstream coverage is missing: this isn’t a statistics debate. It is a policy lever. If Warsh governs by the trimmed mean, inflation is already at 2.3% — within 0.3 points of the Fed’s target. That makes rate cuts justifiable on the numbers, even while the official gauge says they aren’t.

How Does a Change in Inflation Measurement Move the Gold Price?

Everything runs through one mechanism: the real yield.

Real yield equals the nominal interest rate minus inflation expectations. When real yields fall, gold rises. When they climb, gold faces pressure. This relationship has held across decades and market regimes.

The FOMC currently holds its benchmark rate at 3.5%–3.75%. Against official core PCE of 3.0%, the implied real yield is roughly 0.6%–0.75% — thin, but positive. Now shift the inflation input to Warsh’s 2.3% trimmed mean. The same nominal rate then implies a real yield of around 1.3%. That gives the Fed more room to cut without prematurely claiming victory over inflation. Furthermore, every rate cut compresses real yields further.

Lower real yields reduce the opportunity cost of holding gold — an asset that pays no interest. That’s precisely when central bank and institutional buyers tend to accelerate. The World Gold Council reported 244 tonnes of net central bank purchases in Q1 2026 alone. If the rate environment turns more accommodative under Warsh, those buyers don’t slow down — they lean in.

The Edge Every Investor Needs Smarter precious metals investing starts here. The Nuggets Newsletter brings you essential market insights, Fed updates, global trends, educational videos, and much more.

Does Today’s GDP and PCE Data Change the Picture?

This morning’s data release made the stakes concrete. The Bureau of Economic Analysis (BEA) released its Q1 2026 GDP advance estimate and March PCE figures simultaneously at 8:30am ET. Wall Street expected GDP growth of 1.8% annualised. Meanwhile, the Federal Reserve Bank of Atlanta’s GDPNow model had been tracking as low as 1.2%.

Slow growth combined with sticky inflation points to stagflation — the one macro environment where the gold price has consistently outperformed every major asset class.

Under the official core PCE lens, stagflation looks severe and rate cuts look impossible. Under Warsh’s trimmed mean lens, by contrast, the inflation half of that equation is already approaching target. The same economic conditions therefore produce two entirely different policy conclusions, depending on which ruler you use.

The April 29 FOMC decision showed how deep those divisions already run. The vote to hold at 3.5%–3.75% was 8–4 — the most fractured Fed decision since October 1992. Governor Stephen Miran voted for an immediate 25-basis-point cut. Cleveland Fed President Beth Hammack, Minneapolis Fed President Neel Kashkari, and Dallas Fed President Lorie Logan voted the opposite way.

All three opposed the statement’s dovish language, signalling they see no path to cuts in the near term. Warsh walks into a committee split between two different views of where rates should go. His Warsh inflation measurement framework would pull one group toward him, and harden the other.

Isn’t the Trimmed Mean Also Flawed?

Yes. Bank of America economist Aditya Bhave has pointed out two problems. First, the trimmed mean has overstated inflation relative to core PCE in some past environments. Second, today’s energy shock is broad-based — not the kind of isolated outlier the trimming process is designed to remove. As a result, the trimmed mean could read higher than Warsh expects if oil-driven price pressure bleeds through.

That’s a real risk to the near-term rate-cut case.

Still, it’s the wrong question for gold investors. The deeper issue isn’t whether the trimmed mean is accurate. It is what Warsh’s preference reveals about the institution he’s about to lead.

On April 21, 2026, Warsh told the Senate Banking Committee: “After COVID, when prices went up to the tune of 25 to 35% for virtually all deciles of the American people, that’s an indication that the Fed missed its mark.” He added: “We are still dealing with the legacy of the policy errors in 2021 and 2022.”

That’s a Fed chair nominee publicly indicting his institution’s recent record. A central bank that admits it lost control of inflation — and is now hunting for new measurement tools — is not projecting monetary credibility. It is exposing structural doubt. Gold has absorbed monetary credibility gaps for five thousand years. Consequently, this one is no different.

So Where Does This Leave the Gold Price?

Warsh might not cut at his first FOMC meeting in June. The Strait of Hormuz remains closed and oil prices are elevated, and the stagflation trade still has legs.

Nevertheless, none of that changes the shift that happened on April 21. The incoming Fed Chair has redefined, at least provisionally, what “near target” means. If trimmed mean PCE is the yardstick, the US is already within 0.3 points of 2%.

That’s not a rate-cut prediction — it’s a change in the policy ceiling. Real yields could compress even without a single cut, simply through the signal that cuts are coming sooner than the official data implies.

Gold near $4,600, up over 2% this morning, is therefore not reacting to today’s GDP number. Instead, it’s repricing the next 12 months of monetary policy under a chair who just told the Senate he doesn’t trust his predecessor’s instruments.

Stay On Top of Gold & Silver Prices

Get important market alerts sent straight to your inbox.

SOURCES

1. Federal Reserve Bank of Dallas — Trimmed Mean PCE Inflation Rate, February 2026

2. CNBC — Warsh Pushes His Plan for ‘Regime Change’ at Senate Hearing

3. Rev — Kevin Warsh Senate Banking Committee Confirmation Hearing Transcript, April 21, 2026

4. Federal Reserve — FOMC Statement, April 29, 2026

5. Bureau of Economic Analysis — GDP and PCE Release Schedule

6. Federal Reserve Bank of Atlanta — GDPNow Model Estimate, Q1 2026

7. World Gold Council — Record Gold Prices Continue to Shift Demand Dynamics, Q1 2026

8. CNBC — Kevin Warsh Gave His Preferred Way for Measuring Inflation. It Could Come Back to Bite Him

9. Trading Economics — Gold Spot Price, April 30, 2026

By the GoldSilver Editorial Team — helping investors understand sound money since 2005. This article is for informational purposes only and does not constitute financial, investment, or tax advice. Always consult a qualified financial advisor before making investment decisions.

You May Also Like:

- Gold Is Down 19%. This $3.8B Bet Says It Doesn’t Matter

- Gold, Oil, and the Fed: Why the Old Rules Don’t Apply

- Why Turkey Sold Its Gold Reserves — And What It Proves About Sound Money

- Why Gold Spikes Every Time Hormuz Opens — And Why It Never Holds

- Oil Hits $100 and OPEC Is Fracturing. Gold Knows Why

- How China Restricts Silver Supply Without Touching Silver

- Powell Press Conference: What It Means for Gold

- Iran Blinked — And One Word From Powell Decides What Happens Next