Published: 04-17-2026, 06:03 pm | Updated: 04-17-2026, 06:15 pm

America now spends more on debt interest than on defending the country. That crossover happened quietly. Most people missed it. Gold didn’t.

Gold closed Friday, April 17, 2026, at $4,867 per ounce — up 1.65% on the day, more than 41% from a year ago, and higher for the fourth consecutive week. Silver closed at $79.60, up 1.52% on the day and roughly 4% for the week — its fourth straight weekly advance. The US Dollar Index, which tracks the dollar against six major currencies, held near six-week lows in the 98–99 range.

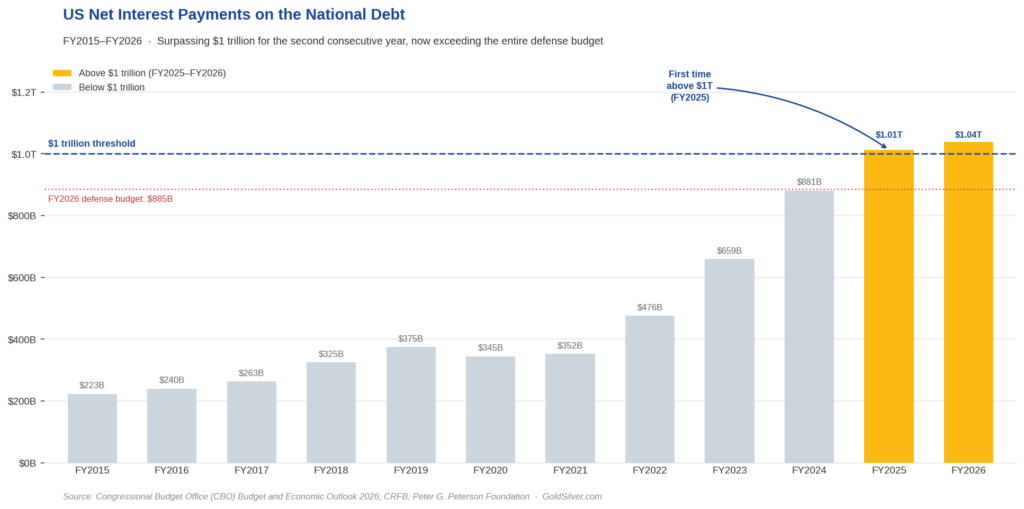

That same week, the Congressional Budget Office confirmed the US will pay more than $1 trillion in debt interest in fiscal year 2026 — the second consecutive year above that threshold.

Why Does $1 Trillion in Annual Debt Interest Matter?

It exceeds the entire defense budget, enacted at $885 billion for fiscal year 2026. That’s more than Washington spends on Medicaid — and more than it spends on transportation, education, and veterans’ benefits combined. The only federal programs bigger are Social Security and Medicare.

And unlike any of those, this spending produces nothing. Roads go unbuilt. Soldiers go unfunded. Patients go untreated. Every dollar is the price of debt that already exists — for spending that already happened.

The Congressional Budget Office projects interest costs will hit $2.1 trillion annually by 2036. By 2048, net interest is projected to overtake every other budget line item — including Social Security. It would become the single largest expenditure the federal government makes.

What Is Fiscal Dominance, and Why Is It Bullish for Gold?

Economists have a name for this: fiscal dominance. It is the condition in which a government’s debt load grows so large it begins to override monetary policy. The debt effectively starts setting interest rates — not the central bank.

You can see it operating right now. The Federal Reserve meets April 28–29. According to the CME FedWatch Tool, markets are pricing better than 97% odds the Fed holds rates steady at 3.50%–3.75%. Not because inflation is under control — the Bureau of Labor Statistics reported the Consumer Price Index at 3.3% for March 2026, up from 2.4% in February. And not because the economy is strong — the Institute for Supply Management’s services employment index fell to 45.2 in March, a level that signals contraction.

The Fed is holding because it is trapped. Cut rates and inflation accelerates. Raise rates and the $1 trillion interest bill grows even larger, compounding the fiscal damage while slowing an already fragile economy. Paralysis here isn’t indecision — it’s arithmetic.

The Edge Every Investor Needs Smarter precious metals investing starts here. The Nuggets Newsletter brings you essential market insights, Fed updates, global trends, educational videos, and much more.

How Does the Debt Problem Translate Into Gold and Silver Prices?

Fiscal dominance suppresses real yields — the return on savings after inflation. When real yields are low or negative, gold and silver tend to outperform. Cash and bonds lose purchasing power when inflation outpaces their yield. Gold doesn’t pay interest — but it also doesn’t dilute.

Gold and silver cannot be printed. Global mine supply grows at roughly 1–2% per year, regardless of what any government or central bank decides. They are, by nature, outside the debt system entirely.

Which is why gold’s 41% gain over the past twelve months is not a surprise. It is a measurement.

There is a fair counterargument: if the Fed eventually does hike hard to break inflation, real yields rise and gold faces genuine headwinds. Worth taking seriously. But hiking at $1 trillion in annual interest makes the fiscal crisis dramatically worse. Paul Volcker could raise rates to 20% in 1980 because the national debt was manageable. Today’s debt-to-GDP ratio leaves no equivalent room. That structural constraint is what gold has been pricing in — not panic, not chaos. Just arithmetic.

The $1 trillion figure is not a warning shot. It landed two years ago, quietly, and the number has only grown since. Watch what happens if the Fed eventually tries to fight inflation seriously. That’s when the constraint becomes visible to everyone — not just to gold.

Stay On Top of Gold & Silver Prices

Get important market alerts sent straight to your inbox.

SOURCES

1. Congressional Budget Office — Monthly Budget Review: Summary for Fiscal Year 2025; The Budget and Economic Outlook: 2026 to 2036; The Long-Term Budget Outlook: 2025 to 2055

2. Congressional Research Service — FY2026 Department of Defense Appropriations: In Brief

3. Bureau of Labor Statistics — Consumer Price Index: March 2026

4. Institute for Supply Management — Services PMI Report: March 2026

5. Federal Reserve — FOMC Meeting Calendar 2026; Minutes of the FOMC Meeting, March 17–18, 2026

6. London Bullion Market Association — Gold and Silver Price Data

7. World Gold Council — Gold Supply Data

By the GoldSilver Editorial Team — helping investors understand sound money since 2005. This article is for informational purposes only and does not constitute financial, investment, or tax advice. Always consult a qualified financial advisor before making investment decisions.

You May Also Like:

- 5 Signals That Say Gold’s Bull Case Just Got Stronger

- The Largest Gold ETF Outflow Ever – But China Disagrees

- Silver Market Deficit 2026: Six Years and Getting Worse

- Is the Petrodollar Ending? What the Iran War Means for Gold

- France’s Gold Repatriation Is Done. Germany Is Next

- Gold/Silver Ratio Hits 61.1 — Silver’s Turn to Run

- Silver Holds Near $80 as Iran Ceasefire Revives Rate-Cut Bets

- The Fed Goes Silent in 3 Days – What Does That Mean For Gold?